Online retail sales growth slowed in May following a fairly strong April

Insight

Why such little reaction to Friday’s historic peace promise? NAB’s Ray Attrill suggests why it failed to move the markets, and looks to this week’s major influences.

https://soundcloud.com/user-291029717/markets-not-drawn-on-peace-promise-yet

Former Smiths guitarist and co-songwriter Johnny Marr’s 2014 solo effort Back in the Box is really about euphoria, not about things being returned from whence they came; the latter being a decent enough description of Friday’s market, in FX and bonds at least. The USD firmly rejected a test of the important 92.0 level on the narrow DXY index and US 10 year Treasuries recoiled from the mid-week achievement of a move onto a 3% handle to close at 2.96%. US stocks failed to hold their Intel and Amazon earnings-related opening bounce, the S&P 500 closing up just 0.1%

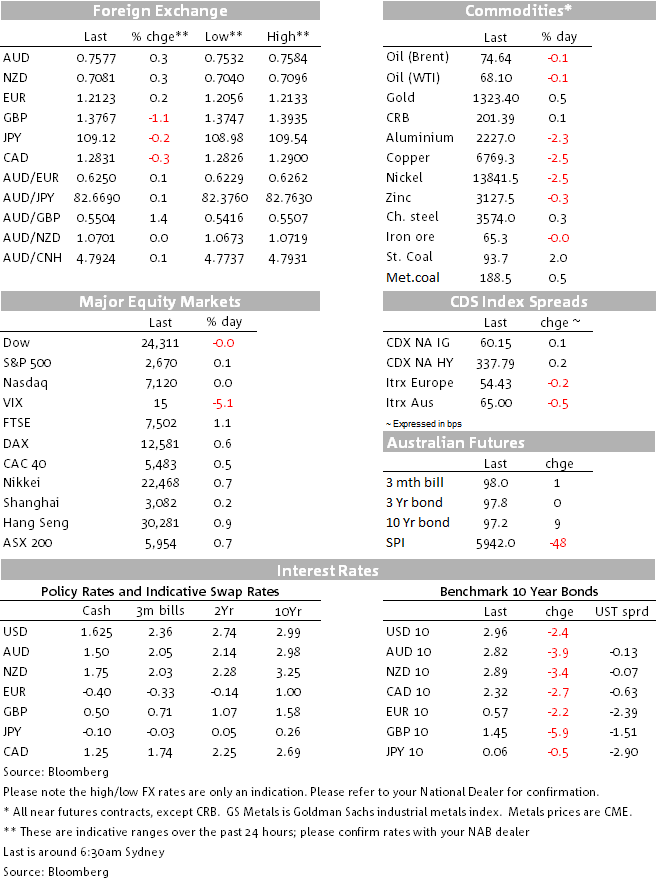

On the week the S&P is flat, so recovering from the mid-week wobble that came in conjunction with 10 year Treasuries topping 3% for the first time since early 2014, thanks to some stellar earnings reports and fall-back in UST yields. More than half of S&P500 firms have now reported, with EPS on average 24.6% up on a year ago, against pre-reporting season expectations of about 20%. The VIX finished the week back on a 15 handle from above 16 both on Thursday and a week ago:

Early New York session US dollar strength and just about the best intra-day levels of the day for Treasury yields came in the immediate wake of US Q1 GDP figures, showing annualised growth of 2.3% against the 2.0% market consensus and the Q1 Employment Cost Index (ECI), the latter printing 0.8% up from 0.6% in Q4 2017 and above the 0.7% expected.

The detail of the GDP data was less impressive however, with private consumption rising by only 1.1% despite the boost to incomes in the quarter from January’s tax cuts, and inventories making a relatively large 0.4% contribution to growth. The 2-year Treasury yields did end marginally higher on Friday – perhaps a nod to the strength of the ECI and what that means in terms of ongoing Fed policy normalization – with the 2s/10s yield curve ending the day – and week – some 2-2.5bps flatter.

In FX, it turned out to be a day of two halves, the USD up across the board though early morning NY trade with highs coming soon after the GDP print, and then giving it all back. Thus DXY was flat on the day but the broader BBDY down 0.2%. 92.0 was always going to be a tough nut to crack on DXY, being the January breakdown level and the 200 day average and Friday’s price action proved it (complete with a gravestone doji on the candlestick charts, or so the charting aficionados tell us. All G20 currencies bar GBP were firmer on the day, so AUD ending Friday over half a percent back from its intra-day low of 0.7532.

The GBP story was all about GDP, the pound dropping by 1% after Q1 UK GDP printed just 0.1% to see odds on a May 10th BoE rate rise slashed to less than 25% from around 60%. The jury will remain out for a while in determining the extent to which this was just a weather-related hit to growth or something a bit more pernicious. Either way, it has almost certainly taken a UK rate rise next week off the table (NAB moved its call from May to August ahead of the data and following the rhetorical back peddling from BoE Governor Mark Carney the week before).

In commodities, the main feature of Friday’s trade was a 2% fall in the LMEX index, with both copper and aluminium off more than 2%, the latter on reports that Russian oligarch Oleg Deripaska is now set to give up control of Rusal by reducing his majority stake in EN+, its London-listed parent company. On the week, LMEX is off almost 5%, oil and coal were mixed and gold down 1% thanks largely to a firmer USD.

CFTC futures market FX positioning data for the week ending Tuesday April 24th shows only modest reductions in net speculative longs in EUR, GBP and NZD, much less than the spot market price action would have had you believe. As we often note though, significant shifts in reported positioning tend to lag big moves in spot, often by several weeks. Either that, or there is a lot more downside potential for these currencies from still-stretched long positioning. The overall USD short (than in notional terms was at a post-2011 high the week before) has been trimmed by about 13%.

In US rates markets, the move higher in 10 year yields to 3% has been accompanied by an extension of already extreme net speculative shorts, to a new record, one reason at least for caution vis-à-vis the likelihood of a further rapid move higher in yields.

Coming up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.