Online retail sales growth slowed in May following a fairly strong April

Insight

Will the US dollar rally continue this week?

https://soundcloud.com/user-291029717/the-week-ahead-for-the-dollar-china-iran-argentina-and-brexit

Like Katie Perry would sing, Friday night was a bit of “hot n cold” market session, we had a mixed US labour market report, but the decline in the unemployment rate to 3.9% eventually lifted the USD and shorter dated UST yields. US-China trade talks ended with no progress and although the lack of resolution keeps the prospects of trade tariffs alive, both parties agreed to keep talking. Meanwhile Argentina’s decision to lift its official borrowing rate to 40% brought the focus back to EM markets amid a rising USD and higher UST yields environment.

Although the disappointments from US average hourly earnings (0.1%mom vs 0.2% exp.) and payrolls (164k vs 194 exp.) initially drove the USD and UST yields lower, the market eventually reversed this initial reaction, focusing instead on the fact that the unemployment rate declined to a new cycle low of 3.9% (4% exp.). Tapas Strickland, one of our northern hemisphere market strategists noted that the data disappointment looks to be weather related with around 52k more people unable to work due to inclement weather compared to this time last year while weather effects were likely responsible for the sharp falls in wages for Utilities (-1.0% m/m) and Information (-0.6% m/m).

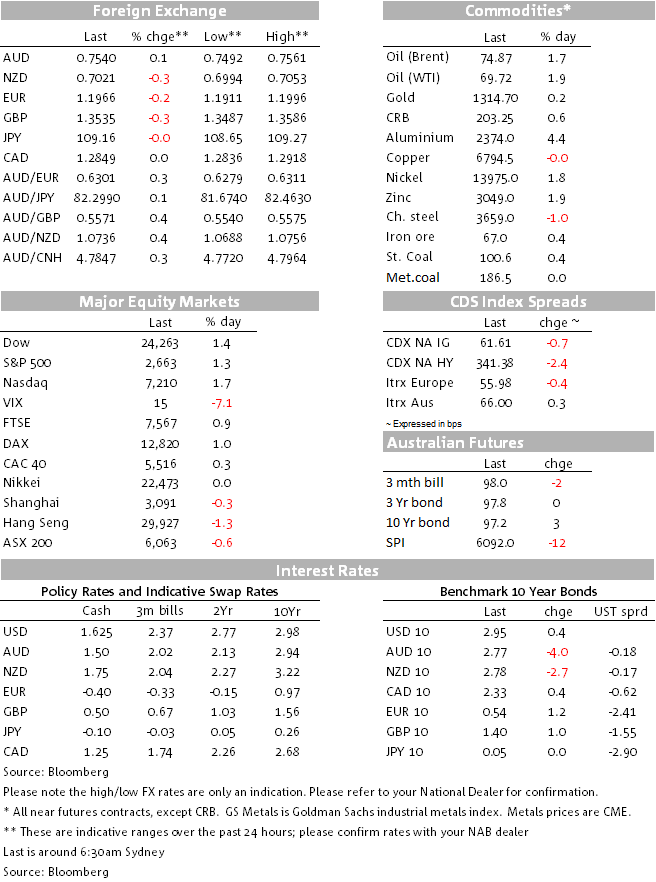

In the end the USD closed Friday higher in index terms (DXY +0.16% @92.56 and BBDX +0.21% @ 1156.4) and stronger against most G10 currencies. AUD (0.09% @ 0.7539) and JPY (0.06% @¥109.12) resisted the upsurge in the USD while GBP (-0.32%, 1.3531), NZD (0.31% 0.702) and the euro (-0.23%, 1.196) were amongst the biggest losers.

Overall our sense is that Friday’s US labour data is unlikely to change the Fed’s thinking that more rate hikes are needed this year. The US labour market is very tight, forward indicators suggest more tightening should be expected and this tightening should also see an eventual acceleration in wages growth. In our view the risk remains that the Fed will need to do more than the 2 rate hikes currently priced by the market in 2018. Incidentally, several Fed officials were out speaking on Friday with the key message being that the Fed’s inflation target was “symmetric” and that they didn’t intend to overreact to a modest inflation overshoot. Fed Chair Powell speaks on Tuesday in Switzerland and hopefully we will get a better understanding on the magnitude and timing of the Fed tolerance to inflation.

Looking at currencies in more detail, the USD was the big winner during the week up more 1%. In relative terms the AUD has actually coped rather well, declining just 0.55% over the week and closing Friday at 0.7536. In contrast, the kiwi struggled a little, down 0.92%, ending the week just above the 70c mark. Meanwhile GBP and SEK have led the declines in G10. Notably too GBP, at 1.3532, closed the week below its 200DMA . This week the BoE is expected to stand pat, but according to a Bloomberg survey, the Bank’s forecasts for both growth and inflation are expected to be revised lower and with political uncertainty still simmering in the background, cable looks vulnerable to the downside. EUR traded to an intraday low of 1.1911 on Friday and at 1.1961, the pair almost closed at a new 2018 low. Lack of EU data releases this week suggest the union currency is unlikely to get any direction from domestic inputs meanwhile the US- EU rates differential remains a downward force.

This week Argentina led the declines in EM currencies given an increase in capital outflows, a stronger USD and higher UST yields. Argentina’s Central Bank’s decision to lift rates by 6.75% to 40% on Friday, helped the Argentine Peso on the day (+2.34), but the pair still closed as the biggest EM loser on the week, down 6.06%. We think pressures on EM markets deserve monitoring as an escalation in EM pressures has the potential to hurt the broader market sentiment and would also weigh on the AUD and NZD

After trading in a 2.90%-2.99% range, 10y UST yields ended the week at 2.95% essentially unchanged over the past 5 days .The 2y10y UST curve flattened 1bps to 45bps as the 2y tenor edged 1.4bps higher to 2.496%. In contrast, other core bond yields such as the 10y Bunds (-2.7bps, 0.544%) and 10y UK Gilts (-4.5bps, 1.40%) declined during the week and our 10y AU futures rate fell 5.5bps to 2.79%.

US equity gains on Friday (up between 1.3% and 1.8%) helped the NASDAQ end the week higher, but gains were not enough to move the S&P and the Dow back into positive territory for the week. Of note however, gains on Friday helped the S&P 500 move back above its 200DMA.

Ahead of the Trump administration decision on whether or not to re-impose oil sanctions on Iran next week, oil prices closed higher on Friday posting gains between 1.7%/1.9%. WIT closed at $69.72 and Brent was $74.87. Coal prices led the gains on the week, Iron ore climbed $1.5 to close just under the $70 mark while gold and copper were little changed over the past 5 days.

Last week’s US-Sino trade talks ended with no progress, but news that the US has pushed for a $200bn reduction in its trade deficit with China (double the amount originally requested in March) essentially means that the US has hardened its line of negotiation and thus the prospects for trade tariffs remains a distinct possibility. Neither party offer any comments, but there has been an agreement for talks to continue. Given upcoming mid-term elections (November) and dwindling Republican support, President Trump doesn’t have the luxury of time, therefore the risk is that the lack of progress may force him to toughen his line further ahead of the elections. The President reaction to last week’s talks will be important for sentiment at the start of this week

Market prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.