A private sector improvement to support growth

Insight

Italian two year bond yields rose 190 basis points overnight. It’s the worst sell off in 26 years, with the distinct possibility that Italians will go back to vote as soon as July.

https://soundcloud.com/user-291029717/italian-meltdown-as-early-election-looms

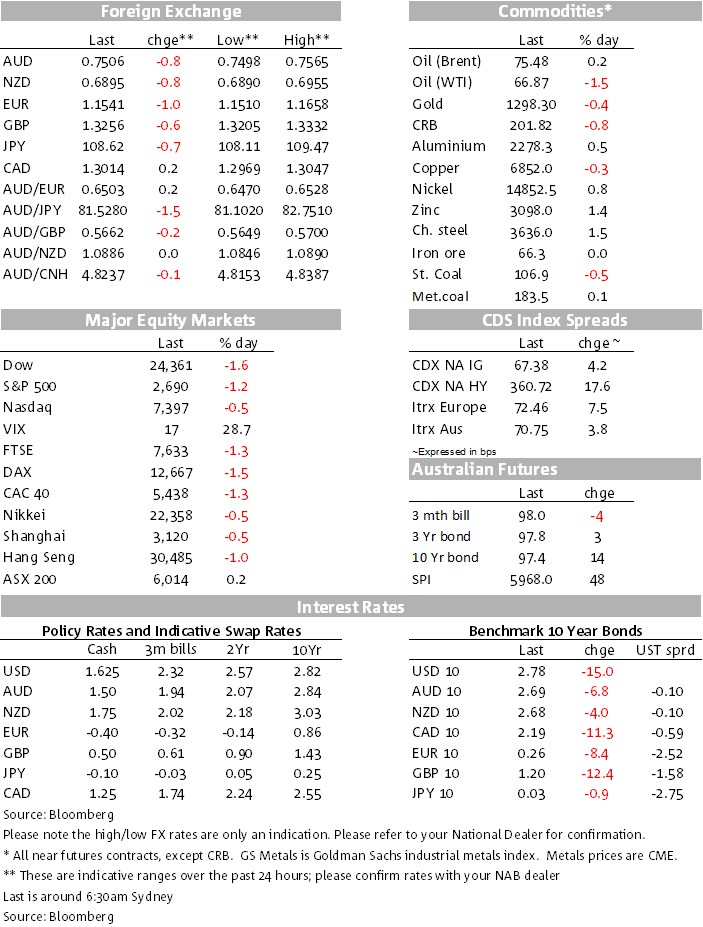

It’s been a night of heavy selling of Italian debt securities, bonds and stocks, spilling over into other prone European markets, nothing short of a meltdown as others have noted, also selling of the Euro and risk assets globally as the US and UK markets return after their respective long weekends. (The exceptions were base metals and gold, the latter finding no new support.) With Italy’s President rejecting the League/Five Star Coalition’s nominee as Finance Minister (a known Eurosceptic), the President’s choice of former IMF official Cotarelli as a technocrat leader is given the cold shoulder by the Coalition. Moreover, Cottarelli reportedly left a meeting overnight with the President without any agreement on a cabinet team. They are apparently meeting again tomorrow. Whatever the outcome there, with no indication that a “technical-led” government could even work now for a time, there’s understandable pressure to hold fresh elections, possibly as early as July. The League/Five Star is already turning the election into an anti-establishment/anti Euro one and that’s what the market has in its sights.

Italian yields soared from the open. Two year bonds spiked higher by a net 186bps in a savage move as investors became agitated about redenomination risk given the rapid pace of change in Italian politics. Italian 10y yields also jumped, still by a huge 48bps daily move, spilling over into global markets, with investors though shying away from Spanish, Portuguese, and Greek bonds. Spanish 10 year bond rose by 9.6bps, Portuguese bonds by 12.2, and Greek bonds by 31.3bps. The 5 year credit default swap on Italian sovereign debt spiked higher from 170 to 290, the highest since 2012/13 in the aftermath of the Euro debt crisis.

Global bond markets rallied sharply, German 10 years by 8.4bps, having rallied by 6.2bps on Monday, the yield down to just 0.26%, having been over 0.6% as recently as a fortnight ago. US 10 years came back from the weekend and have dropped by 14.5bps for the session, the yield down to 2.786%. Markets are still pricing for the high likelihood of the Fed hiking on 13 June, but have understandably scaled back the odds given current market turmoil. No surprises then that stocks were down in Europe and in the US, the Eurostoxx 600 index by 1.37%, Milan by 2.65% and Madrid by 2.49%. The Dow was down 500 points in the afternoon session and has ended own close to 400 points, -1.58%, the S&P by 1.16%, and the Nasdaq by 0.5%.

It’s been relatively measured in the currency space by comparison. The Euro has been sold down another big figure testing support at just over 1.15 earlier in the London session and again in NY, currently trading at 1.1536. With the VIX higher, by 3.8 points, it’s not surprising that the AUD and the NZD are lower, but AUD/EUR has made up some net ground over the past 24 hours. There was support overnight for the yen and the Swiss France, the DXY also making some positive headway.

What can the ECB do? It can take steps to calm European money markets and provide liquidity as needed. It could also potentially wheel out its post Euro debt crisis policy of Outright Monetary Transactions (OMT), a program to support a Euro economy’s secondary bond market if requested to do so, but that program was intended to come with an accompanying fiscal plan. ECB President Draghi might yet have to step up and “do whatever it takes” to support the Euro as he famously said back in 2012. At the end of the day, it’ll be Italy’s politics that will remain under focus. Market pressure is one risk that can be addressed by the ECB; political pressure is another, largely beyond the purview of the ECB.

On the Spanish political scene, Prime Minister Rajoy is facing a no confidence vote on Friday and it seems that the centre of the road Ciudadanos Party might also now be angling toward another election.

Just to throw some more geopolitical spice into the mix, the US Administration has arced up again on US-China trade tensions, now with a plan to be unveiled on June 15 spelling out $50bn in Chinese goods that will then be subject to tariffs. Controls on Chinese investment are also expected on June 30. China issued a follow up statement to the effect that they will protect their interests. Meanwhile preparations for the US-North Korea June 12 Summit continue. The President has also been tweeting overnight on Chinese aggression to obtain technology from American companies to undermine creativity and innovation as well as practices that undermine fair and reciprocal trade.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.