Total spending grew 0.9% in June.

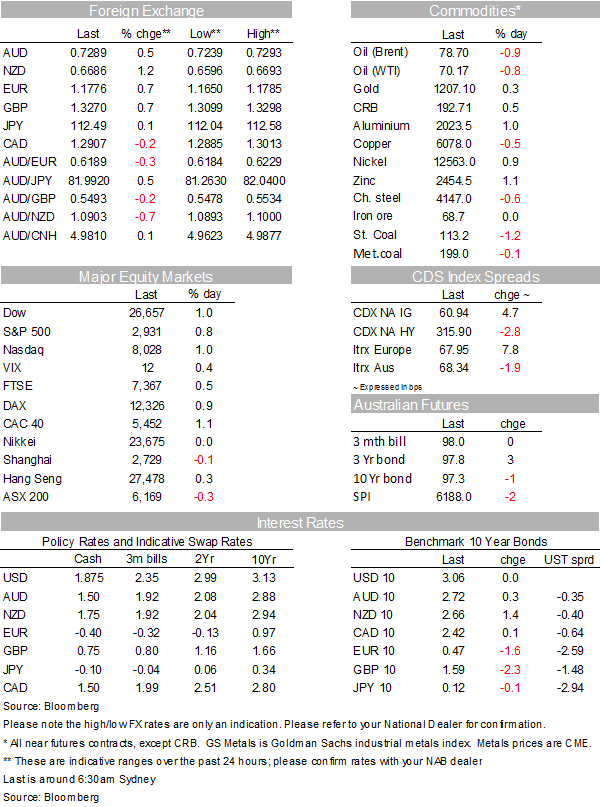

The US dollar is down this morning even though equities are at record highs.

https://soundcloud.com/user-291029717/why-the-us-dollar-is-falling-chequers-wont-work

It’s been another overnight risk-on session, US equities reaching new records, Treasury yields trivially higher, but the USD continues its retreat seen over recent days. Data released over the past 24 hours has been positive in NZ, the UK, and in the US adding some more support for the risk-on mood. The Norges Bank lifted rates for the first time in seven years but downgraded its longer term rate expectation. The NOK under-performed.

While the USD has been on the back foot again, the two currencies that have out-performed over the past 24 hours have been the Kiwi and Sterling.

The NZD jumped 40 pips from 0.66 on the release of the much stronger than expected Q2 GDP, up 1.0%, double the RBNZ 0.5% forecast and the strongest in five years. It was right at the top end of economists’ expectations, the market also alert to a possibility that some recent under-performing data might have spilled over to the GDP report, which was not to be. The Kiwi continued to garner support through the APAC session yesterday and further overnight as the USD retreated.

The strong data dampened market expectations for future NZ OCR rate cuts, with OIS pricing for the August-2019 meeting up 3bps, to now suggest “just” a 25% chance of a rate cut by then. The 2-year swap rate ended the day up 3bps to 2.035%, while 5-10 year swap rates were up in the order of 4-4.5bps. The sustained strength of the NZD spilled over into a higher NZD up on all the key crosses, ranging from 0.2% against GBP and EUR to 1.3% on NZD/JPY.

The other currency that has performed well has been Sterling. The currency was pushing higher into the release of the August Retail Sales report, benefiting from the pull-back in the USD and some tailwinds from what appeared to be a more conciliatory EU attitude to Brexit over recent times in the lead up to the Salzburg EU summit dinner the night before. Retail Sales surprised in a large way to the topside, Retail Sales in August on an excluding fuel basis up 0.3%/3.5%, well above the -0.2%/2.4% expected, Sterling’s positive reaction also assisted by upward revisions.

PM May then held a press conference early afternoon to report on the Salzburg meeting that by all reports was apparently quite a testy affair. Despite all the apparent bonhomie of late, it seems that the UK and the EU have reached an impasse over the EU. (Have a listen to Gavin Friend’s wrap on this morning’s podcast for more; email if you’d like to get the Podcast, but don’t already.) The lead story on the FT was “EU ambushes May over Brexit plan”. EU leaders warned PM May that her economic plan for Brexit “will not work” and gave her four weeks to save the exit talks. French President Macron said that “no blind deal” will be done with the UK and that Brexit must hurt and only liars said it would be easy. PM May is now working on a new proposal on Northern Ireland to take back to the EU shortly.

The AUD has made some further incremental gains. We note that among other statements yesterday, China announced that it could be cutting import taxes (tariffs) for a majority of its trading partners as early as next month (US included?). The AUD/USD is trading just above 0.7290 this morning.

The US economy reports again painted a positive picture of the US economy. The Philly Fed index for September beat expectations (though some analysts suggest its level and the lower Empire State reading points to a lower ISM this month after the over-60 reading last month), weekly jobless claims were the lowest since the Apollo 11 moon landing, while US household net worth rose again in Q2, aided by stellar stock market and higher house prices, nice sweet support to consumer spending. Also, and something I’m back to watching more, the Conference Board’s Leading Index was up another 0.4% in August, pointing to a further extension of the cycle.

The Norwegian central bank raised rates for the first time in seven years, lifting its deposit rate from 0.50% to 0.75%. The hike was entirely expected, coming with guidance that another hike is likely coming in early 2019. But the NOK lost some ground against the Euro, the central bank saying that it expects the key rate to be at 1.22% by the end of next year, down from 1.26% in its previous forecast and some expectations for a higher rate path.

Oil prices were somewhat lower overnight, base metals were generally higher (copper the exception), as was gold, while iron ore and coal prices were a little lower yesterday. Trump teed off against OPEC, saying: “We protect the countries of the Middle East, they would not be safe for very long without us, and yet they continue to push for higher and higher oil prices! We will remember. The OPEC monopoly must get prices down now!” There’s been little change in major bond markets overnight, US Treasury yields little changed, 2s up 1.27bps to 2.8034%m but 10s unchanged at 3.0626%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.