Online retail sales growth slowed in May following a fairly strong April

Insight

The US Senate on Friday failed to muster the 60 votes necessary to pass a stop-gap funding measure that would have averted the partial government shutdown that instead went into effect at one minute past midnight on Friday.

https://soundcloud.com/user-291029717/a-shutdown-a-coalition-agreement-and-a-strong-aussie-dollar

The US Senate on Friday failed to muster the 60 votes necessary to pass a stop-gap funding measure that would have averted the partial government shutdown that instead went into effect at one minute past midnight on Friday. It was not just Democrat opposition that produced the failure – several Republican Senators also crossed the floor to oppose the motion. So even if President Trump decides to adopt the ‘nuclear option’ allowing for a simple majority in the Senate to approve a spending bill, there is no guarantee this will yield a positive outcome. Attempts by Democrats to link Deferred Action for Childhood Arrivals (‘DACA’) into the spending bill, while the President insists spending and immigration issues should be kept separate, continues to be the obstacle in terms of a bipartisan deal to keep – or now rather re-open – the government.

At time of writing, a fresh vote has been scheduled for 1am Washington time Monday morning (that’s 7pm this evening AEDT) so those of us watching screens are going to be subjected to a minute by minute barrage of red headlines out of Washington throughout the day.

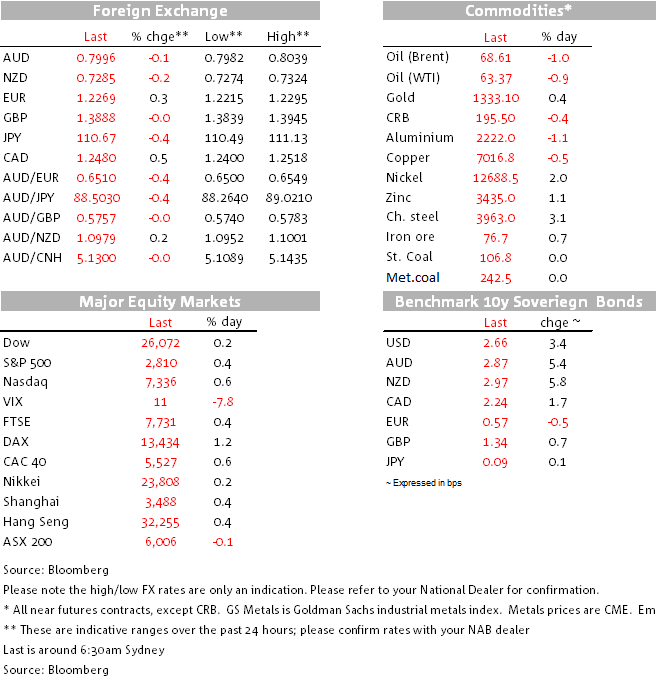

Markets had been travelling last week with an expectation that a shutdown would be avoided. Now that it hasn’t (and assuming it still hasn’t by tonight) it’s hard not to believe this will accentuate the weaker US dollar theme that has been prevalent so far in 2018 and is the main reason the Aussie dollar has poked it’s had back above 80-cents having fallen as low as 75 cents last December. The caveat here would be if risk sentiment suffered a material and sustained knock (back in October 2013 during the last shut-down, the VIX did jump from around 15 to above 20, though the AUD came to no harm whatsoever).

As far as economic impact is concerned, the October 2013 shutdown lasted 16 days and was reckoned to have knocked about a quarter of a percent of US growth (much of which was subsequently recouped). Markets are likely to hold the view this will latest shut-down will again be a short-lived affair, though we’d warn than second guessing US ( indeed global) politics has been a losing strategy ever since the June 2016 Brexit referendum.

The other main development since we went home on Friday has been the weekend vote by Germany’s Social Democrat Party (SPD), by 362-269, in favour for a new Grand Coalition government with Angela Merkel’s Christian Democrats (CDU). This will ultimately have to be ratified by the entire party, but should be a formality. The Euro has jumped by half a cent or 0.4% at the market re-open (a move that has so far at least not lifted other currencies against the US dollar).

The British pound is also stating the week firmer, supported by some fairly friendly comments from French President Macron (in the UK) about a Brexit deal for Britain that would definitely border on the ‘soft’ side of the spectrum of possibilities (while insisting that any deal could not be such that other countries could feel incentivized to follow Britain down the EU exit road). Latest UK unemployment data and Q4 GDP – latter seen at 0.4% – are both due this week and will have some bearing on the near term course of GBP.

In other markets, US equities were unfazed on Friday at the looming prospect of a government shutdown, nor too by US bond yields at 10 years finally breaking up through the 2.63% range tops that have been in place since late 2014. Again though, US dollar support from a rising US yields environment is still lacking. Both the S&P500 and NADAQ closed at new record highs. In commodities, oil and precious metals both fell back while industrial metals were mixed. Iron ore added 50 cents but at $76.68 is still a just over a dollar back from its 11th January high of $77.72.

The AUD dropped back below 0.80 into Friday’s New York close, but is threatening to move back above this morning.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.