Coming in for landing in a heavy cross wind

Insight

It’s been a bumpy day for oil following Trump’s withdrawal from the Iran Deal. But it’s today’s weaker than expected US CPI data that has had the most influence, driving down Treasury yields and giving a boost to share prices.

https://soundcloud.com/user-291029717/iran-makes-oil-bumpy-weaker-cpi-pushes-us-yields-lower

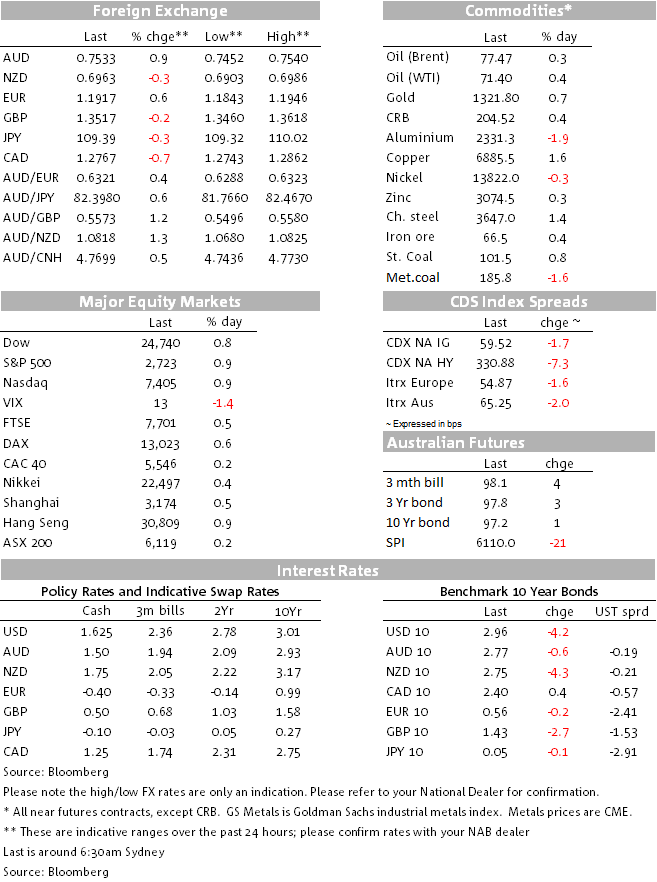

The USD and GBP are the both softer overnight, after US core CPI surprised by 1/10% to the downside and the Bank of England shaved a 1/10% off its inflation forecasts and gave a nod the current market pricing that currently see no more than three 25-point Bank Rate rises over the next 2-3 years. The NZD is still weaker than both currencies over the past 24 hours following yesterday morning’s crunch lower after new Governor Orr said he sees an equal chance of the next move ion rates being down as up. The NZD has recovered about two thirds of its losses against the USD but none versus other currencies, including the AUD. The AUD/NZD cross has finished in NY at its best levels since mid-February.

US stocks and bonds both liked the softer CPI news, the S&P finishing up almost 1% with the VIX at its lowest close since Jan 26th, 10-year Treasuries down 2.5bps to 2.965% and the 30-year 5bps following a strong auction.

The surprises from the Bank of England was not that they left rates unchanged, nor the 7-2 vote (both were fully expected) but rather that the inflation profile was lowered by about 0.1% to be at target in 2-years (lower pass-through from past exchange rate weakness being cited) and that these lower forecasts came on the assumption that Bank Rate moves up only in line with prevailing market pricing over the forecast horizon. GBP/USD promptly fell from above $1.36 to below $1.35 (low of $1.3460, with AUD/GBP from 1.55 to 1.5575). Losses were then pared in the wake of the US CPI report but GBP is still the second weakest currency of the past 24 hours after the NZD.

US CPI met expectations at 0.2% in headline terms, but rose by only 0.1% (0.098% unrounded) against 0.2% expected to leave the year-on-year rate unchanged at 2.1% against 2.2% expected. Lower used car and airline fares were largely responsible for the downside miss, the former seeing an ongoing reversal from last year’s post-hurricane surge. The key takeaway from the report is that there is as yet no smoking gun for the Fed to be lifting its median ‘dot’ forecast for the expected number of Fed rate hikes this year from two more to three. The read-through from CPI to the April core PCE data due at month end is that it should fall from 1.9% to 1.8%, albeit still on track to push above 2% in coming months.

The US dollar, having already recoiled by about 0.5% on Wednesday for no obvious fundamental reason, is down about another 0.25% compared to its pre-CPI levels. This fully accounts for the recapture of the 0.75 handle by AUD/USD (overnight high of 0.7540) though we can also point to the latest decline in the VIX and small extension of this week’s commodity price gains. AUD is the best performing currency of the past 24 hours but AUD/USD still remains substantially below our short term fair value model estimate (currently close to 0.79). This suggests scope for a deeper correction higher in coming days if the USD dollar further loses its footing from its mid-week highs.

Finally, the return of political uncertainty in the Eurozone hasn’t done any real harm to the Euro, even before the US CPI inspired USD sell-off, but has seen Italian government bonds underperform their ‘core’ counterparts. This is after former Italian PM Silvio Berlusconi announced he was dropping his opposition to a coalition between the far-left Five-Star movement and far-right League, after months of failed negotiations to form a government. As our BNZ colleagues note in their daily commentary, the two potential coalition partners have plenty of ideological differences on economic policy (the League want a flat income tax while Five Star want a guaranteed income scheme for the poor) but are seemingly united by their mistrust of Brussels and dislike of austerity. The Five Star movement has in the past called for a referendum on the euro, and while they have backed away from that stance recently (calling it a “last resort”) investors are likely to be unsettled.

The spread between Italian government bonds and those of German bunds widened 5bps overnight, although it remains well off the wides reached when the market was worried about the French election last year. Certainty we don’t see these developments as representing anything like the existential threat to the Euro that the election of Marine Le Pen would have represented. Markets seem to concur so far, with the likes of the EUR/CHF exchange rate actually moving up not down in the last 24 hours.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.