Online retail sales growth slowed in May following a fairly strong April

Insight

The US dollar hit new highs on the back of a falling Euro and Pound.

https://soundcloud.com/user-291029717/dollar-hits-highs-on-scary-european-growth-numbers

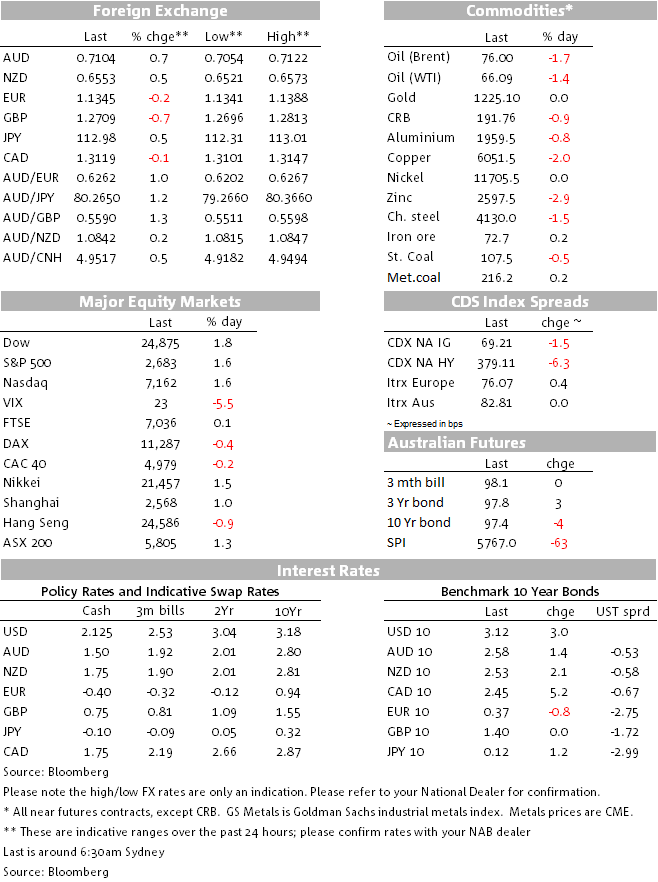

USD indices made new highs overnight mostly reflecting weakness by European currencies supported by solid US consumer confidence and faltering EU GDP growth. European equities closed mixed and US equities bounced into the close. Against a backdrop of USD strength, AUD and NZD outperformed boosted by President Trump comment of a great deal with China. UST yields closed marginally higher reflecting the uptick in US equities.

USD indices have recorded a second consecutive day of gains, more than reversing the losses recorded on Friday. The broader BBDXY index (@1208) is 0.33% on the day and now trades at levels not seen since mid-May last year. Meanwhile DXY has finally traded through its mid-August year to date high and now trades at 97.00, up 0.43% over the past 24 hours.

USD strength overnight has been mainly driven by weakness in European currencies while a solid US consumer confidence reading was also supportive. The euro was under pressure overnight following the release of a softer than expected Eurozone GDP, the advance Q3 GDP print revealed growth at just 0.2% for the quarter, a lot weaker than the 0.4% expected by the market. Growth in annual terms also disappointed at 1.7% y/y against 1.8% expected.

Meanwhile US Consumer confidence printed at an 18 high overnight further reinforcing the notion that US GDP growth drivers remain solid for now while more question marks are raised on other major economies growth prospects. The soft EU Q3 GDP reading comes on the heels of soft EU PMI readings and a disappointing IFO German survey, add to that Brexit uncertainty and Italy’s budget battle with Brussels and it is not hard to see why the market appears to doubt ECB president Draghi that the EU growth slowdown is only temporary. After trading to an overnight high of 1.1388, the euro now trades at 1.1346, a couple of bps above its overnight low.

No Brexit news also appears to be weighing on the pound as the clock keeps on ticking and politician edge ever so closely towards a now deal. GBP is the big G10 underperformer, down 0.73%, the pair briefly traded sub 1.27 and now trades at 1.2711. S&P overnight noted that the risk of a no-deal outcome had increased sufficiently to become a ratings consideration, and the ratings agency forecast a moderate recession in the event of no-deal.

Despite the broader backdrop of USD strength, the NZD and AUD have moved higher over the past 24 hours. Yesterday afternoon, President Trump gave an interview with Fox News in which he predicted a “great deal” with China on trade. While Trump added that he didn’t think China was “ready” to reach a deal yet, the NZD and AUD immediately moved higher on those comments and both currencies have extended those moves a bit further in the overnight session. The AUD is up 0.6% to 0.7106 over the past 24 hours while the NZD is up 0.5% to 0.6552, with market positioning (squaring of short NZD and AUD positions) likely exacerbating the moves higher.

Another dynamic for the AUD to consider is the impact equity FX hedging could be having on the currency this month. The fall in US equities this month (S&P 500 currently -7.94%) raises the question of whether Australian fund managers will be significant sellers of AUD in order to rebalance their portfolio hedges (i.e. buying back US dollars and selling AUD in order to push hedge ratios back closer to benchmark). To some extent, this is likely to have been occurring during the course of this month, but could be even more evident at month-end. Countering this argument, the AUD traded to a new multi-year low last week and for some fund managers this could be the trigger to lift their FX strategic hedge ratios. Either way the last day of the month is likely to be a busy day for the AUD.

European equities closed mixed and US equities bounced into the close with the S&P500 adding 1.5%, a day after dropping 0.7% raising the prospect of moving into correction territory. All 11 sectors in the S&P 500 traded higher, led by gains in energy (+2%) and communications (+1.8%) shares. The NASDAQ climbed 1.3%.

After the bell Facebook fell about 1% following its earnings report revealing revenue came in pretty much on the screws ($13.73bn vs. $13.8bn and analysts’ range of $13.12-14.09b), the share is now back to black (+1.9%)

US Yields are a little bit higher reflecting the gains in US equities. The 10y UST yield now trades at 3.113%, up 2.8bps on the day

Metals and oil prices had a night to forget, both down around 1.6%, but copper and zinc where the big losers down 2.55% and 2.75% respectively.

US Conference Board’s index of consumer confidence rose to an 18-year high of 137.9 in October, above the consensus, 135.9. The elevated number is suggestive of solid spending growth ahead.

US S&P/Case-Shiller 20-city home price index was +0.1% m/m in Aug in line with consensus, The yoy change is still solid at 5.5%, but down from the high 6.8% in March.

BoC’s Governor Poloz out an hour or so ago in parliamentary testimony, re-iterating the message from last week’s BoC meeting that rates need to rise to neutral, ted to be 2.5-3.5% (1.75% now). Market currently fully priced fro next move in January

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.