We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

The markets didn’t react positively to the UK opposition leader’s Brexit speech – infact, they hardly reacted at all. Phil Dobbie asks NAB’s Tapas Strickland in London about the latest chapter in the saga.

https://soundcloud.com/user-291029717/iron-strong-corbyn-confused-powell-on-the-way

US equities are having another solid day, boosted by further declines in UST yields while the VIX index continues to decline. The big dollar is little changed with CAD and MXN under pressure as NAFTA talks resume. Position squaring is probably one factor at play as the market awaits Fed Chari Powell first public appearance.

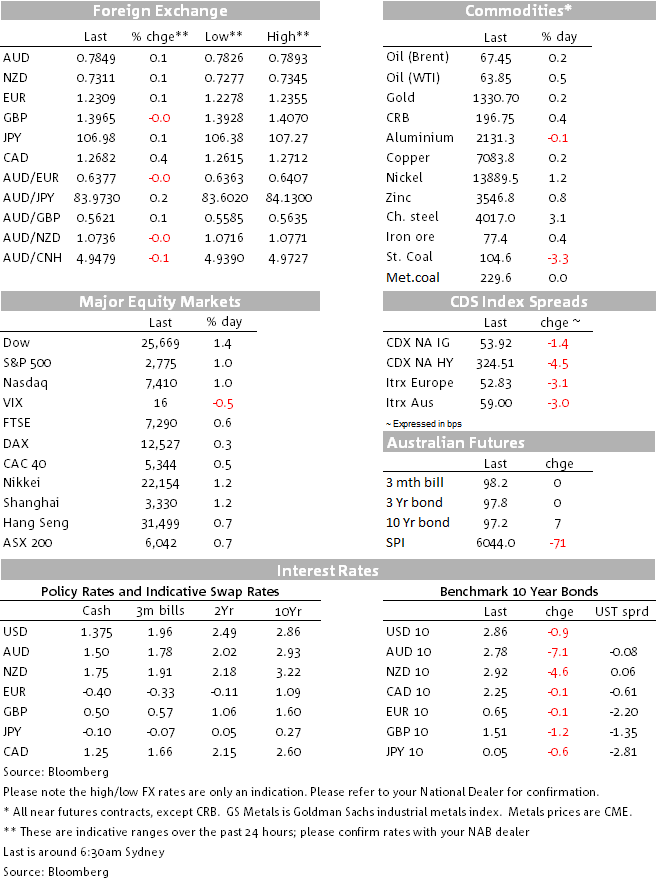

After solid gains on Friday, US equities have started the new week on a strong footing with the Dow currently up 1.62% while the S&P500 and NASDAQ are both up close to 1.20%.Meanwhile, equity volatility has continued to ease with the VIX index currently at 16.54, a week ago the index was at 20 and early in February it traded to an intraday high of 50.

Back then a spike in UST yields was the trigger for the rout in US equity and now the decline in UST yields appears to be the main driver for the equity rebound. 2y and 10y UST yields are now on their third consecutive day of decline with the 10y note currently trading at 2.865%, after trading to an intraday low of 2.82%. Last week Wednesday, when US equities were on their knees, 10y UST were trading at 2.95%. Front end yields have also pared back most of last week’s move with the 2y tenor currently trading at 2.225%, 1bps down on the day.

In index terms the USD is little changed over the past 24hrs and both DXY and BBXY indices are trading on the upper half of their past month range. NOK is the top performer in G10, up 0.22%. Oil prices might have been a supporting factor for NOK with both WTI and Brent up around half a percent, but the rise in oil prices were no help for the CAD with Loonie the big underperformer over the past 24hrs, down 0.54%. The resumption of NAFTA talks amid a tense negotiating environment has not only weighted on the CAD, MXN has also come under pressure with the peso down 0.73%.

The AUD is little changed over the past 24hrs, the pair currently trades at 0.7850 almost exactly where it was this time yesterday. Overnight the Aussie traded to an intraday high of 0.7893 boosted by news that China’s biggest steel producing region plans to extend its winter production curb. China’s top steelmaking city of Tangshan has proposed new restrictions on production once the current curbs expires in March in order to improve air quality. News reports suggested that the curb in production is likely to incentivise steel mills to concentrate on higher valued-added steel products amid their higher profit margins, if so this would be a positive for higher quality ores that Australia produces. Overnight iron fines 62% hit a 10 month high of $79.15, but later in the session the initial spike was retraced with the AUD following the move.

The NZD moved from around 0.7280 at lunchtime yesterday to a high of 0.7345 overnight, but it has since returned to 0.73. Our BNZ market strategist notes that the NZ trade balance is due for release this morning and BNZ expects strong growth in both exports and imports to generate a monthly trade deficit of $214m (vs. median expectations of 0). There shouldn’t be more than a fleeting market reaction to the data.

The Euro is also little changed seemingly unfazed by comments from ECB President Draghi before European Parliament lawmakers. Draghi said further declines in unemployment and a pickup in wage growth should boost consumer-price growth, but that there is still a way to go. While the euro-area economy is enjoying its fastest expansion in a decade, data this week will likely show inflation continues to undershoot the ECB’s target of just below 2 percent. Draghi also singled out the recent volatility in financial markets, including in the exchange rate, which he said deserves close monitoring with regard to its possible implications for price stability.

In the UK, Labour leader Jeremy Corbyn officially announced the party’s intention to remain a member of “a” customs union after leaving the EU. He said “I appeal to MPs of all parties…to join us in supporting the option of a new UK customs union with the EU.” A small number of pro-EU rebel Conservative MPs have tabled an amendment to the government’s Customs Bill (to stay in the customs union) and in so doing have effectively sided with the opposition Labour’s own policy. Given Theresa May’s slim Parliamentary majority, one possible outcome is a government defeat in the bill, which may then trigger a no confidence vote in the government. While we acknowledge the risks, we remain constructive on GBP for now as we expect a transitional arrangement to be agreed over the coming few months. Despite UK politics remaining in flux, GBP wasn’t overly affected overnight, and it might be a case of the market being fatigued by the constant barrage of Brexit-related headlines. Theresa May sets out her ideas for post-Brexit relations on Friday

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.