Online retail sales growth slowed in May following a fairly strong April

Insight

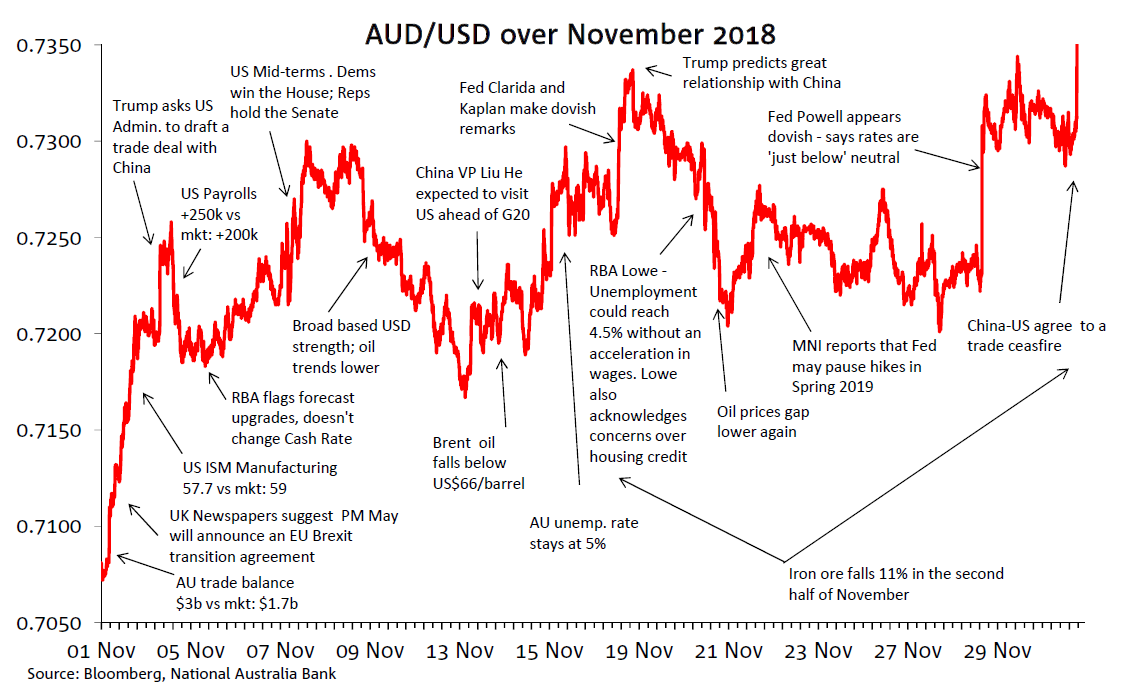

After rallying at the beginning of the month, AUD/USD mostly range-traded between 72 and 73 cents during the rest of November.

The AUD/USD tentatively halted its year to date downtrend in November; for the first time in 2018, the monthly low of 0.7072 (1st November) was not a fresh year-to-date low. Speculation over the US-China trade relationship, softer oil prices, Fed rhetoric turning dovish and a more cautious RBA were the main sources of volatility for the currency during the month. The G20 summit over the weekend culminated in a China-US trade ceasefire, boosting the AUD/USD at the start of the new month. In November, the AUD/USD traded in a 3.1 cents range, ending the month at 0.7306.

The AUD/USD rallied early in November, as strong trade data and risk-positive Brexit news saw the currency reach 0.7209 (2nd November). Having broken above 72 cents the AUD/USD mostly traded between 72 and 73 cents for the rest of the month. US-China headlines suggesting a trade ceasefire could be in the offing helped the AUD/USD trade higher while lower oil prices weighted on the pair. In the second half of the month a broader weakening in metal prices including an 11% fall in ore prices, also mitigated the currency’s attempts to trade higher. Softer China activity data alongside a decline in steel mill margins were key factors behind the softness in iron ore prices.

Dovish remarks by Fed speakers in conjunction with media reports suggesting a possible change to the current gradual Fed hiking plan weighed on the US dollar during the second half of the month. On the morning of November 29th, Fed Chair Powell added to the speculation by noting that interest rates “remain just below the broad range of estimates of the level that would be neutral for the economy”. This was a material change from his view in October when he noted that that “we may go past neutral, but we’re a long way from neutral at this point, probably.”

Meanwhile on the domestic front, the unemployment rate (Oct) printed unchanged at 5% and on November 20th RBA Governor Lowe suggested that the unemployment could reach 4.5% without an acceleration in wages. Lowe also acknowledges concerns over housing credit.

In early November AUD/USD rose above our short term fair value (STFV) estimate for the first time since mid-April. STFV was depressed in particular by the slide in oil prices while spot was supported by the above-mentioned Sino-US trade-truce optimism and revised thinking about the pace and magnitude of future Fed rate hikes. STFV ended October at 0.7217 and finished November at 0.7124, while spot rose from 0.7073 to 0.7330 to be just shy of ‘overvalued’ relative to our fair value range of +/- 3.2 cents (Chart 2). The rally in developed market stocks in November and associated fall in the VIX was a partial offset to the negative impact on STFV from the falls in commodity prices (Chart 3).

Download the report for the full picture

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.