Coming in for landing in a heavy cross wind

Insight

The biggest moves have been in US equities, hit by a court ruling on state taxes, and the pound, after a moderately hawkish Bank of England meeting.

https://soundcloud.com/user-291029717/long-night-little-said-us-stocks-down-pound-up

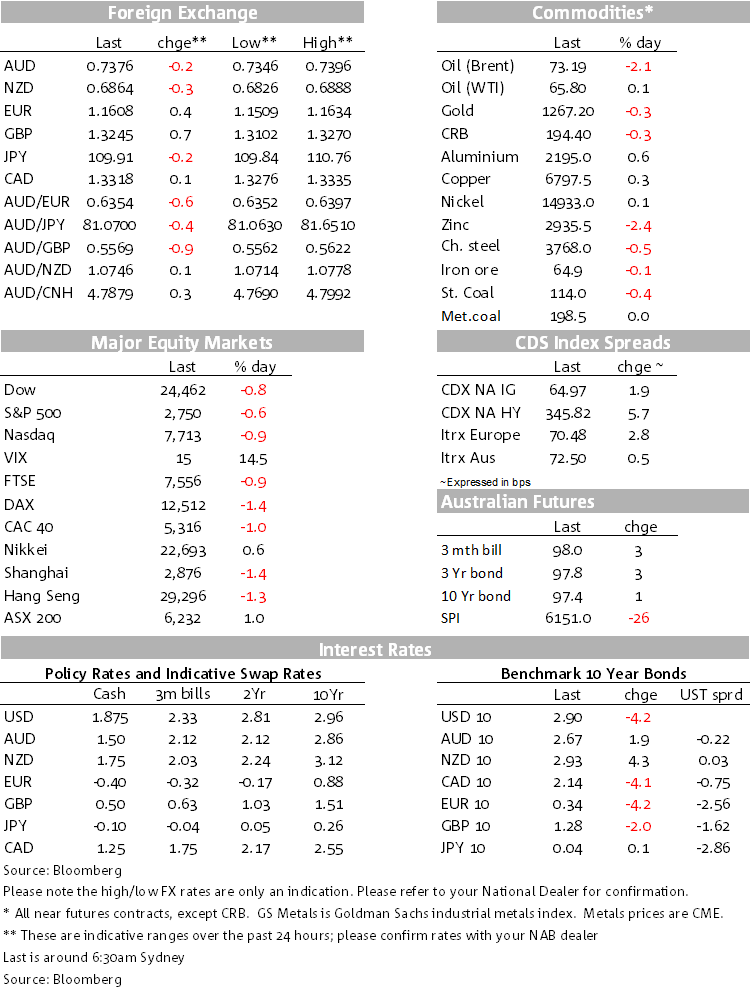

It’s been a night of several parts, the USD DXY index this morning back below 95, equities lower overnight, bonds stronger (except in Italy, Spain and Portugal), and commodities mixed to softer, oil down ahead of a likely OPEC deal tonight to cut output. Iran’s Oil Minister Zanganeh has reportedly come around to the view that some rise in combines OPEC-Russian output, a deal around 600-900Kbpd now on the cards. (Recall that the deal to cut output in late 2016 was 1.8mbpd.) While Brent crude declined $1.65/bbl to $73.08, WTI is marginally higher on the back of the latest EIA report showing a 5.9mb cut in US crude inventories.

The decline in oil prices seemed to weigh on US energy stocks, equity sentiment also dented by the profit warning from Daimler on the impact of tariffs on its Alabama produced SUV imports into China, its shares down 4.32%, the second largest decline on the DAX. (India retaliated to US tariffs on steel and aluminium with reciprocal tariffs on US goods.)

Standing out on the FX front is Sterling aided by three dissenters to the no change expected from the Bank of England against expectations of two dissenters. The other dissenter was no one less than the BoE’s own Chief Economist Andy Haldane. That, the comment in the BoE statement that the softness in Q1 activity was likely temporary, together with an earlier prospective start to winding back QE (after the BoE rate reaches 1.5% (some time away given the current rate is 0.50%) against an earlier signal of 2.00%) all added support to the Pound. Sterling interest rate markets moved to lift the probability of a hike at the August BoE meeting from 45% to 65%. As we go to press, BoE Carney is delivering his Mansion House though his comments so far seem less Pound sensitive. USD/GBP sits at 1.3242, a rise of 0.83%, while AUD/GBP is trading at 0.557 this morning, down from just under 0.56 this time yesterday.

With stocks on the back foot, bonds were generally bid, but not Italy’s with the Italian Senate confirmed two Eurosceptics to head up the Parliament’s Finance and Budget committees. Italian two year yields jumped 26.7bps to 0.861% and its 10s by 18.3 to 2.732%, running against the tide of mostly lower yields in Europe and the US, expect in the UK short end and some spillover from Italy into Spanish and Portuguese yields. The market is alert to the history that the two appointees have both made suggestions that Italy should leave the euro. There is the assurance from new Finance Minister Tria that Italy will abide by EU rules and has no plans to leave the euro. League leader and Deputy PM Salvini said yesterday that he aimed to lower the retirement age for pensions, setting up a potential confrontation with the EU later this year if the coalition chooses to go down that route.

The Euro was sold lower on the appointments news but has since rebounded to over 1.16 from the lower 1.15s as support for the USD has faded somewhat, trade tension music a little more comforting. For what it’s worth, the Philly Fed survey printed on the lower side for June at 19.9 (29 expected; L: 34.4) though weekly jobless claims remain low. Fed President Kashkari (non-voter this year) said that the US is not at maximum employment until wages pick up and that he doesn’t see any signs of overheating.

Though all of the above, the AUD is off its lows but remains stuck for now below 0.74. The USD/CNY rate was pushed further higher yesterday – weighing on the AUD yesterday – while there is market talk that the Chinese authorities might reduce reserve requirements to ease business credit costs. Support for the economy perhaps, if at the margin at this point. It’s a quiet’ish week ahead for AUD data with RBA Credit for May the only release of note and not due till next Friday, under watch for what it discloses about housing and business credit, recently trending in opposite directions. There’ll be continued focus on local short end rate pressures with quarter end approaching.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.