Long-term signal vs. Short-term noise

Insight

The NAB Corporate Cash Index draws on our own Corporate and Institutional Banking client insight analytics to reveal cash management trends.

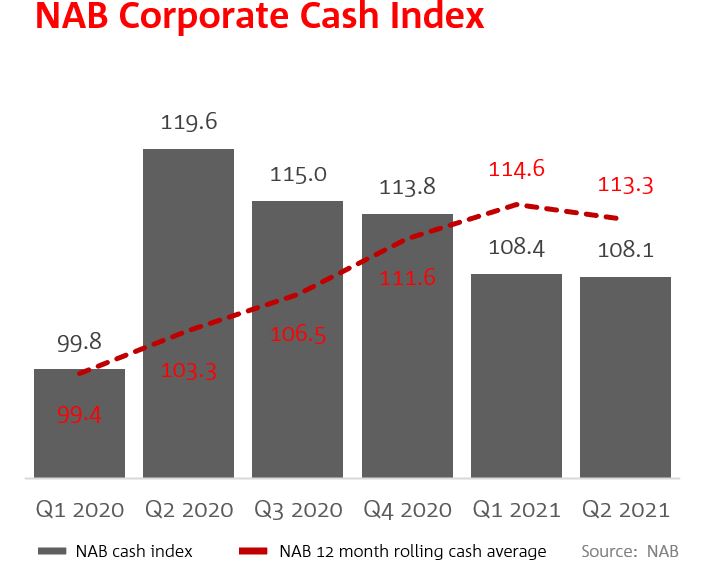

Cash holdings stabilised across Corporate and Institutional businesses during the second quarter of 2021, with the smallest recorded quarterly movement in the last three years.

Reducing by 0.3 points to 108.1 this quarter, compared to the pre-COVID average movement of 2.8 points.

At a headline level, this modest shift in cash holding is in contrast to the Australian Bureau of Statistics’ company gross operating profits growth of 7.1% in Q2 2021. However, behind the headline, we are seeing one third of industries increase cash holdings from strong business performance.

And 53% of industries maintaining cash holdings within 2% of their Q1 level.

Fluctuations in the Cash Index of less than 3 points (period on period) are considered to be tactical and not indicative of strategic shift in cash holding appetite.

Our data shows that the QoQ movement in the 12-month rolling cash average was 1.6 pts (113.3 vs 114.6), suggesting the move was primarily tactical in nature.

Looking forward and against the emerging backdrop of accelerating COVID-19 cases on the south-east coast of the country, and the potential for continued heightened uncertainty around the operating environment ― the risk of Corporates returning to a position of caution and conservatism towards capital, funding and liquidity in the near term remains elevated.

Exceptional economic uncertainty and cashflow vulnerability in Q2, 2020 drove the global rush to build cash.

This had the effect of pausing many important and necessary capital management initiatives – for example investments, buy-backs and acquisitions and instead bringing forward initiatives to bolster the balance sheets of businesses caught in the eye of the storm.

A combination of assets sell off, dividend reductions, pausing of share buy-back programs, reducing capital expenditure, compression of working capital and accessing rights issues for cash injections from shareholders were a feature of the past year.

These actions pushed the cash index to its peak at 151 index points.

While the sentiment was more balanced between risk and return at the March and June quarter, ‘lower-for-longer’ interest rate environment, interest rate targeting and overnight cash rate reduction have narrowed Corporates’ options for capital productivity, stability and asset returns.

At the June quarter, cash continues to flow into at-call, now representing 61% of total cash holdings for corporates ― a vast difference to pre-COVID levels.

Corporates entered 2021 with better balance sheet positions. And at the June quarter, we are seeing evidence of clients who are managing well through the pandemic starting to carry surplus cash balances in their medium to longer-term cashflow forecasts.

Firms are moving to delineate their cash between at-call and longer-dated, to take advantage of higher rates further up the yield curve.

This trend is not broad-based, but highly client and sector specific. At the June quarter, 40% of industries increased term deposit holdings with Retail, Mining and Wholesale leading the shift.

“Corporates generally continue to hold elevated cash positions given the environment. At some point, opportunistic forward looking businesses will begin to deploy that cash for growth and returns management.

In the meantime optimising the cash that is held, making it work as hard as possible for owners – has never been more important.”

