NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

A full Senate vote to ratify the deal struck a few hours ago to re-open the US government is scheduled for 4:30pm Washington time (8:30am AEDT).

https://soundcloud.com/user-291029717/us-shutdown-is-over-davos-has-started-imf-ups-forecast

Overview:

A full Senate vote to ratify the deal struck a few hours ago to re-open the US government is scheduled for 4:30pm Washington time (8:30am AEDT). It’s now a formality, but does nothing more than kick the can two weeks down the road (until February 8). Avoiding a repetition of the last few days is contingent on a deal being strict on the fate of the so called ‘Dreamers’ satisfactory to both President Trump and enough Democrats such that the Senate will agree to a somewhat longer lasting funding bill.

More significant will be what happens when the debt ceiling is hit, likely in March. It was the failure to lift this in a timely manner in 2011 that led to S&P expressing a loss of faith in the US’ ability to get its fiscal affairs in order and to a downgrading of the sovereign to AA+ from AAA.

The prospect of a shutdown didn’t faze US equity markets on Friday, but news of a deal to re-open the government has predictably been offered as an excuse for yet new record highs being chalked up by the S&P and NASDAQ. In truth, the better ‘excuse’ is the ongoing lifting of earnings expectations by stock market analysts, driven in large part by assessment of the tax deal and, in the case of many multinationals, ongoing slippage in the US dollar.

The IMF has been out with a global growth upgrade in front of the World Economic Forum about to kick off in Davos and which will hear the latest vintage of President Trump’s vision to Make America Great Again. What he, in conjunction with his Commerce Secretary Wilbur Ross, decide to do, or not do, vis-à-vis trade protection measures – specifically on steel and aluminium and where Commerce department findings are reportedly sitting on the President’s desk – has much more potential to move markets than anything that comes out of Davos itself

Th IMF has lifted its 2018 global growth forecast by 0.2% to 3.9%, the upgrade is led by the US (a 0.4% lift to 2.7%) and Eurozone (+0.3% to 2.2%). The tax deal is largely responsible for the former, but the IMF sees the longer term impact of the deal as growth-negative. The IMF makes the familiar call for leaders to use the current upswing to ‘mend the roof’ and make growth more inclusive. It warns of risk to the growth outlook from, specifically, trade protectionism, geopolitics or a significant market correction, noting “rich asset valuations and very compressed term premia”. It also warns of risk that the Fed raises rates faster than expected leading to tighter financial conditions around the world.

The Australian government has already been out this morning praising the IMF’s revised global growth estimate, saying it supports its own optimism for stronger Australian growth.

One country not to feel the IMF’s love is Great Britain, which has suffered a small growth downgrade (unchanged at 1.5% in 2018 and -0.1%, also to 1.5%, for 2019). Brexit related woes are to blame of course. The FX market response is to push the pound to its best level since the referendum, now within a whisker of $1.40 against the US dollar. French President Macron’s comments about the possibility of a ‘special deal’ for Britain, during his weekend visit, are part of the story here.

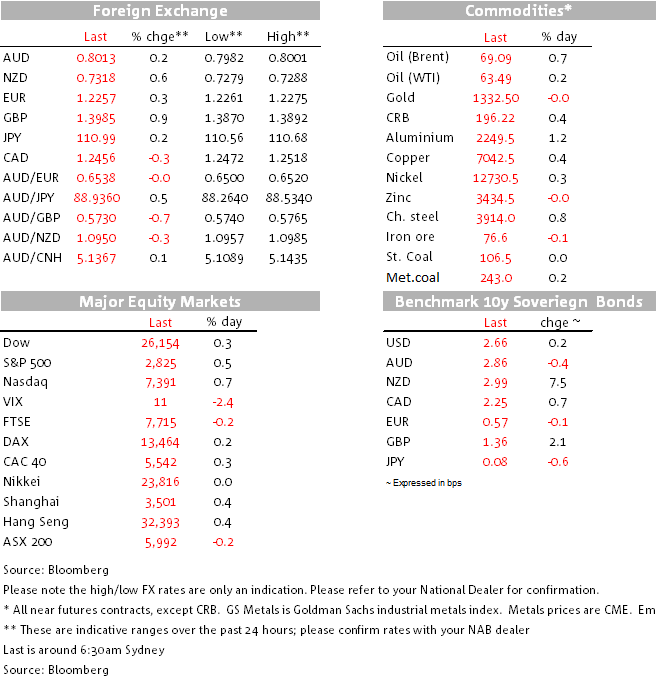

The AUD was sitting just beneath 80- cents when we went home yesterday and sits just above this level this morning while marginally weaker against most other major currencies. It doesn’t look like budging too far from 0.80 for the next little while at least. Commodity markets have had a mixed night but are mostly stronger, with oil still benefiting from OPEC and Russia’s weekend commitment to hold its lower output level through 2018.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.