Long-term signal vs. Short-term noise

Insight

President Trump has been making headlines with peace treaties and trade pacts, but what if they don’t happen? North Korea has threatened to pull out and now the President is saying the China talks may not be successful.

https://soundcloud.com/user-291029717/trumps-headlines-may-not-come-to-pass

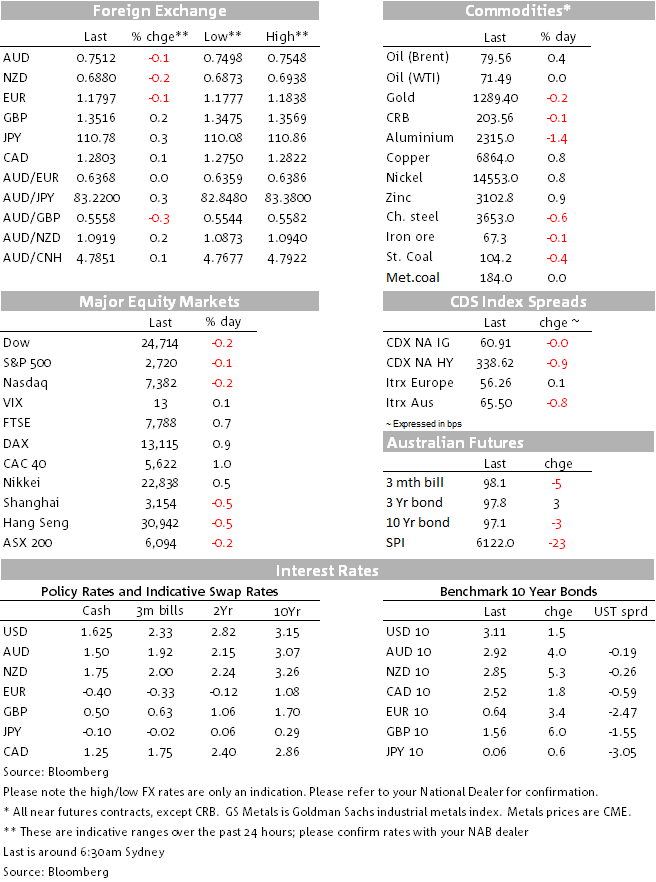

Amid a range of uncertainties from Italian politics, North Korea’s tantrum, US-China trade talks, NAFTA, Brexit and ….let’s not forget Iran, market moves overnight have been relatively subdued reflecting a wait and see mode by investors. The Waiting by the late Tom Petty made it to today’s title, apparently this song took him a long time to write and it’s about waiting for your dreams and not knowing if they will come true. So with that in mind, US equities have ended the day marginally in the red, the USD is essentially back to where it was this time yesterday and the UST treasury curve is steeper with the 10y tenor closing the session at 3.11%.As we are about to press the send button, headlines are hitting the screen suggesting China is set to offer the US $200trade deficit reduction, if true that would be a big positive for market sentiment.

After heading south during our APAC session yesterday, USD indices are now a smidgen higher with GBP the only G10 currency that has managed to outperform the greenback. The pound has been on a bit of a roller-coaster over the past 24hrs amid conflicting reports on the UK government internal Brexit negotiations. Yesterday reports of a backstop plan which would entail the UK remaining in the Custom union saw the currency trade up to an intraday high of 1.3569, then the pair traded to a low of 1.3476 amid conflicting reports over the validity of the agreement. Eventually, PM conceded that her cabinet has agreed to a backstop plan for the UK to remain tied to a customs union with the EU after 2021 until an alternative to having a hard border in Ireland can be found. The market has treated the news as a positive Brexit step, taking GBP up to 1.3516 where it currently trades. Nevertheless, it is unclear whether there is public support for the UK staying in a customs union and we suspect political wrangling is likely to keep GBP volatile for a while still. The EU summit late in June is a soft deadline, but realistically the political wrangling could go on until October/November before a proposal must submitted for EU approval.

Staying with Europe, after trading down to an overnight low of 1.1777, the euro recovered a bit ground (now trading at 1.1796) following news that Italy’s Five Star/Northern League coalition had completed a government agreement with a briefing of the programme revealing a series of social reforms as expected (such as tax cuts, a basic income for poorer Italians, and roll back of pension reform), but importantly there was no mention of ECB debt write offs. The omission boosted the euro and help BTPs (Italian Sovereign bonds) reversed some of the losses incurred over the previous 24hrs. Both leaders plan to ask party members to vote on the plan over the weekend before they present it to President Mattarella next week. We think the Italian uncertainty (debt issue and push for an easier path to exit the EU) is likely to linger on for some time suggesting there is more downside risk for the currency near term.

Moving on to trade news, NAFTA negotiations remain ongoing and although we had good sound bites from both Canada and Mexico, suggesting a deal still looks likely, now the deadline has been pushed towards the end of May, but then Mexico’s Economy Minister Ildefonso Guajardo added that if no agreement is reached the talks could extend beyond the July 1 Mexican presidential election. The CAD is little changed at 1.2806 with the NAFTA uncertainty offset by the move higher in oil prices. WTI traded above the $80 mark, but it has since eased back to $79.5. Overnight we had news that the EU seems to want to keep the Iran nuclear deal aliive, but also states US sanctions will be felt on EU firms. On that score, we also had news overnight that Total, the French group that has led foreign groups back into Iran, has decided to pull its investments out of the country, so even if Iran can sell its oil, it may not have much to sell.

After an up and down APAC session the AUD now trades at 0.7512, a tad lower over the past 24hrs. Yesterday the Australia’s unemployment ticked up another 0.1% to 5.6% despite the fact that 22.6k jobs were created in April (slightly above the 20k expected by the market). We know the RBA will interpret the data as it is and therefore it will likely conclude that spare capacity remains in the labour market. So this week’s data (wage growth and employment) do nothing to alter the market’s view that the RBA is on hold until well into next year (a full 25bps hike is not priced until Jul-19).

The NZD is down 0.3% for the day to 0.6877, with gains during the local trading session more than wiped out overnight as sentiment for the USD turned around. The NZ Budget confirmed much of what we knew already – that NZ’s fiscal accounts remain in great shape, with the government projecting modestly rising operating surpluses and lower net debt to just below the 20% of GDP target. While it looked like the NZD caught a bid after the announcement and almost reached 0.6940, this coincided with a particular period of general USD weakness. The growth dividend, winding back the previous government’s tax cuts and accounting for a more moderate reduction in debt is allowing the new coalition government to achieve its pre-election spending plans while at the same time keeping NZ’s fiscal accounts in rude heath.

Looking at UST yields, the 10y tenor is at 3.11% – a touch under the high reached in Asia yesterday and the 2y yield is around 2bp lower at 2.57%. The 2y10y UST curve now trades at 54bps, 11bps higher relative to last Friday’s closing levels. Higher oil prices and strong US data releases appears to have swang momentum towards steepeners, easing concerns of US recession risk. On this last point we note that overnight the Philadelphia Fed manufacturing index blasted up through expectations. The new orders component reached a 45-year high while the prices received component reached a 29-year high. It adds to the flavour of US economic data doing better than other regions at present, alongside a positive inflation dynamic

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.