Total spending grew 0.9% in June.

The Turkish Lira continues to fall.

https://soundcloud.com/user-291029717/a-fowl-monday-as-turkey-spreads

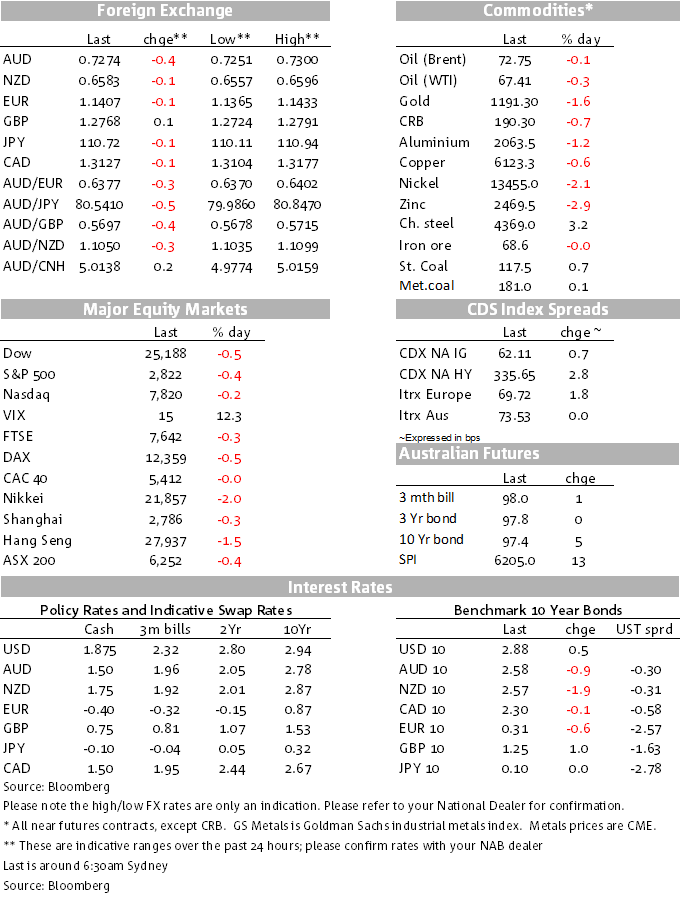

Given the start that the local market had yesterday kicking the global week, it’s been relatively contained for global markets overnight in terms of contagion. Equities have been softer, as have base metals (with oil marginally and gold) and there’s been some widening of credit spreads, but it’s been a relatively orderly market and with the Turkish lira still trading barely above its lows.

The Dow has closed down 0.5%, the Eurostoxx 600 index by 0.25%, the Eurostoxx bank index by 1.18%. The Turkish stock market closed down 2.38% and Turkish 10 year bonds up 52bps to 21.53%. (Turkish CPI in July was 15.85% after averaging 7.8% in 2016, increasing to 11.1% average last year; it runs a current account deficit running at 5.9% of GDP.)

The USD remains in the ascendancy, but it has not extended its gains against the majors. The AUD/USD was testing 0.7250 in early Asia yesterday, and although it remains not far above that level as the NY session comes to an end (at around 0.7270/75), it has not made new lows overnight. It’s been trading more in a sideways pattern.

To recap yesterday, the Turkish lira continued where it left off last week, opening 11% lower in illiquid conditions during the Asian session and taking the currency to a new low. This triggered a ripple effect, with the South African rand suddenly spiking 10% lower in thin conditions, although it subsequently reversed most of this move to be down only 2.4% on the day.

The Turkish central bank announced overnight it was cutting bank reserve requirements (intended to free up $6b of USD liquidity) and pledged to “take all necessary measures” to stem the crisis, although it refrained from announcing a rate hike. Meanwhile, the Turkish banking regulator announced restrictions on TRY FX swaps to make it harder for speculators to short the currency. These are likely to be only short-term fixes however, and until there is a clear and credible policy response from Erdogan and the central bank, the TRY will remain under downward pressure. (See also the call from the Bundesbank for stronger action, mentioned below.) Also as my BNZ colleague Nick Smyth has reported this morning, investors might well be worried about the possible imposition of capital controls (despite the Finance Minister’s claims these are not on the agenda) and thus likely to want to exit while they still can.

The Turkish lira remains not far above its lows of early yesterday, after the measures to provide currency support. (The USD/TRY is trading at around 7, having been around 4.8 to the dollar only a month ago.) Seeking to calm some market nerves, the Bundesbank’s Wuermeling said that the ECB hasn’t seen the need for Turkey bank risks meeting and not to “over dramatise” the risk of Euro shoot. Mind you, in the same breath they were also urging Turkey to take “bold action” to stop a spiral.

Italy has also reappeared on the market’s barometer, with pressure on some Italian (and other European) bank stocks, presumably from some concerns over exposures to Turkey, but also Italian political/budgetary uncertainty. Claudio Borghi, the head of Italy’s Lower House Budget Committee has called for ECB support for Euro periphery economies to defend speculative attacks. “There cannot be a system at the mercy of market movements without any shields by the central bank”, he said Monday. “Nowadays there is a system that has a residual amount of quantitative easing, but with everybody knowing that this is being phased out and will come to an end soon.”

Italian 2 year bond yields jumped 16.7bps while 10 year yields rose 10.8bps. 10 year bond yields in Spain (4.8bps), Portugal (+6.8bps), and Greece (+6.7bps) were higher on the day when German bunds were virtually unchanged and US Treasuries likewise, the 10 year at 2.8768% (+0.36bps).

There were no economic reports of note overnight. Ahead of its July economy releases today, China yesterday released its new yuan lending volumes, aggregate financing, and money supply report. Banking yuan loan volumes printed at 1.45tr, above the 1.275tr expected, suggestive of some easing in credit conditions. Aggregate financing – a measure of non-bank/alternative financing – though was a little softer than expected. The market is looking for somewhat stronger July readings for Retail Sales and Industrial Production today and steady Fixed Assets Investment.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.