Australian carbon project developers see a maturing of institutional financing as key to scaling the market and taking it on a similar trajectory as renewable energy.

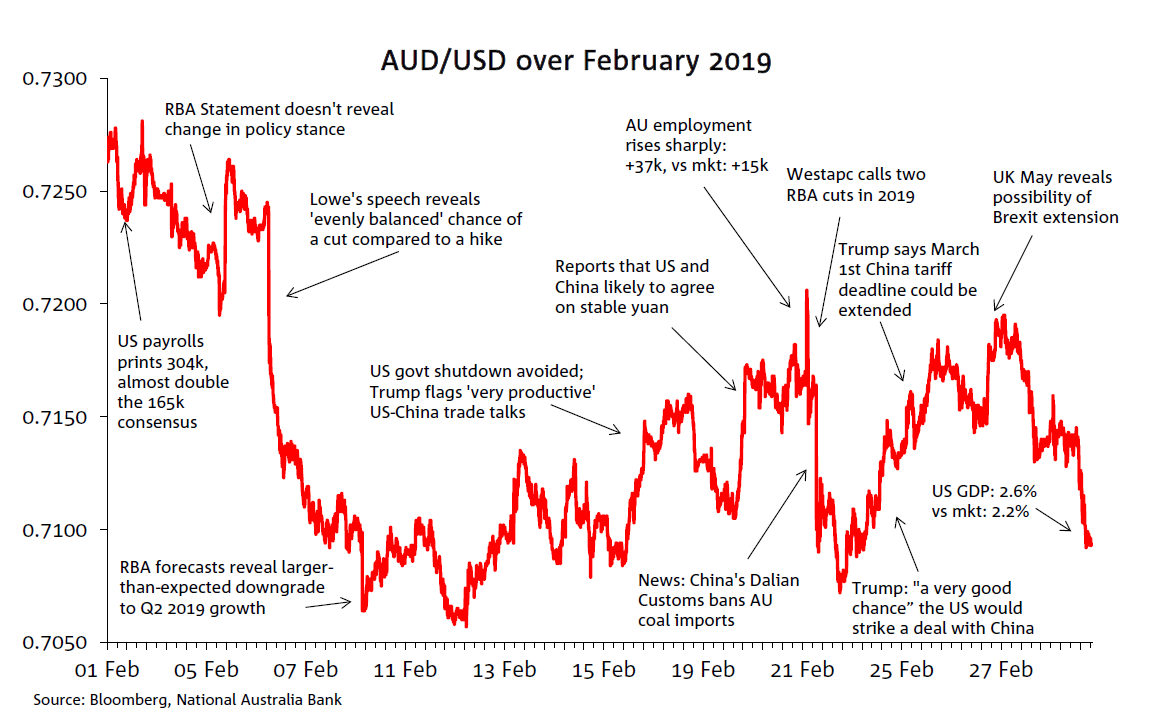

The AUD/USD was conflicted in February, as improvements in risk sentiment and higher commodity prices pulled the currency higher, but a softer domestic economic outlook and a more dovish RBA acted as an offsetting force.

Starting the month at 0.7265, the AUD/USD soon hit its monthly high of 0.7281 on February 2nd. However, it broke below 72 cents a few days later, after Governor Lowe revealed the RBA had removed its tightening bias, to spend most of February in the range of 0.7050 to 0.7200. The AUD/USD reached a monthly low of 0.7057 on February 12th and range traded thereafter, ending the month at 0.7094.

The RBA was the focus early in the month, as Governor Lowe’s first speech for the year (Feb 6th) revealed the Bank saw the chance of the next cash rate move being a hike or a cut as being ‘evenly balanced’. The shift in stance surprised markets, particularly given little change to the post meeting Statement the day before. The Governor’s speech triggered an AUD/USD sell off 1 cent to 0.7140.

After reaching its monthly low of 0.7057 on February 12th, the currency broadly trended sideways over the rest of the month, buoyant equity and commodity prices supported the AUD/USD following news that a US government shutdown had been avoided and reports suggesting a US-China trade deal was increasingly likely. Then on February 21st the AUD/USD came under renewed downward pressure. On the day a very strong AU employment print initially boosted the pair, only to fall sharply as Westpac announced its forecast for two RBA rate cuts in 2019 shortly after. Later in the same day, news that China’s Dalian customs were banning Australian coal imports saw the AUD/USD fall again, ending the day 0.73c lower at 0.7092. This news was later denied by both Chinese and Australian government officials.

Additional good news around US-China trade saw the currency move higher, with Trump suggesting a US-China trade deal was likely, as was an extension to the March 1st deadline for additional tariffs on Chinese imports (February 25th). Later in the month, softer than expected domestic data releases along with solid US data prints weighed on the AUD/USD with the pair closing the month at 0.7094, 0.37 cents above its monthly low.

The NAB AUD Model

Our AUD/USD Short Term Fair Value (STFV) estimate moved from a slight over valuation at the beginning of February to a mild undervaluation by the end of the month. That being said and as it was the case in January, the AUD/USD ended February comfortably inside its fair value range defined by +/- 1.5 standard deviation (spot at 0.7094 vs STFV at 0.7220)

Buoyant commodities prices, mainly supported by a 4.14% rise in oil prices, lifted our STFV by about half a cent in February. The improvement in risk appetite, evident by a 4 points decline in the VIX index to 14.78, was also a positive influence, adding another 0.3c to the STFV. Meanwhile, lower AU vs US rates, amid a shift to a neutral bias by the RBA, resulted in a 0.25c detraction in the STFV estimate.

Download the report for full the picture

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Australian carbon project developers see a maturing of institutional financing as key to scaling the market and taking it on a similar trajectory as renewable energy.

Total spending grew 1.2% m/m in May

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.