Online retail sales growth slowed in May following a fairly strong April

Insight

US 10 year Treasury yields are very close to 3 percent this morning. As NAB’s David de Garis explains to Phil Dobbie its resulted in rising bond yields elsewhere, including Europe and Australia.

https://soundcloud.com/user-291029717/us-yields-climb-commodities-drop

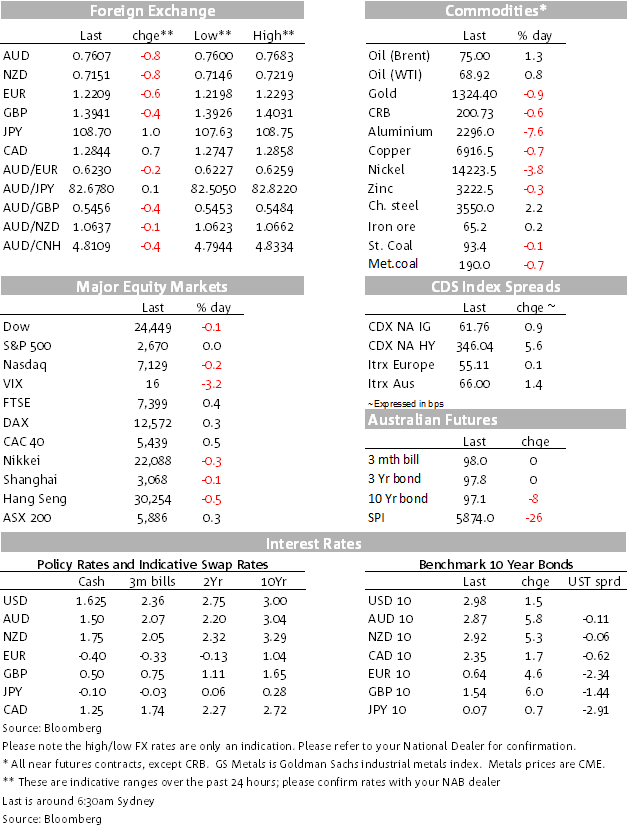

The overnight session has been marked by further strength in the USD, further rises in US Treasury and global bond yields, and commodity price volatility. US equities finished flat to lower, again led down by tech shares (especially semiconductor related stocks). Alphabet has reported after the bell, earnings beating estimates with after-hour trading marking their shares higher. In the wash up of the further rally in the USD, the AUD has made a new low for the year, reaching 0.76 in late NY trading. The preliminary estimates of PMIs for Germany, France and the Eurozone all pointed to solid rates of growth continuing into the second quarter.

The USD has been on a further tear, taking up in Europe where the trading mood ended last week. The DXY is up 0.69% and the spot Bloomberg dollar index up 0.84%, now looking like it’s setting the scene and looking for some clean air for a move above its rather restricted trading range evident for most of this year. The DXY has been testing its highs for this year seen in the earlier part of January. It’s been a yield driven story, with rises in US yields along the curve, by a net 1-2 bps in net terms for the session, 10s having tested close to 3% with an intra-session high 2.996% earlier in the session and ending the US session at a still sturdy 2.975%. The market is pricing toward three more Fed rate hikes this year.

In the commodity space, base metals have had some big moves, but this time lower as the US softened its sanctions position on Rusal with the proposal to remove sanctions on the company if its owner Oleg Deripaska relinquishes control of the company. Base metals retreated quickly, Ally down 7.05% for the session and having retraced the big move up last week and back to levels of 10 days ago. Nickel also fell back, down 3.81%, copper by 0.69%. When this move happened, oil went lower along for the ride, but it has since retraced on news of Iranian-backed Houthi rebels in Yemen launching unsuccessful missile attacks against Saudi Arabia. Brent is currently trading at $US75/bbl, with WTI knocking on the door of $US69/bbl. French President Macron has just arrived in Washington in an effort to keep the Iran lifting of sanctions deal alive to avert US sanction among a host of other political and economic discussions, all highly relevant for oil, not to mention the state of geopolitical tensions.

On the economic front, the main data of interest has been the French, German and Eurozone preliminary PMIs for April. They showed very little sign of flinching from the still-high levels still evident in March. There was very little change in the Manufacturing, Services, and Composite PMIs, the Composite PMIs steady-to-fractionally higher. Germany’s was at 55.3 (+0.2), France’s at 56.9 (+0.6), and the Eurozone’s at 55.2 (steady). All three were marginally stronger than consensus. As solid as they are, none of this is likely to shift the lingering concerns that the ECB has about persistently low wages growth and inflation ahead of this week’s meeting and thus baulk from giving clear guidance on ending QE in September. But it will bolster the view of continued strong growth laying the foundation for a pick-up in inflation to follow.

Just after we go to press, the RBA’s Chris Kent is speaking on “The Limits of Interest-Only Lending” at a housing industry breakfast (7.50am). But the big one today is the CPI. With the AUD already making new lows this morning, it seems it will be more price sensitive on the downside, whereas an at or slightly above consensus print might hold back the tide for now, lending at least some short-term support unless its material enough for the RBA to think twice about the inflation outlook. That would take something like a 0.6% average print on the two underlying measures. A print around that level would deliver some confidence to the RBA that inflation is one its gradual rise path to inside the target range and spark up market RBA rate change pricing.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.