Total spending grew 0.9% in June.

Whilst China has promised to retaliate against the US tariffs, it hasn’t gone as far as it could.

https://soundcloud.com/user-291029717/aussie-wins-because-of-or-despite-tariff-uncertainty

I won’t do that to you, Won’t do that to you – Robbie Williams

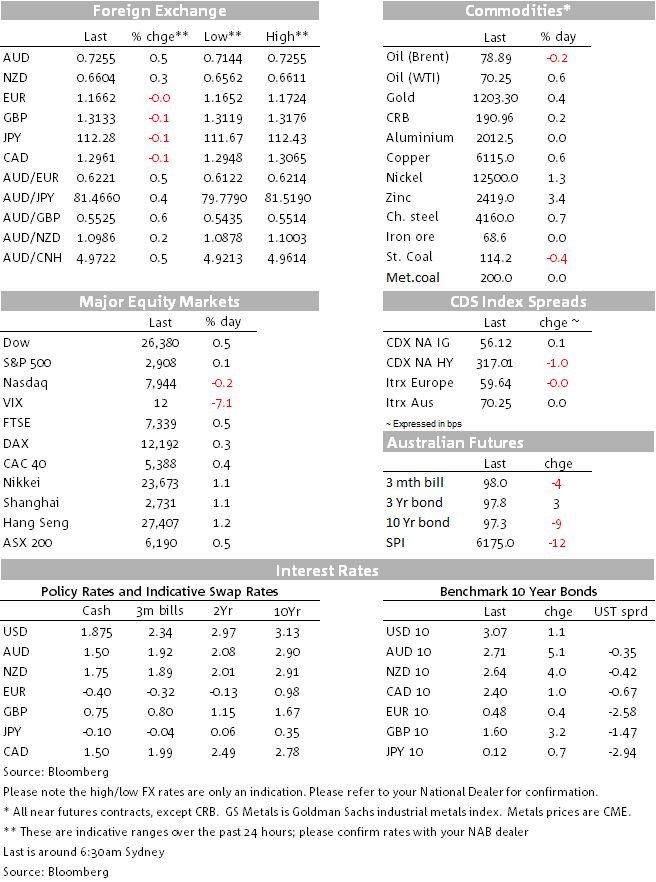

It has been a modestly positive night for risk assets, higher UST yields boosted US banks, but US Tech shares underperformed. The USD is little changed in index terms while EM FX recovery continues helped along by Chinese premier Li Keqiang promise not to devalue the yuan. AUD and NZD benefit from the EM recovery with a paper from the RBA suggesting he AUD TWI could rise in a widespread trade war further helping sentiment for the AUD

The USD is little changed in index terms with DXY now trading at 94.53, close to levels seen this time yesterday. That said a closer look at G10 currencies shows a distinct outperformance by the most risk sensitive pairs with the AUD leading the gains (+0.64%) followed by the NZD (+0.52%), SEK and CAD (both up +0.40%). The improvement in EM sentiment appears to have been the main drivers for the gains in these currencies helped along by comments from Chinese Premier Li Keqiang yesterday afternoon that China won’t devalue its currency to stimulate exports.

The Premier’s comments of course need to be put in the context where the CNY has depreciated just under 10% since US trade tensions began around May/June this year. The Premier’s comments are encouraging as they indicate that China won’t actively use its currency as a weapon in its trade scuffle with the US, but as we have seen in recent months this doesn’t necessarily mean that China will prevent the CNY from weakening if market forces push the currency lower. Note too that the US Treasury is due to release its semi-annual FX report in October, so avoiding a lower CNY ahead of the report is probably a good idea.

AUD traded to an overnight high of 0.7275 and NZD traded up to 0.6623 and although both antipodean currencies have eased a few basis points in the past couple of hours, the upward trend established since September 12 still remains intact. A short squeeze in both currencies amid an ease in EM concerns is definitely one factor at play and based on our fair value models both currencies still look cheap, suggesting the recovery could extend for a bit longer. Of course an escalation in US led trade tension would spoil the party with President Trump threat to kick start the process for tariffs on an additional $263bn a palpable risk.

Further helping sentiment for the AUD, prompted by a freedom of information request, the RBA released an internal paper suggesting the AUD TWI could actually appreciate in a worst case trade war scenario of the US applying 20% tariffs on all goods imports from all countries then Australia could be less exposed than other economies that rely more on global trade flows and manufacturing (see RBA FOI Report). Worth stressing that the assessment is on the AUD TWI and it is over an extended period of time which includes the view that “GDP would then fall by an additional 2.5 %. A lower cash rate could largely offset these effects in the long run.”. We think that in an extreme trade war scenario the AUD/USD will initially fall abruptly amid a souring in risk sentiment and downgrade to global growth, with recovery eventually ensuing as other countries more exposed to trade will likely suffer more.

CAD also managed to perform overnight despite disappointing NAFTA news. Time is ticking down to get Canada on board with a new NAFTA deal before the critical end-September deadline and sources suggest that a deal is unlikely to be reached this week. Sticking points include the dairy sector and dispute resolutions and sources say that Canadian officials are warning that they’re prepared to see the next deadline pass if they don’t get an agreement they can live with.

GBP punched higher, up through 1.32, after UK inflation data came in stronger than expected, adding to the chance of a BoE rate hike by May next year. GBP then unwound all its gain after the Times reported that UK PM May is said to reject Barnier’s improved Irish Brexit offer. Later, an official from PM May’s office confirmed that the UK can’t accept any Brexit offer from the EU that treats Northern Ireland as a separate customs territory. The pair now trades at 1.3144 and focus turns to EU response to PM May’s Brexcit presentations (more below).

Euroepan equities closed higher across the board, but US equities had a mixed night. US Banks led the gains in the S&P500 helped along by a steepening in the US curve, but US tech shares traded lower with the NASDAQ down -0.08% not helped by 1.5% decline in Microsoft shares after a dividend hike disappointment

The US Treasuries curve continues to push higher, with the 10-year rate reaching 3.09% overnight, a four-month high. This is being driven by increased Fed rate hike expectations. Market pricing for Fed rate hikes next year has ramped up over recent days so that two full hikes are now priced through 2019 in addition to high chance of two further hikes priced for the remainder of this year. This has moved the market closer to the Fed’s implied median three rate hike projection for 2019.

Another mixed night in commodities, Zinc jumped over 3%, but lead declined 2.4%. Meanwhile most other commodities were little changed.

US housing starts rose 9.2% in August, with the bulk of the gains coming from a 27.3% rise in multifamily starts. Single-family starts underwhelmed with a 1.9%increase. Building permits fell to 1229K from 1303K, below the 1310K consensus; we had 1300K.

UK August Inflation was higher than expected with Headline of 2.7% y/y (2.4% expected) and Core of 2.1% (1.8% expected). Much of the beat came from recreation, culture and clothing which can be volatile at times

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.