A private sector improvement to support growth

Insight

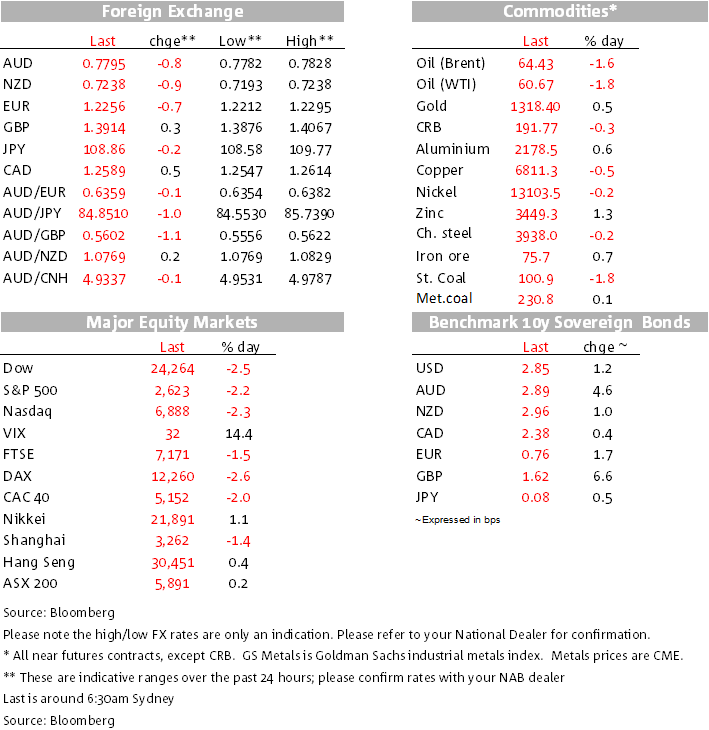

Stocks fell across Europe and the US overnight.

https://soundcloud.com/user-291029717/rocky-road-as-share-indices-crumble-again

It’s back on. Just when it seemed safe to go back out, risk markets are on the defensive again, with European equities down 1½%, but this time rising bond yields have re-emerged as the catalyst as they were at the end of last week on that higher than expected US average earnings print in the payrolls report. As we go to print in the last hour of trade, US Treasury yields while off their intra-day highs, are still up net for the day with the Dow down by ~600 points (>2%). The only data of note overnight has been US weekly jobless claims that remained low at 221K for w/e 3 Feb.

The AUD/USD is trading back around 0.78 this morning, having tested below the figure overnight and again this morning. RBA Governor Lowe was speaking last night and delivering the message that while the next movement in rates is likely to be up, he intimated that he’s certainly in no immediate rush. He noted that the floating currency buys time for the RBA to not move lock-step with other central banks (the RBA cash rate reached a less-low emergency level) and they look for “gradual” progress in reducing unemployment and getting inflation return to the midpoint of the target range. He went on to say that “ ….the Reserve Bank Board does not see a strong case for a near-term adjustment in monetary policy”. In the end, their policy assessment will rest on the data and that is what will drive the RBA Board. In terms of the RBA outlook for growth, unemployment, and inflation, more will be revealed in this morning’s quarterly Statement. Lowe said last night that “these forecasts will be largely unchanged from the previous set of forecasts”, so a likely muted/minimal reaction is likely today.

Aussie traded down to the 0.7780/85 area in the immediate aftermath of the speech before recovering but is again looking again below the figure again with brittle US markets. Yesterday’s Chinese trade figures had little impact, revealing a much larger y/y surge in Chinese imports (30% in CNY terms, 36%.9% in USD terms and including strong iron ore imports), symptomatic of continuing internal Chinese economic growth. Note that there is no January Chinese activity reports, the first not coming till the combined Jan/Feb figures next month.

Currencies that out-performed the USD overnight included the “safe haven” yen and the Swiss Franc. Another swimming against the tide was Sterling, courtesy of the BoE and Governor Mark Carney. The BoE left rates on hold as expected, voting 9-0. So no surprises there, but the market reaction came in the messaging and forecasts. Sterling spiked higher by two big figures (it was weakening slightly into the announcement) after BoE Governor Carney noted that “monetary policy would need to be tightened somewhat earlier and by a somewhat greater extent over the forecast period”, concerned about inflation risk. The BoE upgraded their growth forecasts for the coming few years a bit, mainly due to the more positive global environment. And it continued to highlight the lack of spare capacity in the economy, with the unemployment rate at a multi-decade low of 4.3%. The market now prices a 75% chance the BoE will raise rates at its May meeting (from 50% beforehand). The GBP has since fallen back, but it remains slightly up on the day against the USD.

Bill Dudley (NY Fed President so a voter) was out on the wires. He described the stock market sell-off seen to-date as “small potatoes”. Dudley added that four hikes this year were possible if the economic outlook strengthened. Philadelphia Fed President Harker said the correction hadn’t changed his economic outlook and noted that broader financial conditions were still highly accommodative. Uber-dove Fed President Kashkari noted that bond markets are signalling that inflation is well within control while in an amusing tweet said “stick with the dollar, yen and leave bitcoin to toy collectors”. He doesn’t see it as a currency but as a novelty.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.