Online retail sales growth slowed in May following a fairly strong April

Insight

The market reaction to today’s US announcement on Chinese import tariffs, the FOMC meeting this morning and a near certain rate rise from the Bank of England.

https://soundcloud.com/user-291029717/up-tariffs-apple-shares-bond-yields-down-the-aussie-dollar

For the past hour, it’s been expected that President Trump would announce at a press conference details on the further $16bn of tariffs and more importantly increase the threatened tariff from 10% to 25% on the additional $200bn in tariffs promised on retaliation. Chinese Foreign Ministry spokesman Geng Shuang said yesterday that “US pressure and blackmail won’t have an effect. If the United States takes further escalatory steps, China will inevitably take countermeasures and we will resolutely protect our legitimate rights”. “Unilateral threats and pressure will only produce the opposite of the desired result”.

But there’s been no press conference, officials backgrounding reporters that the US may lift planned tariffs to 25% on the $200b and hasn’t decided on the other $16bn not specified.

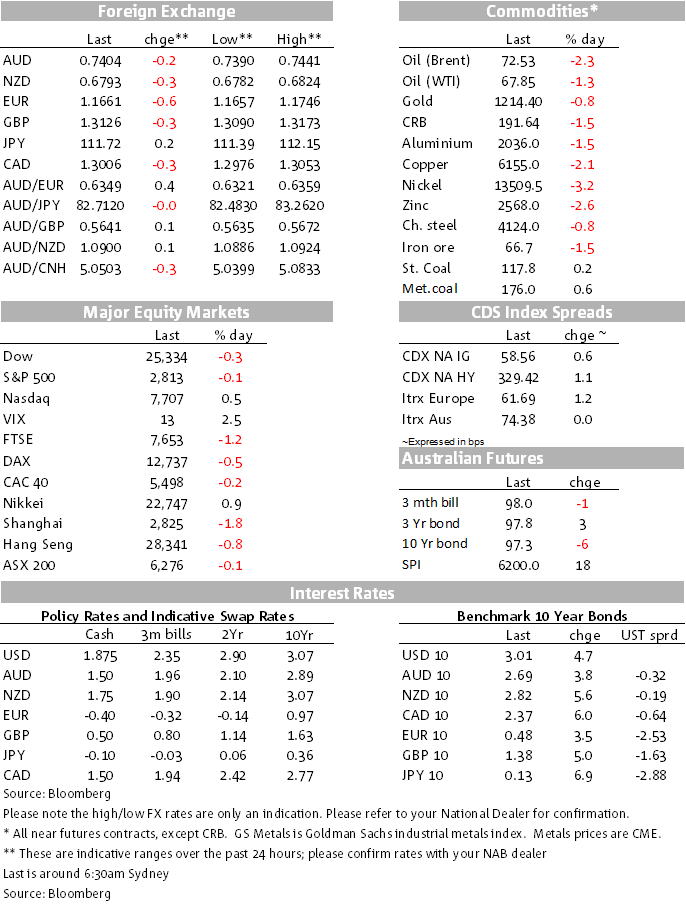

This news took the edge off risk sentiment in the APAC session yesterday, denting the local ASX200 that closed a little lower while the Shanghai stock market closed down 1.8%. This news has dominated market attention, the market putting to one side the announcement out of China yesterday of further measures agreed to by the Politburo to support China’s economic growth. These included: putting economic growth ahead of structural reform, pursuing more tax cuts and seeking to boost infrastructure spending. While reiterating deleveraging as the main job, the meeting stressed that the deleveraging needs to be at gradual pace. They also removed the wording of “neutral” in the monetary policy stance, keeping prudent monetary policy unchanged, adding to maintain reasonable ample of liquidity.

Whether these are more in the nature of fine tuning or more substantial could indeed turn on how events are shaped, but it’s a very clear indication of continued growth intent.

On the commodity front, iron ore and Chinese steel rebar futures were both lower on the Dalian exchange, selling spilling over to the LME with the LMEX composite index off 1.99%, high beta Nickel down 3.14%. Copper fell 2.03%. Gold is down 0.71%. Oil prices are also lower overnight, WTI by 1.32% and Brent by 2.29%; the market factoring in some recently disappointing costs reported by US shale companies, coming after a mix of results from international oil majors.

While risk sentiment has been on the defensive, at least as far as equities and commodities are concerned (and some inkling of that in FX – see below), global bond yields rose. Admittedly, the catalyst was again from JGBs with the market testing the tolerance of the BoJ for higher yields, the 10y up 6.9bps to 0.131%. This spilled over into European and US markets and was very much in train before the Fed announcement a little earlier this morning. The US 10 year rose 4.66bps and now sits a smidgeon over 3% at 3.0064%, that yield sitting at 2.99% before the FOMC announcement and already having tested 3% in the session.

It’s been a measured past 24 hours. Commodity currencies have edged lower, but not outside recent ranges and in an orderly manner. The AUD is trading this morning around 0.74 still, down one fifth of a per cent, Kiwi and the CAD also on balance somewhat lower. The outperformer has been the yen, partly “safe haven” with Japanese bond yields also supportive. The news of an expected ramp up in the tariff rate on the #200bn to 25% took the edge off equities, hit commodities but had a marginal impact on Aussie and even though the CNY has continued to weaken.

The Fed left rates on hold but signalled it was still on track for further gradual increases in its funds rate, describing the stance of monetary policy as accommodative and not including the “for now” rider Powell used in his recent Congressional testimony as a rider to its policy forward guidance. The statement upgraded its description of the economy’s growth from “solid” to “strong”. They described risks to the outlook as roughly balanced.

The US ISM Manufacturing index missed expectations at 58.1 (59.4 expected, down from 60.2). The report cited already stretched resources and supply chains and called out concerns about the further impact from tariffs and reciprocal tariffs on top of already worrying business input cost pressures. The Atlanta Fed upped its estimate of US Q3 GDPNow to 5.0% form 4.7%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.