Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

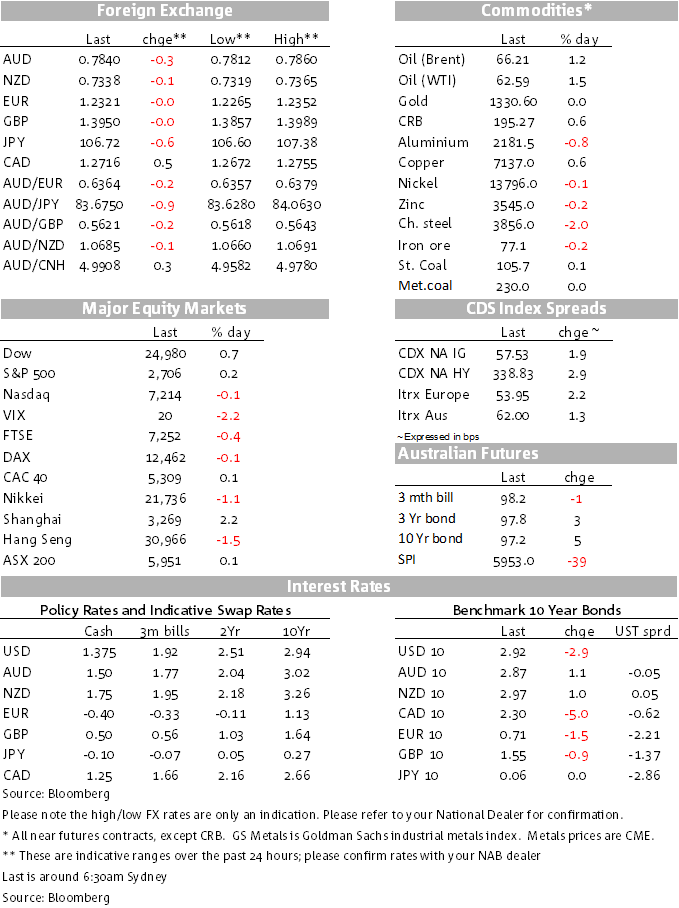

AUD back up to 0.7840/45.

With China back open for business, it’s a confusing equities picture right now. Indices are falling in many parts of the world, just as the US decides to rebound. Phil Dobbie asks NAB’s David de Garis if he can explain what’s happening.

https://soundcloud.com/user-291029717/china-re-opens-britain-slows-stocks-rise-and-fall-minutes-tick-by

As we were discussing on The Morning Call podcast this morning, it’s been a rather temperate/measured week with more of the same overnight. The post-Minutes US growth upgrade enthusiasm saw the USD hold its ground through the Asia session, but Treasury yields began to reverse course through the APAC session yesterday, perhaps setting the scene for a USD pull-back overnight.

It was not a night of top tier US data, but US jobless claims in the February payrolls survey week remained extremely low at 222K against 229K the previous week and below the consensus pick (230K). US equities are back in the black, if off their intra-day highs. There were hints that the ECB will change their forward guidance at upcoming meetings, the next on 8 March. Markets are very much taking in their stride the prospect of an uncertain upcoming election in Italy (March 4) and that Germany is yet to form a coalition.

China came back on line yesterday, the Shanghai and Shenzhen indexes both up handily (Shanghai by 2.17%); Shenzhen +1.89%), Dalian iron ore futures up a net small amount for the day (0.65%), but Chinese rebar futures were off a similar amount. Elsewhere, base metals made further gains overnight, while oil more than reversed yesterday’s falls after a report showing lower US stockpiles against expectations of an increase. Gold was little changed.

Yesterday morning’s release of the January FOMC meeting noted the Fed having increased their growth forecasts since December after signs of positive domestic growth, the upbeat global economy, a rallying stock market, and of course the tax cuts. Since then, US average earnings and core CPI data surprised on the upside, implying more upside risks to the Fed’s expectation of three rate rises this year, a new set of the ‘dots’ coming at the 21 March meeting. US yields moved higher after the minutes, with the 10 year rate hitting 2.95% although these moves reversed overnight, the 10 year rate is back to 2.919%. The short end of the US Treasury curve has been reasonably stable and the market continues to price three hikes for this year.

Data out of Europe was marginally softer than expected, the second estimate of UK economic growth revised down a tenth to 0.4%/1.4% from the initial estimate of 0.5%/1.5% though seemingly from a net export drag, including stronger import volume growth. Sterling had a brief look at somewhat lower levels in the aftermath of the GDP update, but the renewed softness in the USD lifted all boats, including Sterling. It was a not dissimilar story for the Euro dipping a little after the release of a slightly below expectations German Ifo survey for February, though it remains at strong levels. The Business Climate Index came in at 115.4, down from 117.6. In perspective, it was 111.2 a year earlier and it’s well north of its long run average of 102.4.

The market was also tuned in to the release of the ECB Minutes of its January 24-25 meeting. The main takeaway seems to have been that the groundwork is being laid – ever so at a glacial pace -for a tweaking of the guidance on the timing of ending QE (the economy is doing that too), a further iteration likely at the upcoming 8 March meeting. There’s still no absolute clarity about whether to signal an end to QE in September when the current buying is scheduled to have run its course. Some at the January meeting were ready to remove a pledge to expand the bond-buying program if needed, but even that didn’t win the day. In the FX space, there was an acknowledgement it’s been a combination of EUR strength and ‘broad weakness of the USD’ but also EUR strength ‘to a lesser extent in nominal effective (TWI) terms’. The minutes noted ‘although the past appreciation of the euro had so far had no significant negative impact on euro area external demand, volatility in FX markets represented a further risk that required monitoring.’ Some sensitivity to the currency remains given lower than targeted inflation.

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.