NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

It’s been another night for selling stocks, Europe taking up where the US and Asia left off (the Eurostoxx 600 was down 1.56%) and this set the tone for the US market.

https://soundcloud.com/user-291029717/equities-hit-draghi-speaks-the-rba-and-other-aussie-news

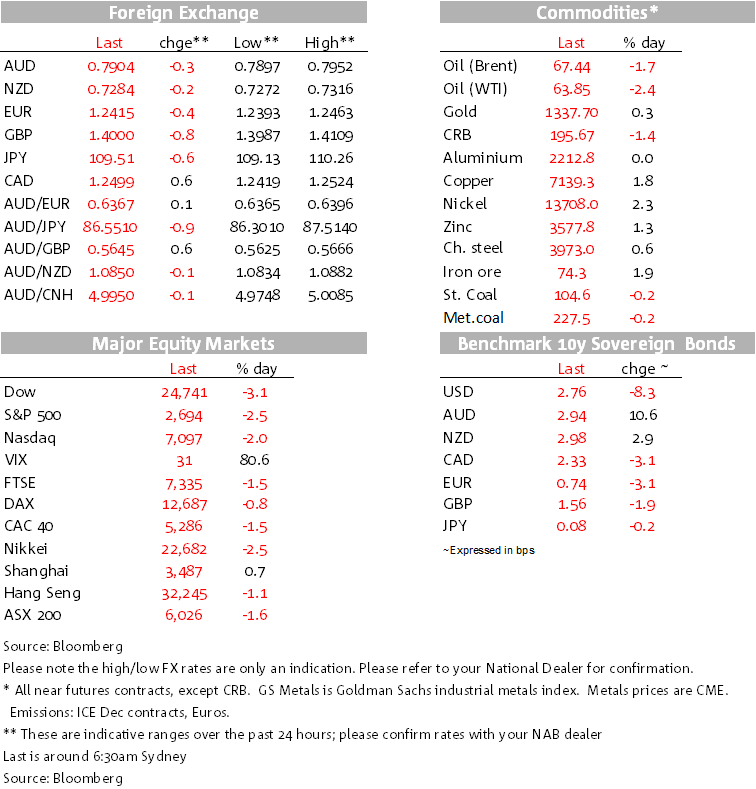

It’s been another night for selling stocks, Europe taking up where the US and Asia left off (the Eurostoxx 600 was down 1.56%) and this set the tone for the US market. The drop in the Dow has accelerated in the last hour to over 1000 (!) at one stage in the past 30 mins near to print, down another eye-glazing 3%, with a 2.3% fall in the S&P 500, the Nasdaq off 1.9%. However, the trigger this time was not further yield nervousness, least not as far as the US Treasury market is concerned, yields down initially 3-4 bps for the session pushing further lower, 10s now down a net 7.5bps. A stellar US ISM Non-Manufacturing report was a side issue on the day. The VIX index is up 13 points to over 30, on three year highs.

It’s been mixed news on the commodity front and not all playing to the defensive market thematic. Base metals were actually higher in London, copper up 1.76% and the volatile nickel price up 2.31%. Gold is up 0.4% to $1342/0z while oil is lower, WTI by 2.41% to $63.87/bbl and Brent down 1.66% to $67.44. Dalian iron ore and steel rebar futures were both higher in China yesterday, spot iron ore futures by 1.15% and rebar +0.68%.

The DXY remains bid, up another 0.30%, making gains against most of the majors, the AUD, EUR, and NZD being pushed proportionately lower as a consequence. Sterling came in for more selling from a combination of more Brexit chatter and a somewhat lower than expected reading on the Services PMI for January that came in at 53.0 after 54.2 against expectations of 54.1. Not a big miss and still in growth-positive territory, but a modest technical one. UK Chief Brexit negotiator Davis has been speaking of constructive talks with the EU, Barnier saying that is the UK leaves the customs union, there will be trade barriers. Speaking to the European Parliament, ECB President Draghi said that they need to prepare for the risk of no transitional agreement.

While most of the major currencies lost some ground against, one that swam against the tide was the Yen which has held its ground. The safe-haven bid perhaps, though the Swiss Franc has been sold lower.

Most of the further rise in the USD came before the release of the US ISM Non-Manufacturing report for January that was a blockbuster. The market consensus was looking for a modest rise from 55.9 to 56.7, but it jumped to 59.9, the highest since 2005. And the important orders, employment, and prices paid details of the report were if anything even better, all printing north of 60. The Employment index jumped from 56.3 to 61.6, the highest level since this report was first complied back in 1997 while new orders was 62.7 and prices paid at 61.9. This is all testimony to a still strengthening labour market into this year, continuing the strong growth thematic that emerged from the January payrolls report but with no immediate market impact.

On the inflation theme, Kashkari has been doing a Bloomberg TV interview this morning, seemingly softening his post-payrolls comments a shade that we reported on yesterday. “On Friday, with the jobs report, we saw a little hint that wages might finally be rising,” he said. Still, it’s “not yet” enough, he added. “It could be a blip, but let’s not ignore it.” There’s more Fed speak over the next few days, including dovish Bullard tonight.

In his remarks to the European Parliament overnight Mario Draghi seems to be laying the groundwork to offer an end of QE timing view when they do their major forecast review next month. He recognised better than expected growth at an above potential rate and more confidence inflation will converge on their goal. But he said they can’t yet “declare victory” and was not prepared to provide an end date for the ECB’s QE program. Not yet anyway.

The market is not priced for any fireworks from the RBA 2.30 statement today, but of course will be paying close attention to their views on the economy and the outlook. We look for their forecasts to be left unchanged. There may well be more market reaction to Retail Trade with the market looking for -0.2% after November’s +1.2%, NAB’s expectation more AUD-defensive at -0.5% of not a little more. A better international trade balance might offer some respite.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.