We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Leaders going into G7 seem to be holding their positions firm on trade tariffs and the Iran Nuclear Deal. So much so, it’s unlikely the markets will pay too much attention.

https://soundcloud.com/user-291029717/g7-brexit-north-korea-deal-or-no-deal

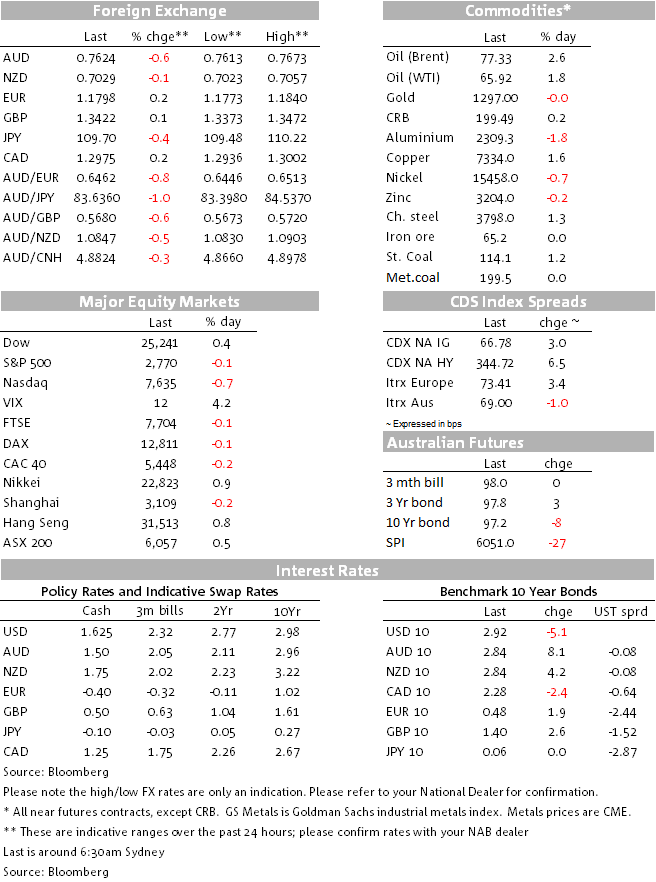

Just when it looked safe to be thinking about the Aussie dollar pushing up though some pretty significant resistance level and potentially advancing back up into the 0.78s, along come the latest Emerging Market ructions to push it firmly back down in the range. Indeed, AUD is far and away the weakest G10 currency in the last 24 hours (down to 0.7625) a day after having made a new six week high just above 0.7675 in the wake of Wednesday’s local GDP report. The Japanese Yen and Swiss Franc are the strongest.

Brazil is the proximate cause of the overnight moves not just in currencies but also in global stocks and equities, where the S&P has just closed (slightly) in negative territory, the VIX has added back almost a point from Wednesday and US Treasuries at 10 years come into the New York close about 5bps lower. The South African Rand, Mexican Peso and Russian Rouble have also been under the pump, ZAR down 2.5% and MXN and RUB both down by just over one percent, versus the 1.6% loss for the BRL.

The latter move brings its loss since the end of April to some 13%. As Rodrigo noted in yesterday’s note and the Morning Call Podcast, there is nothing specifically new about the (ongoing) political and economic travails in Brazil; rather it seems to be more about the momentum established since USD/BRL broke up above its post mid-2016 range highs near 3.50, which led markets to start entertaining the thought of a return to the prior highs above 4.00. The seeming ineffectiveness of initial efforts by BCB, the central bank, to defend the Real, looks to have added to negative sentiment and related capital outflows..

