Online retail sales growth slowed in May following a fairly strong April

Insight

The dollar remains the hot topic, just as the weather has been in SE Australia with a slice of this summer’s heatwave coming through with a vengeance, not to mention Roger Federer’s fifth and winning set to reach 20 Grand Slam wins at the Australian Open.

https://soundcloud.com/user-291029717/the-weak-us-dollar-and-much-ado-about-davos

The dollar remains the hot topic, just as the weather has been in SE Australia with a slice of this summer’s heatwave coming through with a vengeance, not to mention Roger Federer’s fifth and winning set to reach 20 Grand Slam wins at the Australian Open.

After comments from US Treasury Secretary Mnuchin arrival at Davos’s commentary extolling the trade virtues of a weaker dollar, the EUR/USD rose further to as high as 1.2537 on Thursday Davos time. ECB President Draghi failed to push back against EUR strength presenting an upbeat view of economic developments. He did though have a very thinly veiled – and loud – pop at US Treasury Secretary Steve Mnuchin, putting the blame for the latest dollar-related rise in EUR/USD to ‘someone else’s’ communications.

The USD then reversed later Thursday after President Trump’s intervention saying Mnuchin’s remarks were taken out of context and that the dollar was only going to get stronger (as the US economy went from strength to strength).

As my colleague Ray Attrill wrote in his weekend summary yesterday, our take on Trump’s intervention was that they were prompted by realisation that the US administration would otherwise have lost whatever moral authority it still had in demanding market determined exchange rates and railing against ‘beggar thy neighbour’ exchange rate policies. Mnuchin’s original comments (and the context in which they were made, straight upon his arrival in Davos and with the dollar already on the skids) deserve some attention, attention the markets subsequently delivered and re-embraced. FX markets tilted back toward a weaker Dollar view, US dollar indices retracing about half of Thursday night’s pop higher as of Friday’s close.

Q4 US GDP data on Friday showed growth of 2.6% (saar) against 3.0% expected. On the surface this was technically a “miss”, but the quality of the report was high from a growth momentum viewpoint. There were big growth drags from inventories (-0.7% points) and net exports (-1.1% points). Consumption was a strong 3.8% as was business fixed investment +6.8%, with the core PCE deflator 1.9% as expected, but still only 1.5% y/y.

The drop in inventories is explained by a big run down in car inventories as sales soared in the aftermath of the hurricanes, and so dealerships were caught short and not a worry from a demand viewpoint. In fact it was the opposite. The jump in the (previously unreleased) December trade deficit was a bit more sinister, insofar as the deterioration in the trade balance since mid-2016 is at last partly reflective of the lagged impact of the 20114-2016 US dollar rally (the currency matters for the trade balance, a point clearly not lost on Mnuchin last week). That was also given further force by the large 1.1% point net export growth drag in Q4 though we’d note that, Q4 real exports still grew a solid 6.9%. It was the 13.9% Q4 import surge that did the damage, influenced by past dollar strength and upbeat US domestic demand.

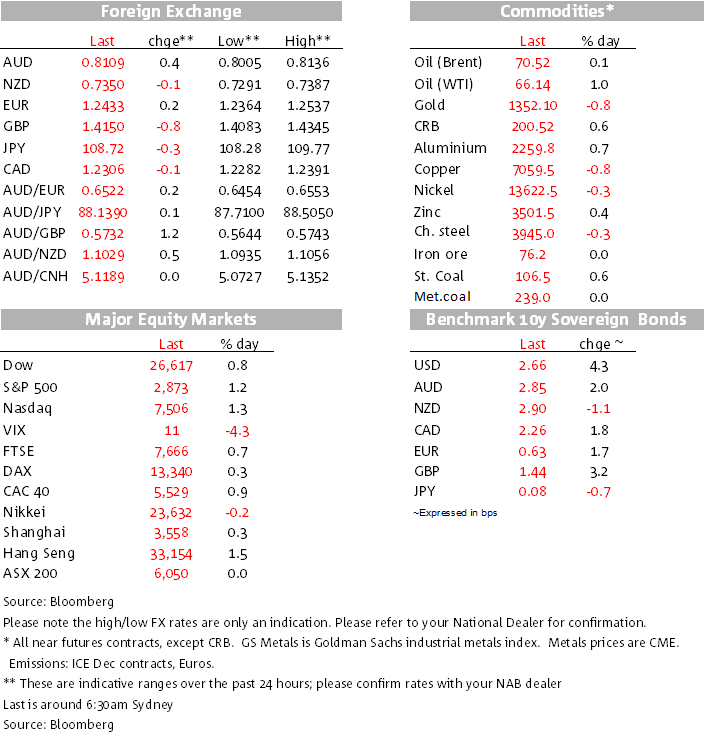

Going along for the ride with the further push lower in the USD, the AUD poked its nose above last September’s 0.8125 high on Friday (to 0.8134) before easing back to 0.8110 at the close. It trades close to that level in early morning. The NZD finished Friday about a cent lower than its pre-CPI levels and also opens close to Friday’s close, currently at around 0.7350. The market will be alert to any downside surprise from Australia’s CPI on Wednesday, though this is not what NAB expects. NAB’s forecast call for marginally higher headline CPI but marginally lower core (0.8% for headline, 0.4/0.5% for core against 0.7% consensus for headline and 0.5% for core/underlying.

The other currency that’s come in for special notice was the JPY. It was given a further boost late last week after BoJ Governor Kuroda said in Davos that inflation was finally moving towards the 2% target. It subsequently retraced some of that appreciation after a BoJ spokesman was compelled to issue a clarification, saying that Governor Kuroda/the BoJ had not revised (up) the inflation outlook at last week’s BoJ meeting and their new Outlook report. Friday’s Japanese CPI report for December was close to expectations, headline at 1.0% y/y, ex-fresh food CPI at 0.9%, and “ex fresh food and energy” at 0.3%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.