Total spending grew 0.9% in June.

Friday was another choppy day for equity markets, although the S&P500 managed to end on a positive note.

The markets are prepared for another day of volatility, but there were signs on Friday that things might be returning to normal. The question is, what does normal look like now? Phil Dobbie talks to NAB’s Ray Attrill about the lasting impact of the last week on equity prices and bond yields, and how the Australia dollar will fare.

https://soundcloud.com/user-291029717/will-new-inflation-figures-give-the-markets-another-bashing

US Treasury yields nudged higher, while the NZD and AUD pushed higher.

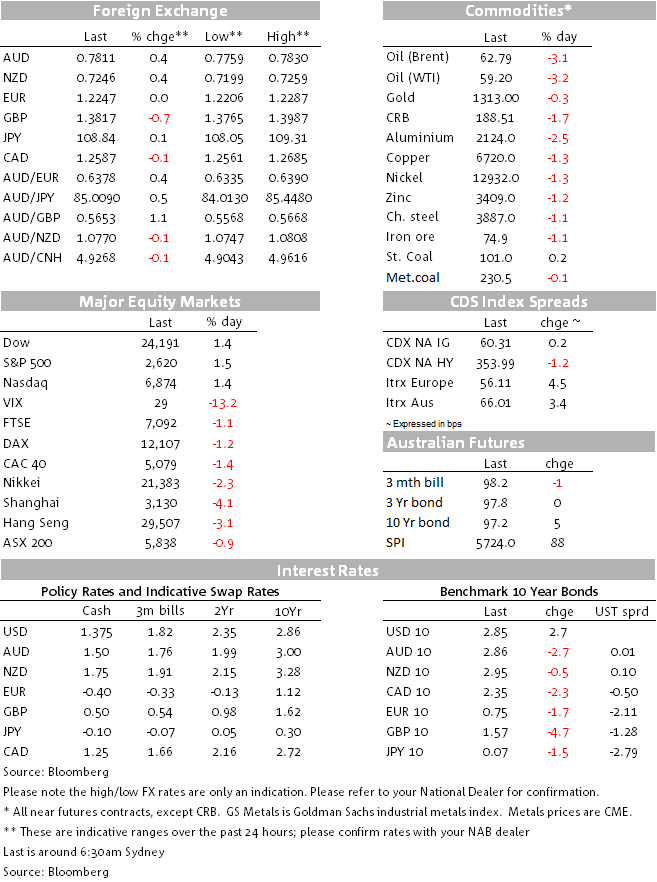

Equity market volatility continued on Friday, with US stocks trading within a 4% range and ending on the positive side of the ledger (+1.5% for the S&P500) while the VIX index traded a 28-41 range and closed the week at 29. There wasn’t much on the economic calendar, with the market wobbles reflecting a continuation of fear, or not, that the big bull run for equities has ended.

President Trump signed a two-year Budget agreement that boosts federal spending by $300b, temporarily finances the government through to 23 March, and suspends the debt ceiling for a year. Economists said that it added about 0.4 percentage points to growth this year, at a time when the labour market is already tight, thereby adding to inflationary pressure and the case for the Fed to consider four rather than three rate hikes this year.

However, that wasn’t how the market traded, with the probability of three rate hikes for the coming year reduced further and the 2-year Treasury rate down 3bps to 2.07% – the short end of the curve being sensitive to the turbulence being seen in the equity market and some pondering about how the Fed might react to the increased market volatility. There was a notable steepening of the curve, with the 10-year rate ending the day at 2.85%, up 3bps, with one eye on the increased fiscal deficit and extra government borrowing that will ensue. Still, there was evidence that equity market volatility was a factor in the session, as the 10-year rate traded a wide 2.78-2.86% range, with yields highly correlated to the intra-day S&P500 moves.

In the currency market, the USD held on to its gains seen earlier in the week and was relatively flat for the session. Currency market volatility remained modest, considering the turbulence seen in equity markets. GBP was the worst performer as Brexit headlines were in focus and weaker than expected UK industrial production and trade data didn’t help. The EU’s chief negotiator Barnier warned that a Brexit transition deal was “not a given” if disagreements with the UK persisted. He also pointed out that come Brexit day the UK will leave behind some 750 international agreements the EU has struck on behalf of its member states on the date of the withdrawal. Our view remains that the UK government will deliver on a transition deal out of self-preservation, for if a transition deal is not agreed to, the government would likely fall. GBP fell by 0.6% to 1.3825.

The AUD and NZD ended the week on a positive note, being the strongest of the majors for the session, highlighting that this isn’t an ordinary bout of risk appetite reduction we’re seeing. The market sees the current risk-off episode as largely an issue confined to the equity market, perhaps a reflection that share prices were just simply over-cooked, and has little to do with changed expectations about the global growth outlook. The RBA said in its Statement on Monetary Policy that the economy was way-off full employment and inflation returning to the mid-point of the target, signalling policy will stay on hold. This was a familiar refrain and there was little reaction for the AUD. The AUD closed the session up 0.4% to around 0.7810.

Canada saw a record drop in part-time employment that coincided with a 20% increase in the Ontario minimum wage. The soft employment, higher wages combo only saw some passing volatility in CAD, while another 3% sliced off oil prices didn’t help sentiment.

The economic calendar is light over the next 24 hours, but that won’t necessarily prevent any further market volatility, something we’ll be keeping a close eye on. In the coming week the key focus will be US CPI data on Wednesday night NZ time. Another positive surprise of 0.3% m/m for the month for the core measure could send bond yields higher and equity markets (and the AUD) lower.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.