Online retail sales growth slowed in May following a fairly strong April

Insight

Rising commodity prices, stalling inflation, a flattening curve and cautious Canadians

David de Garis talks Phil Dobbie through a busy day for market news, starting with a big jump in oil prices.

https://soundcloud.com/user-291029717/rising-commodity-prices-stalling-inflation-a-flattening-curve-and-cautious-canadians

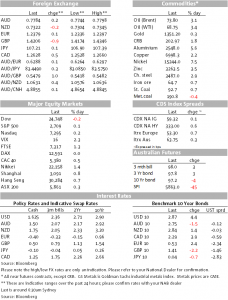

It’ been an overnight session marked by a very solid night for commodity prices. Oil prices pushed higher, to levels not seen since it was on the way back down in 2014 from the surge then in US tight oil supplies. WTI and Brent oil are both up over 3% and up $2.30/$2.25/bbl, this time from the weekly US DoE report showing declines in US inventories of crude and refined products across the board. Stricter compliance from OPEC also seems to be playing out with OPEC meeting at the end of the week. The global/US growth story has very likely been a contributing factor, with both oil prices and US supply continuing to rise without any noticeable change in US inventories.

While the rise in oil was chunky, price gains of 3% looked modest next to the price action on the LME overnight and Dalian iron ore futures yesterday. Much of the talk attributes the gains to spill-over effects from the Russian sanctions. Ally prices rose 5.49%, while nickel jumped an eye-glazing 7.46% as traders scrambled to cover positions. Copper was up a rather pedestrian 2.11%, pushing up through $7,000/t, nickel to $15275/t (+1,060 on the day!). After having tracked lower in recent weeks, Dalian iron ore jumped 4.26% yesterday, supported also by Chinese steel rebar futures, up 1.16%. Be aware also that iron ore and coal markets are no longer the strictly over-the-counter markets they were some years back but are now very active in the derivative space with speculation from the likes of everyday/retail Chinese investors. Not to be left out, gold has also edged higher.

The AUD/USD has been only somewhat higher and we expect that if this morning’s NZ CPI and AU employment numbers play out as we expect (lower NZ inflation; strong AU employment), it should be supportive for the AUD/USD and the AUD/NZD over the course of this morning. One Aussie cross that has already moved overnight has been AUD/CAD on the back of caution from the Bank of Canada over their growth outlook. As expected, the BoC left rates on hold at 1.25%, but short term Canadian yields eased back on reduced expectations for higher rates at upcoming meetings. Governor Poloz spoke of headwinds preventing a full recovery (e.g. resolution of NAFTA uncertainties stymying business confidence) and the market took back three points from the expected pricing for the 30 May meeting from a 56% chance to a 44% chance.

While front line commodity price inflation news has been in the ascendancy, UK’s CPI in March came in less than expectations for both headline and core, headline coming in at 2.5% y/y and core at 2.3%, both missing by two tenths on lower goods inflation as the Pound’s previous fall dissipates from importers and High Street cost lines. Meanwhile, the House of Lords voted in a bill to keep the UK in a Customs Union even as the UK leaves the EU, a defeat for the Government which will now likely kick this rather crumped can even further down the road. AUD/GBP is trading this morning at 0.548, up another ½ a penny over the past 24 hours.

There was no key US data. (That is apart from the weekly oil inventory report.) The Fed released its Beige Book, it company anecdote and regional reporting ahead of the 3 May FOMC meeting. While all Fed districts reported “moderate” or “modest” and positive economic growth, there were understandable concerns on the trade/tariff front from manufacturers, from agriculture and transportation contacts. Jumps in steel and aluminium prices were cited and reported rises seemed well beyond what might have been expected just from tariff effects, one manufacturer reporting pointedly to higher aluminium prices as “threats to American jobs and businesses”. You don’t have to think too long about where those reports were aimed at. Higher fuel costs also had a run in the commentary. Businesses reported tight labour markets and various responses, including increasing pay, overtime, retraining, and automation. The Book didn’t seem to be the horror story at the retail price level, prices rises reported as “scattered”.

Coming up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.