NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Speaking from Davos early in the London session, US Treasury Secretary Steven Mnuchin set the tone for the session saying “obviously a weaker USD is good for us as it relates to trade and opportunities.”

https://soundcloud.com/user-291029717/pound-rockets-as-us-dollar-dwindles-ecb-meet-and-more-tariffs-threatened

Speaking from Davos early in the London session, US Treasury Secretary Steven Mnuchin set the tone for the session saying “obviously a weaker USD is good for us as it relates to trade and opportunities.” While he endeavoured to put some context around this comments, noting that longer term the strength of the USD is a reflection of the strength of the US economy, Mnuchin’s (repeated) lower USD remark “presses on an open door”, as my colleague Gavin Friend noted overnight. (Check Gavin’s comments on this morning’s Podcast where he also previews tonight’s ECB.)

It’s not only this week’s White House tariffs issue that’s been a headwind for the greenback (more to come tomorrow night from Trump at Davos?), there’s a whole range of factors stacking up against the USD, including the upward momentum in oil and commodities and perception of what other (non-US) central banks will do with policy this year.

Released overnight, European January PMIs remained overall at very elevated levels indicating strong growth. While the Manufacturing components slightly missed (but still above 60), the Services and the Composite indexes accelerated further. The data overall added on net to the theme of continued Eurozone growth acceleration, and did nothing to halt the Euro then benefiting from USD weakness. Adding support to the Euro was a letter from Draghi to European MPs reported by Reuters noting that QE has not led to statistically significant movements in the FX rate, FX moves “are a mere side effect, not the objective.” Note though that It’s not clear when that was written. It’s very unlikely to have been recently with no reference or green light to the Euro’s current rise. Look for some clarification tonight at his press conference.

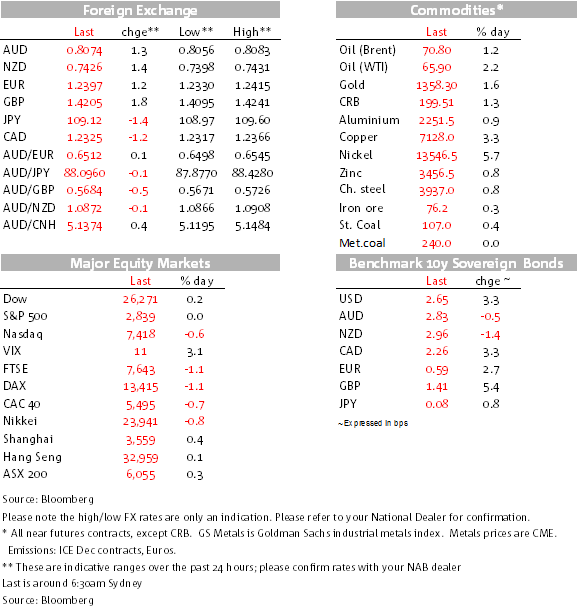

Among the majors, GBP showed the way overnight, GBP/USD above 1.42 this morning, given a leg up by much stronger than expected employment for November in the monthly labour market report, arriving with Sterling-supportive soothing Brexit background music. UK Brexit Secretary David Davis said Britain will stay closely aligned to the EU regulatory regime while Merkel said Germany is open minded when it comes to the shape of a future partnership with Britain. Italian PM Gentiloni also chipped in, saying that any deal between the UK and EU should include financial services. The likelihood of the UK securing a transition agreement that provides around three years of unchanged trading arrangements has been a continuing driver of GBP gains. While the EUR is bid, but EUR/GBP has fallen back to mid-2017 at 0.8700/20.

With the USD lower, oil and commodities rose but more so than just currency valuation effects. WTI rose above $65 for the first time since December 2014 and base metals rose in size. For oil, the weekly US EIA oil report showed the 10th weekly decline in inventories, the longest such stretch. WTI is up 1¾% against around another 1% decline in the USD. The LME base metals index rose 2.45%, copper up a cool 3.28% and nickel 5.64%, both near to if not at current cycle highs. Gold rose another $22.80/oz to $1364.30, +1.69%. The AUD trades is looking to test 0.8080 this morning, up 1.3% over the past 24 hours, broadly in line with gains seen for the Euro, Yen, CAD, and Kiwi.

The DXY (majors) index has eased to fresh three-year lows at 89.2. Each step lower helps build confidence that the 91.01 (Jan 12 breakdown through Sep lows) will form a decent line of resistance for the next event. From that perspective, tonight’s ECB is well and truly on the radar and may contain mixed messages for the Euro. Look for Draghi to again talk up the economic recovery, but we’ll be alert to any anti-EUR messaging at the same time warning on too rapid exchange rate adjustments and the need to maintain a very accommodative monetary policy to secure their inflation objective.

This morning sees NZ’s Q4 CPI, where we (and the consensus) look for +0.4% q/q, leaving annual inflation at 1.9% y/y. We will also be alert to NZ tradable inflation that often correlates to the AU counterpart, AU’s CPI out next Wednesday. NZ tradable inflation is expected to remain steady at 1.0%. For Kiwi and AUUD/NZD watchers, also be alert to the range of “official” core inflation measures for Q4, especially the sectoral factor model version produced and favoured by the RBNZ, which, at 1.4% y/y in Q3, lagged the others.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.