Coming in for landing in a heavy cross wind

Insight

To some, The Beatles’ Helter Skelter planted the inspirational seeds for heavy metal.

https://soundcloud.com/user-291029717/volatility-reigns-is-the-ride-over

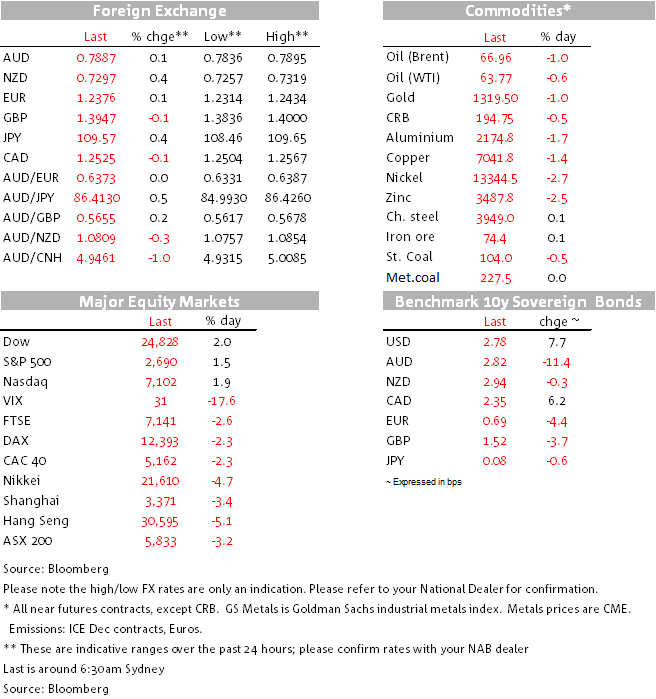

To some, The Beatles’ Helter Skelter planted the inspirational seeds for heavy metal. Personally I have no idea, but like Paul McCartney once described it, I think it is certainly the “”loudest, nastiest, raucous and dirty thing” the Beatles ever wrote. Helter Skelter is also quite a suitable description of the ongoing equity price action. After sharp drops in Asia, European equities cratered overnight and following a big decline at the open, US equities have rallied in the past few hours and look set to close up near 2%. Meanwhile , the VIX index briefly traded above 50 and remains elevated at 31,the USD has pared back all the gains seen at the start of the overnight session and after an initial rally UST 10y yields are higher relative to Sydney’s close.

After sharp equity losses in Asia which saw the Nikkei close down 4.73%, Europe followed a similar line with all major regional indices closing over 2% lower. US Equity futures suggested a similar outcome was in line on for US equities, but after a sharp decline at the opened US indices have rallied into the close. The VIX index has also endured a bit of a roller coaster ride, climbing just above 50 before midnight, sinking to 22 just before 2am and now it has stabilised around 30.

Looking back in history the jump to 50 in the VIX index is pretty remarkable, indeed since 1990 there have only been 9 periods where the VIX has traded above 40. The index is now back at 30, so the move above 50, at this stage at least has been very brief. Notably too, although events over the past few days have also seen sharp rises in bond and currency volatility, unlike equity vol these spikes have not reached historical extremes. The Move index, for instance, is currently at 60, its highest level since May last year and nowhere near the highs of 92 reached in mid-2015 or the 208 level reached at the peak of the GFC in 2008. A similar story can be seen in currency volatility, the CVIX index has risen a point in the last month to 8.7 currently, in 2015 it reached levels just above 11 and during the GFC the index traded to a record high of 23.15.

So the current equity rout which appears to be reversing as we type, has been relatively contained with limited spill over effects onto other asset classes, this probably helps explain the remarkable stability of traditionally risk sensitive currencies such as the AUD and NZD. NZD is the best performing G10 currency over the past 24hrs, after trading to an overnight low of 0.7257, the kiwi now trades at 0.73, up 0.55% over the past 24hrs. The rise in US equities over the past few hours and a solid dairy auction appear to be the main factors behind the flightless bird’s performance. The GDT Price Index rose 5.9% and a rise in prices was recorded across the board including wholemilk powder, skim milk powder, cheese and butter all up between 7% and 8.

Softer retail and trade figures weighted on the AUD during our Asia session yesterday and the initial softness in equities overnight saw the AUD trade to an overnight low of 0.7836. But just like the kiwi, the improvement in risk sentiment has helped the pair recover all the lost ground and some over the past 24hrs. AUD now trades at 0.7891, up 0.20%. Yesterday the RBA left rates on hold at 1.50% now steady for 18 months and reaffirmed the current policy setting. Our economists noted quite a few wording changes but the messaging of a gradual increase over time in inflation toward target and growth to pick up over the next couple of years to average a bit above 3% has not changed. on the AUD the only distinction is the reference to the AUD on a trade weighted basis rather than just the Australian dollar. Thus emphasising that much of the recent moves in the exchange rate have been USD related while on a trade weighted basis the AUD is little changed. Meanwhile, the important line on the currency was left unchanged. ‘An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast’.

So the recovery in risk sentiment has seen the USD give back most the gains recorded in the earlier part of the overnight session, DXY is essentially unchanged relative to Sydney’s closing levels ( currently at 89.59). After trading to an intraday low of ¥108.46, USD/JPY is now at ¥109.46 and a similar pattern can be seen for the euro, the pair currently trades at 1.2383, after dipping to a low of 1.2314 just after 2 am this morning.

As we are about to press the send button, 10y UST yields are currently trading at 2.78%, up over 10bp from yesterday’s low in Asia, but still 10bp below Monday’s high. Meanwhile, commodities appear to be lagging the improvement in sentiment with most of the complex trading in negative territory. Oil prices are down between 0.9% (Brent) and -0.3% (WTI), gold is 0.6% while copper and aluminium, are down 1.4% and 1.7% respectively . Iron ore is unchanged at $74

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.