Total spending grew 0.9% in June.

Zombie was one of the Cranberries’ biggest hits and though written about what O’Riordan described as the seemingly interminable fight for Irish independence, it’s a fitting description of the US dollar, which more and more resembles a dead man walking.

I must admit to having had a bit of a crush on The Cranberries lead singer Delores O’Riordan, who had one of the most astonishing voices of the 1990s rock scene and was particularly saddened to hear this morning of her untimely demise at the age of just 46. Zombie was one of the Cranberries’ biggest hits and though written about what O’Riordan described as the seemingly interminable fight for Irish independence, it’s a fitting description of the US dollar, which more and more resembles a dead man walking.

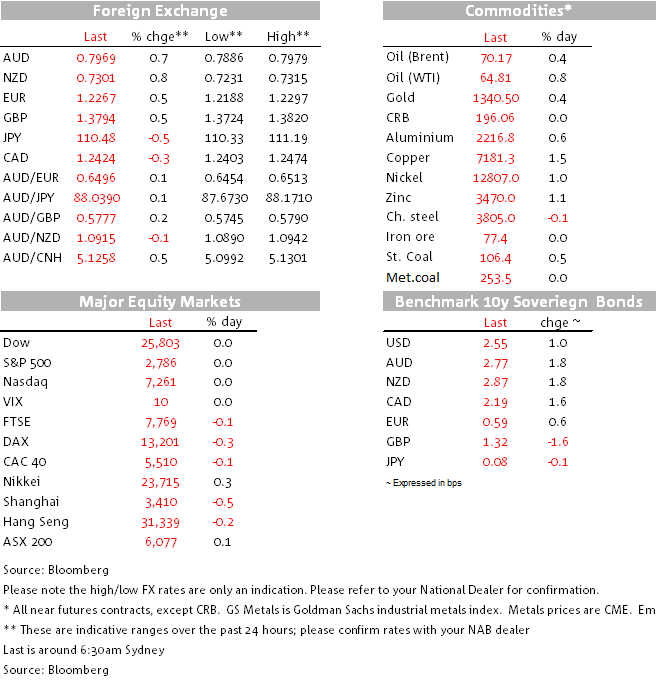

Overnight we’ve seen the broader BBDXY index join the narrow DXY is pushing (just) through its 2017 lows on a closing basis, to its weakest since the start of 2015. The US Martin Luther King holiday has evidently proved not to be a constraint on ongoing and fairly indiscriminate dollar selling.

It’s the NZD quite closely followed by the AUD that top the G10 leader board since yesterday’s Wellington open, up by 0.9% and 0.7% respectively, AUD/USD to a high of 0.7979 (0.7968 now) and NZD to 0.7315 (0.7301 now). Commodity price tailwinds continue to support Aussie and Kiwi even though we see these as part and parcel of ongoing US dollar weakness. Brent crude closed in London above 0$70 for the first time 2nd July 2015 and every single precious and industrial metal price is higher (lead, +2% and copper +1.4% leading the way).

Thursday’s China December activity readings will provide the next (non-USD related) test for the veracity of the commodity price rally, that we are already concerned about given the further slowing in China credit and money supply growth indicated in the December credit statistics published on Friday night.

The Mexican peso is actually the strongest major currency overnight, up almost 1% and feeding off yesterday’s Axios report that President Trump was softening his line on NAFTA (this after reports last week of Canadian officials becoming increasingly fearful Trump was about to abandon it). NAFTA negotiations are due to restart next week, the same day that the Finance Ministers of the U.S., Mexico and Canada will all be in Davos for the World Economic Forum.

Given where MXN and CAD sit today, we’d judge there’s much more upside on USD/CADand USD/MXN from US abandonment of NAFTA that downside on successful renegotiation of the pact.

In the meantime the Banks of Canada looks set to lift rates for the third time in just over 6 months tomorrow weakening (to 1.25%). Such a move is 88% priced, so CAD reaction will be governed by the narrative surrounding a move, assuming of course there is one.

EUR/USD added the best part of a cent to its rally after we wen home last night to come within kissing distance of 1.23 (high 1.2297). This high came soon after comments from the ECB’s Hansson who said the ECB could end QE bond purchases in one step after September and that Euro appreciation was no threat to the inflation outlook. Mario Draghi might have something to say about that next Thursday.

The Banque de France has just joined the Bundesbank in saying it is investing part of its FX reserves in the Yuan. No surprise to be reading that this is being used as yet another excuse to be selling US dollars, the argument being that since the USD represents the lion’s share of FX reserves, most of the moves into CNY, as modest as they will be, are likely to be out of USD.

As for Sterling, it has lagged the Euro move but not by much. To the extent that its recent run up was in part driven by reports late last week that Spain and Holland favoured a ‘soft’ Brexit, there might be some adverse reaction to the current FT lead story saying that the EU has toughened up its conditions for a post-Brexit transition deal for the UK, demanding that Britain abide by stricter terms on immigration, external trade agreements and fishing rights for nearly two years after it leaves the bloc

The FT says the revised “directives” drawn up by EU member states for Michel Barnier, Brussels’ chief negotiator, complicate the talks by giving him more precise instructions on several politically sensitive topics for the UK, according to a draft seen by the Financial Times. These include extending free movement rights and a special status to all EU citizens arriving before the final day of the transition at the end of 2020. It also requires that British ministers seek “authorisation” from Brussels in order to continue benefiting from EU trade deals that it would otherwise fall out of on Brexit da

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.