A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

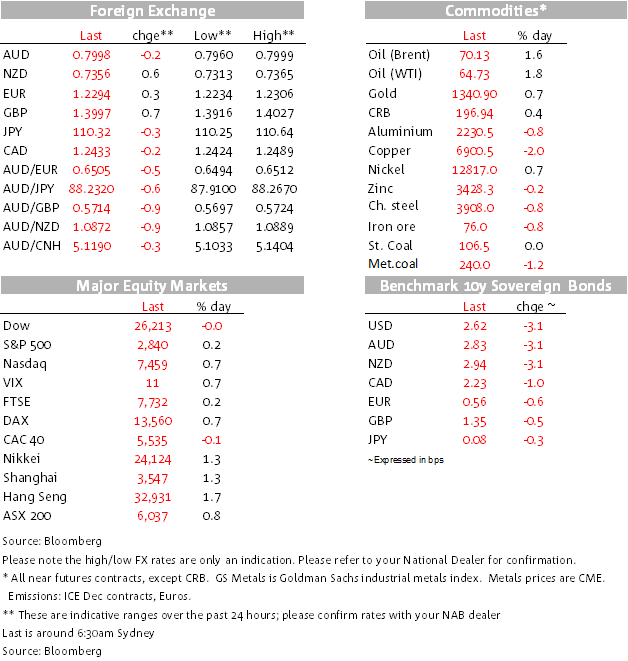

Big dollar subsides again overnight after attempted rally yesterday.

https://soundcloud.com/user-291029717/tax-cuts-and-protectionism-how-trump-is-making-america-great-again

Overview:

Davos kicked off formally overnight, (now in its 47th year), with President Trump to speak Friday at a reception for CEOs, an event that seems to be drawing as much interest as any from the press. Trump is the first President at Davos since Clinton in 2000.

It’s been another quiet night as far for first tier data. There’s been the German/Euro ZEW Investor Surveys for January, the January monthly UK CBI Trends survey and quarterly CBI Business Optimism, and Eurozone Consumer Confidence survey. Notwithstanding their second tier status, these readings have generally been very good still suggesting that the last year’s momentum seen in the Euro-zone economy from a confidence and investor viewpoint has very much carried over into the New Year.

European consumer confidence printed at its strongest level since 2000 and even the UK CBI Industrial trends survey revealed order levels at near record levels in Jan, only marginally below last month that was a record high. Even the UK public borrowing report for Dec was better than expected on record VAT receipts and a credit from the EU, ostensibly on better EU budget finances from an improving economy. There was only the Richmond Fed manufacturing report out of the US that was only slightly weaker than expected, following other US regional partials a little lower ahead suggesting a lower tilt risk for the national Manufacturing ISM Feb 1.

From an FX standpoint, yesterday in the latter part of the Asian session and into London trading, some support for the USD emerged, but it’s proved to be rather short-lived. The announced US tariffs from the White House on solar panels and washing machines has so far come and gone without material market impact, though the market will be paying attention to what President Trump says later in the week at Davos. In the event, the USD has not been able to sustain yesterday’s attempt to move higher, emerging market currencies and its “major” counterparts re-taking some lost ground.

US stocks are little changed into the close (the Nasdaq doing better, helped by Netflix), US bond yields down 2bps across the curve.

The AUD/USD was one cross that was seeing some selling back below 0.80 yesterday, coming when there was some intra-day pressure on Chinese iron ore futures, providing a reason to sell the Aussie, coming on the heels of the US tariff news. Though still closing down for the day, iron ore futures closed somewhat above their intra-day lows, the AUD also garnering some respite from renewed USD selling. The AUD/USD trades around the 80 figure as we go to press this morning. LME base metals were mostly lower overnight, while oil and gold prices rose.

The US Senate Banking Committee had its confirmation hearing for Fed Governor nominee Marvin Goodfriend. He’s currently Professor of Economics at Carnegie Mellon, thought to market-oriented and sceptical about the use of unconventional monetary policy such as QE. He was the head of research at the Richmond Fed for 12 years from 1993, having earlier worked as an economist at the White House in 1984-85 (during the Reagan years). Broadly seen as a safe candidate with a hawkish tilt.

His hearing and views were uncontroversial. He said that inflation is rising slowly, the Fed is on the right path and he has every reason to believe inflation could be at 2% in a year or so. He said that low growth was more corrosive than low inflation, hinting at not being too hawkish. He did say that his job would entail worrying about financial stability. There was no sign of the idea the Fed needs to study its inflation mandate or consider other measures such as price level targeting.

Market Rates

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.