The irony here is that the Institute of International Finance’s latest EM flows tracker published last night showed the daily inflows to EM equity and bonds market since May 31st recording their sharpest upturn since early 2016 (of some $6.1bn). However, over half of that is into China, followed by Korea and Taiwan. Brazil and South Africa have both experienced sizeable outflows (Mexico isn’t included in this data set). Positive flows into EM Asia show up in a firmer ADXY (the Asia EM currency index) this month, to which the AUD is correlated, but as Rodrigo also noted in a recent research note (see The EM Risk to AUD Stability from 25th May) judged purely on the basis of what is happening in global emerging markets, in terms of overall EM FX, bond and equity performance, this does justify lower AUD levels.

While there are no obvious catalysts for an apparent broadening of EM (albeit ex Asia) pressures in recent days, it is valid to speculate that the ECB’s mid-week signalling that the conditions for ending its QE bond buying programme look to have fallen into place, is relevant. We’re not yet talking ‘QT’ as is the case in the US, but another nail in the coffin at least of liquidity expansions from major central banks. Watch this space.

As well as the Mexican Peso, the Canadian Dollar has also performed poorly overnight, albeit not as badly as the AUD. Relations between US Presidents Trump and Canadian Prime Minster Justin Trudeau look to be going from bad to worse in respect of barbs being traded on trade matters, in front to the G7 meeting slated to start in Quebec today and run through Saturday.

In other Trump-related news, the President offered Chinese company ZTE Corp a lifeline, allowing it to continue in business after paying a $1.4b fine and requiring US enforcement officers inside the Chinese company to monitor its actions. At the margin, this eases US-China trade tensions, with no doubt expectations of China offering a quid pro quo in return. This though has further inflamed members of Trump’s own party. Marco Rubio, the Republican senator leading criticism of Mr Trump’s shift on ZTE, immediately lashed out at the agreement, calling it a “very bad deal” and vowing to continue his push for congressional action to block it. Rubio tweeted that “I assure you with 100% confidence that ZTE is a much greater national security threat than steel from Argentina or Europe”.

Economic news overnight has been scant. Very weak German factory good orders data isn’t seen changing the course of ECB monetary policy, where speculation continues to reign of another tweak next week to the Bank’s official policy stance, setting the scene for an end to the quantitative easing programme. EUR weakness post the data was fleeting and the common currency reached an overnight high of 1.1840, continuing to show signs of recovery from the 1.1510 nadir at the height of angst around Italy recently. US weekly jobless claims remain near record lows, and come after the JOLTS report earlier this week shows there are no more job vacancies in the United States than there are unemployment people to fill them. Who need immigration?

GBP trading has been whippy, trading in a 100pip range, as rumours swirled of the potential resignation of UK Brexit secretary Davis. He seriously objected to PM May’s plan to tie the UK into EU customs rules for an open-ended period of time after the country leaves the bloc next March. A political crisis was averted with fudge on the Irish border issue. PM May has amended the back-stop plan in the case of no agreement being reached for a “temporary customs arrangement” until a longer term trade deal is in place. This saga has a long way to run yet, with EU officials still said to be dismissive of the UK plan. The debate in the House of Commons schedule for Tuesday and Wednesday next week on the amendments to the original Brexit Bill demanded by the House of Lords is the next potential flashpoint.

G7 noise will be filling the airwaves as G7 the heads of state assemble in Quebec for what is being billed as G6 + 1 summit.

It’s a fairly light data calendar today. Japan has Current Account and revised GDP (latter seen lift to -0.4% from -0.6% after new capex data published last week).

Tonight Germany has trade figures (actually worth a look-see in the context of rising EU/US trade angst), France has industrial production, and Canada published its last Employment figures – of some relevance with money market still attaching a more than 70% probability to the Bank of Canada lifting rates next month.

Finally, note that on Sunday Switzerland holds its referendum on ‘Vollegelt’, a proposal that would in effect strip the Swiss Banking system of its ability to create credit beyond that supplied by the Swiss National Bank. Polls strongly suggest it won’t get up and the SNB is adamantly opposed, but were it to succeed it would cause ructions not just in Swiss market put potentially globally.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.