Online retail sales growth slowed in May following a fairly strong April

Insight

We can expect a relatively quiet 24 hours trading as the world waits for the results of the US mid-term elections.

https://soundcloud.com/user-291029717/rba-mid-terms-and-the-law-of-the-jungle

Because he’s racing and pacing and plotting the course, He’s fighting and biting and riding on his horse

He’s going the distance…he is going for speed, she is all alone (all alone), All alone in her time of need – Cake

I have no idea about horses, but based on 5 minutes of research it seems that the Melbourne Cup race is all about going the distance and I couldn’t get past Cake’s classic. A wet course could be in the offing with my phone suggesting a good chance of rain, so that is another factor we have to put into the mix and based on 153 cups, only 22% of the time the favourite horse won the race. So my best uneducated guess is that is going to be between Magic Circle or Sound Check, both have form and can go the distance. Good luck if you are playing!

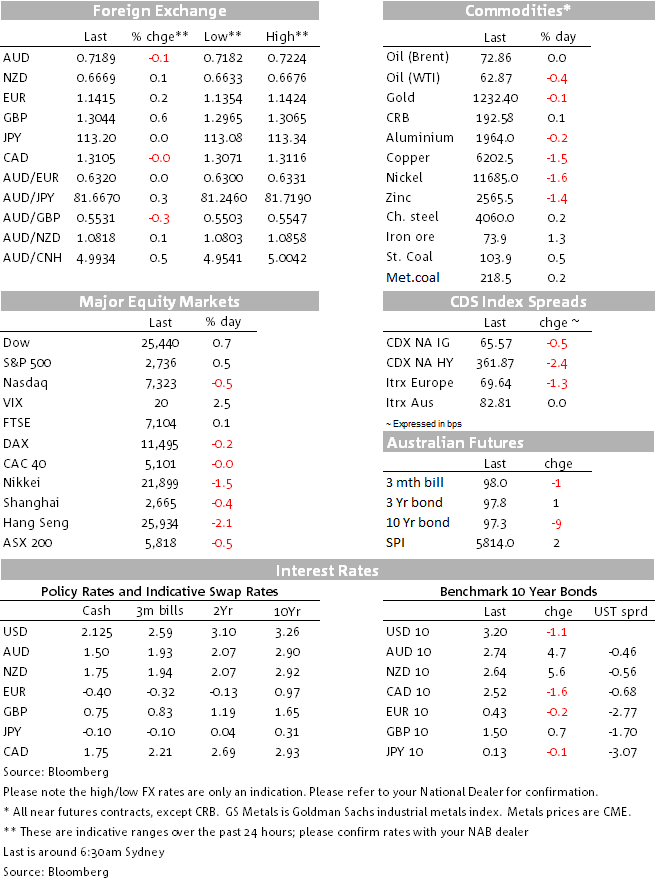

It has been a relatively subdued night in markets with focus in tech shares after Apple extended its Friday decline to over 8%.The USD is weaker across the board with GBP the G10 outperformer while TRY and ZAR have led the gains in major EM FX. The UST curve is flatter with longer dated yields leading the decline and oil prices have edged higher as US restarts sanctions on Iran.

The S&P500 and Dow Jones indices have started the new week on a positive note, up between 0.50% and 0.75%, but the NASDAQ remains under pressure, down 0.46% with Apple shares leading the decline for a second day in a row. A Nikkei report raised concerns over Iphone demand noting that the company was cancelling a production boost for its iPhone XR line, Apple shares were down more than 3% on Monday, taking the two day decline to just over 8%, its biggest two-day slump in more than five years.

Early in the session European shares closed mixed, the Euro Stoxx ended 0.09%, the FTSE100 was +0.14% while the CAC40 closed -0.1% and the DAX was -0.021%.

It has been a quiet start to the week for currencies with the market in a cautious mode ahead of the US mid-term elections and FOMC later in the week. USD indices are softer across the board with the Emerging markets FX index leading the gains, up 0.35% while DXY and BBDXY are down -0.25% and 0.10% respectively.

GBP has been the big mover in G10, following mixed Brexit reports. Yesterday GBP went bid at the open after a the Sunday Times reported that PM May had secured private concessions from Brussels that will allow her to keep the whole of Britain in a customs union, avoiding a hard border in Northern Ireland. However, the positive vibe didn’t last long as the Telegraph dismissed that report and added that UK Brexit Secretary Raab had privately demanded the right to pull Britain out of EU’s Irish backstop after just three months. “If anything, things are now going backwards”, one negotiator said. So after trading to an intraday high of 1.3062, the pound fell to an overnight low of 1.2967 with a softer than expected UK services PMI not helping the cause. The index printed at 52.2 vs expectations for a 53.3, its lowest levels since March. Later in the session we had confirmation that the U.K. Cabinet will discuss Brexit on Tuesday, but Prime Minister Theresa May is unlikely to ask ministers to approve the terms of a deal, but on a more positive note Irish Prime Minister Leo Varadkar said he was willing to consider the latest U.K. proposal. So thanks to the latter news, GBP is the best G10 performer over the past 24 hours, up 0.58% and currently trading at 1.3049. Despite all the noise, the news flow is still more suggestive that a deal with Europe can be reached before the end of the month, then the big test would be whether the deal gets approval from Parliament. GBP is likely to remain a sharp toy for a few more weeks at least.

The Euro also moved a bit overnight, apart from brexit news, the union currency was under pressure early in the session amid ongoing concerns with Italy’s budget proposal. The Euro traded down to a low of 1.1354, but then we had confirmation that the EU commission had decided not to fine Italy (at this stage at least) and instead it has asked for Italy to submit a new budget proposal by 13 November, in line with the rules of the Stability Pact with Brussels announcing its verdict on the new proposal on 21 November. Suggestion that discussions remain amicable appears to have boosted the Euro with the pair on a steady ascendency since midnight and now trading at 1.1415.

After trading a bit lower yesterday, following a softer than expected China’s Caixin services PMI (50.8 vs. 52.8 exp), the AUD range traded for most of the overnight session and then edged a little bit higher early this morning as the USD drifted lower and European currencies drifted higher. AUD now trades at 0.7214 and a move above 0.7250/0.73 is probably still needed to be sure that the downtrend established since late January has finally been broken. NZD now trades at 0.6670 and similar to AUD, the jury is still out on whether the downtrend on the Kiwi is over. Jason Wong, BNZ market strategist notes that we need to see a convincing break above previous resistance of 0.6730 to have more confidence that the downward trend is finally over.

US Treasury yields are slightly weaker across the curve with a flattening bias, unwinding a little of the big move up in rates last week. The 10-year rate is down 1.5bps to 3.199% and the 30y rate is down 2.20 bps to 3.433%. After some concerns over a potential payback following the big jump in September, the October US ISM non-manufacturing index printed at 60.3 against expectations of a 59.1 outcome. After all of that there was little reaction to the number, but the decent print suggests US growth remains solid.

Copper and lead have remained under pressure down 1.91% and 2.76% respectively and oil prices have edged up a little after US sanctions on Iran started overnight, although eight countries were allowed to continue temporarily buying some crude from the country.

BoC Governor Poloz said the central bank’s estimated range for the so-called neutral rate — between 2.5 percent and 3.5 percent — is “sufficiently uncertain” and “in principle movable.” It could rise or fall depending on global developments. “All we know is that as we get closer to it, whatever it is, we’ll begin to see signs that we’re no longer stimulating demand,” Poloz said. “In fact, we know if we cross into the neutral zone we may see signs” that demand is being constrained.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.