Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Markets react firmly to the US decision on the Iran Deal and the news the markets don’t want to hear about the Italian government.

https://soundcloud.com/user-291029717/us-treasury-yields-stocks-and-oil-up-on-iran-decision-fallout

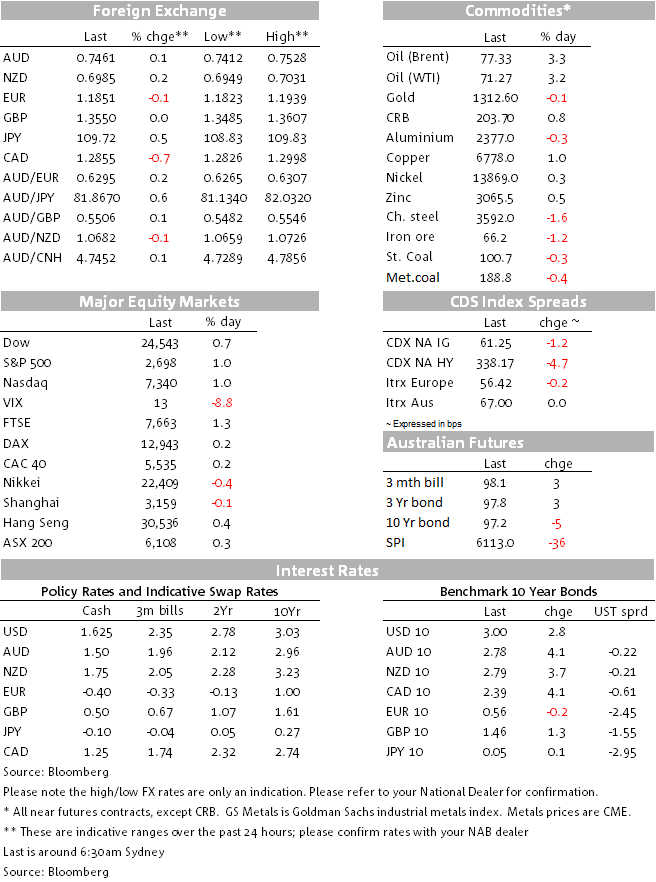

I was tempted to go with Midnight Oil for today’s title, but in then end Dark Energy, the first single from The Cult’s tenth studio album (2016) won the day. Price action over night has been all about the jump (+3%) in oil prices following yesterday decision by President Trump to pull the US out of the Iran nuclear deal. 10y UST yields have climbed above 3% and US equities have rallied with gains led by energy and financial shares. After edging higher during our APAC session, USD indices are unchanged with Nordic and commodity link currencies the outperformers overnight.

Oil prices have climbed over 3% in the past 24hrs with both Brent (@$77.32) and WTI (@$71.27) now trading at levels not seen since late November 2014. After yesterday’s decision by President Trump to pull out of the Iranian nuclear deal and reinstate sanctions on Iran, oil prices embarked on a steady rise aided as well by overnight news of an unexpected drop in US stockpiles, reinforcing the notion that the oil market is tightening and hence vulnerable to a reduction of Iran crude supply.

For now the focus appears to be on the potential reduction in oil supplies assuming Iran is unable to sell its oil to the market. However, sanctions are only coming into effect in 180 days, Europe, India and China have been the major buyers of Iranian oil and it is unclear if they will stop buying. On the subject, US Treasury Secretary Mnuchin said overnight that “we have had various conversations with various parties about different parties that would be willing to increase oil supply to offset this…my expectation is not that oil prices go higher.” Shortly after Trump’s decision Saudi Arabia released a statement saying that it would work to “mitigate the effects of any supply shortages”, raising the prospect that it could raise its own supply.

So despite the uncertainty, the market has run with the view that Iranian sanctions are yet another source contributing to the ongoing tightening in the oil market. Meanwhile the geopolitical implication have also seemingly taken a back seat, if sanctions are impose does that mean Iran restart its nuclear programme? If so, what do Israel and Saudi Arabia do about it? Talks over the next 179 days are going to be critical in this regard.

So the move higher in the oil prices has contributed to the rise in 10y UST yields back above 3%. That said the move higher has not just been led by breakevens, the real rate has also edged higher. The US PPI released overnight came a little bit below expectations (ex-food and energy Apr 2.3%yoy vs. 2.4% exp.), but given its low correlation with CPI (out tonight, see more below) the impact on markets was rather muted. The 10y UST treasury auction saw decent demand, mainly supported by dealers while indirect bidders (proxy for offshore CB demand) interest was below average.

Higher oil prices also played into the US equity performance overnight with the energy sector (+2.03%) leading the gains in the S&P500 (0.97%). The move higher in UST yields has contributed to the gains in financials (1.50%) while news that North Korea had released 3 captive US citizen played into the feel good/risk on environment, dragging the VIX index sub 14.

Yesterday in our APAC session the USD was in the ascendency with USD/JPY leading the way and flirting with a break above ¥110. The AUD was also under pressure trading down to a low of 0.7413 just after 5pm Sydney time. But the improvement in risk sentiment and move higher in oil prices has helped the AUD pair back all of yesterday’s losses with the pair now trading at 0.7463. The AUD continues to prove new lows for the year, but our fair value model is telling us that the decline in the currency is starting to look stretched, so for now we remain weary of chasing the AUD lower from here.

This morning the RBNZ left its cash rate unchanged as expected, but it appears slightly dovish at first glance. Our BNZ colleagues note to their surprise that the medium term inflation track is tad lower. Given the RBNZ’s TWI track which is higher than where the currency currently stands, this might explain the CPI projection. The other surprise is that the Bank said up front that “The direction of our next move is equally balanced, up or down”. This will become the market focus and so it’s not surprising that the currency is falling a little bit post the announcement, NZD now trades at 0.6934, 46pips lower relative to pre RBNZ levels.

Lastly SEK has been the outperformer overnight +1.31%, seemingly still benefitting from the less dovish tone from the central bank’s minutes of its April meeting released on Tuesday.

Looking at other news overnight, former Italian Premier Silvio Berlusconi said he is open to the formation of a government by the anti-establishment Five Star Movement and the euroskeptic League. This may put Italian bonds and the Euro under [pressure today as Berlusconi’s support opens the prospect for an anti Europe and populist administration in Italy.

Market prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.