Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Can we expect any market reaction to the Singapore Summit? Also, the response to the spat between Trump and Trudeau, the disappointing manufacturing data from the UK and the start of a busy week for central banks and Brexit talks.

https://soundcloud.com/user-291029717/trumps-one-on-un-just-hours-away

I had thought Haircut 100’s ‘Love Plus One’ would be due for an airing this morning after the acrimonious end to the G7 Summit and where the Canadian Dollar is about 0.5% down on where it ended New York trade on Friday. Nothing much else is bearing scars from what at one level is charitably described as a spat and on another an absolute train wreck.

Instead, its onwards and upwards for markets, with Kim Jon Un and Donald Trump both now holed up in Singapore ahead of their historic meeting scheduled to begin at 9am Singapore time (11am AEST). They’ll both be leaving just a few hours later, but the omens are good for a ‘successful’ summit, with positive headlines from US Secretary of State Mike Pompeo saying negotiations with North Korea are ‘moving quite rapidly’ and ‘talks to come to a conclusion quicker than thought’. The FT is trumpeting ‘Hope high for Trump-Kim détente’. So maybe John Paul Young is right and love really is in the air, just not between North America’s leaders either side of the 49th parallel.

That risk sentiment has shrugged off a small knee-jerk move lower as Monday’s market re-open is evidenced by US stocks ending in modestly positive territory (S&P500 +0.1%), US Treasury yields fractionally higher (10s +0.5bp) and the Japanese Yen down the same amount as the Canadian dollar. The Swiss franc is hardly moved even though the Swiss referendum on Sunday soundly defeated the ‘Vollgeld’ initiative that would have had profound implications for the way the Swiss financial sector would be allowed to operate.

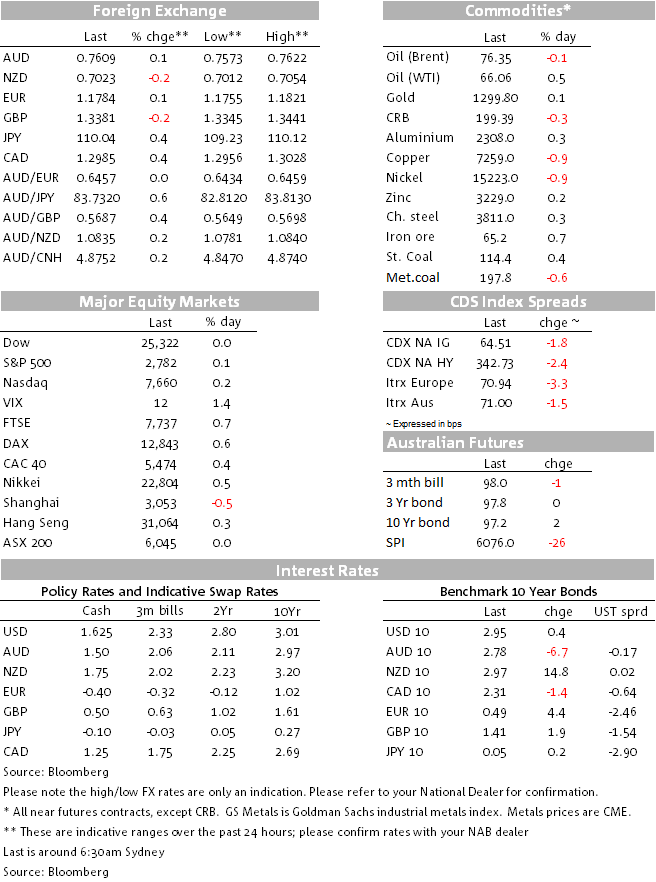

The big moves in bonds since Friday night are not actually in US treasuries but rather German Bunds and Italian BTPs, the former up almost 5bps at 10 years and the latter down a whopping 29bps. This is on the strength of the interview published over the weekend with new Italian Finance minister Giovanni Tria. Highlights include that:

Angela Merkel couldn’t have scripted it better herself.

Euro outperformance against most other G10 currencies is attributable to this, with the Euro-centric DXY actually a touch stronger due to weakness in the other components, notably JPY and GBP

Sterling is suffering in front of the tonight’s first day of a two-day debate on the Lords amendments to the Government’s Brexit Bill. More on this later this today, but this is not the reason the pound is down. Rather it was some rather alarmingly weak UK industrial production data and a blow out in the trade deficit. Manufacturing production in April fell by 1.4% on the month against an expected rise of 0.3% (overall industrial production down 0.8%) while the April visible trade deficit printed at £14bn against £11.3bn expected, the blow out reflecting bigger deficits with both the EU and non-EU trading partners. The NIESR research group currently pegs Q2 GDP at just 0.2%.

The Aussie dollar currently sits at 0.7609, so less than 10 pips away from where it ended in New York last Friday, having recovered from an intra-day low near 0.7560 earlier in the London morning in what looked like it was building into a significant ‘risk-off’ end to the week. A smart recovery in the Brazilian Real (more than 5%) came to the AUD’s assistance in New York, having been the proximate cause of Thursday’s sell-off, after the central bank flooded the market with FX swaps (its de facto method of intervening).

Emerging market currencies in general are on a weaker footing however (losses for RUB, TRY, MXN and ARS on Monday) and remain a weight on AUD. Commodity prices are mixed (see table below) including a near 1% fall for ‘Dr. Copper’. Oil is also mixed (Brent down but WTI up) with Iran still displaying strong public resistance to output cuts when OPEC formally meet later this month. .

Kim Jon Un and Donald Trump are scheduled to meet at 9:00am Singapore time, 11:00 AEST, the leaders of two countries who have officially been at war for 68 years.

NAB business survey at 11:30AEST. Business conditions were last at 21 (equal highest on record) and confidence at 10 (versus long run average of 6).

The FOMC commences its two day meeting, where the outcome will be known at 4:00am AEST on Thursday. As well as the expected 25bp rise in the Fed Funds rate target (and 20bp lift to the IOER) rate) interest centres on whether the median dots shift up and also how the Fed chose to characterise policy (in particular reference to how ‘accommodative’ it still is).

This evening the UK House of Commons begins two days of debate on the various Lords amendments to the government Brexit bill, with particular focus on the extent to which parliament will have scrutiny over whatever deal is agreed between the Government and EU, and whether the government is obliged to negotiate terms for remaining within the Customs Union.

On the data front, we’ll get the German ZEW survey and UK labour market figures, ahead of US CPI. On the latter, NAB sees upside risk to headline vs. consensus (0.3% against 0.2% expected) and a (slight) upside risk on core where 0.2% is expected and would lift the year on year rate to 2.2% from 2.1% (so if a surprise, we’re more inclined to see 2.3% than 2.1%).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.