Shane Conway, Executive, Transaction Banking, NAB

The sector continues to be the one of the ‘bright spots’ of the economy, however the run up in household spending is edging down.

Still a heady distance from pre-COVID levels, NAB consumer spending index for the June quarter reduced by 4.4 pts, landing at 123.9 pts. Q2 is now the fourth consecutive quarter where the consumer spend index is above 120pts; outperformance in consumer spending remains a key driver of higher cash holdings.

In line with contraction to consumer spending, cash balances have reduced by 50.7pts to 253.3pts vs. historical high of 304pts. Retail continues to maintain its position as cash standout and is the only sector sitting above 200pts.

Healthy cash balances and trading outlook are steering the sector’s cash strategy and cash mix towards yield. At the June quarter, investment in term deposit increased by 32%.

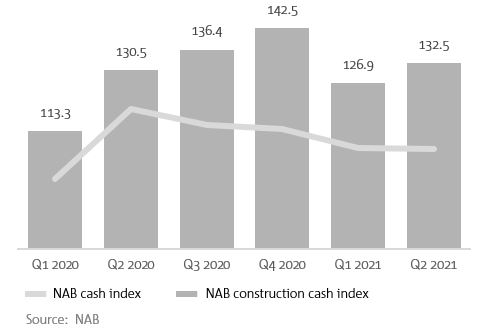

COVID-19 resulted in significant demand shock to the sector with widespread cancellation, slow down or a dry up of projects sending the already struggling sector into sharp contraction in Q2 2020.

COVID-19 resulted in significant demand shock to the sector with widespread cancellation, slow down or a dry up of projects sending the already struggling sector into sharp contraction in Q2 2020.

Low building activities from collapse of new orders, building site capacity restrictions, fall in selling prices and rising input costs sent the sector’s front-book revenue into existential spiral and the sector turned to debt to maintain cash buffers during Q2, 2020.

Contraction in the sector continued well in to August 2020, with expansion taking place in September 2020. House building has led the sector’s growth in the last three quarters with support from low interest rates, HomeBuilder and other state-based programs.

Cash holdings have averaged 125.8 index points over this period with a peak of 142.5pts in Q4. With strong revenue performance and outlook, the sector has reduced cash in at-call deposit products by 20% over the past two quarters, shifting non-operational cash to term deposits for capital yield and protection.

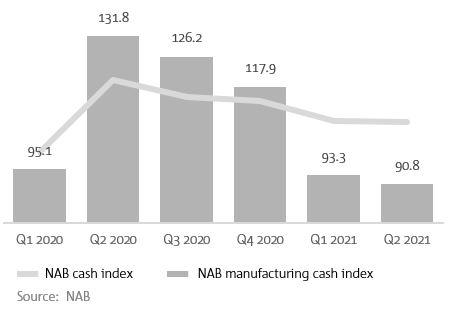

Cancellation of major orders, no new sales due to shutdowns, supply chain problems and increased prices for raw materials escalated into Q2 2020 being the most devastating quarter for domestic manufacturers.

Cancellation of major orders, no new sales due to shutdowns, supply chain problems and increased prices for raw materials escalated into Q2 2020 being the most devastating quarter for domestic manufacturers.

The sector’s initial response to the pandemic in Q2 2020, was consistent with the broader market, stockpiling cash to shore up balance sheets. Cash peaked at 131.8 index points and remained well above the overall index for Q3 and Q4, 2020.

For domestic steel manufacturers, strong global demand combined with global shortage have driven revenue uplift through latter stages of Q4 and into Q1 and Q2 2021.

The increased revenue, high demand and changes in Chinese steel output policy have provided significant increase in cashflow performance and outlook for the steel industry. The improved conditions have resulted in corporates investing cash surpluses into production, capital investments and growth-related activities with the manufacturing index subsequently dropping down to 90.8 index points.

“We’re now seeing variations in cash management strategies from our clients as the nuances of COVID-19 play out through each industry.

Clients in stronger cash earning sectors with greater cashflow predictability are now better positioned to accurately determine their level of surplus cash and revisit their cash segmentation and investment policy to optimise capital return.”

Johan Westh, Executive, Corporate & Institutional Transaction Banking, NAB

If you’d like to learn more about the NAB Corporate Cash Index for your industry, please contact your Transaction Banking Specialist or Relationship Manager.

Download a PDF version of the report

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.