Coming in for landing in a heavy cross wind

Insight

In a rapidly evolving technology landscape, corporate finance teams have a range of options to improve efficiency, productivity and security with bank communication.

Historically, making payments and getting bank transaction data was time-consuming for businesses, with little technology support for the function. Over the next decade, we expect the finance technology landscape to evolve dramatically. Businesses are already seeing replacement of on-premise legacy applications with either cloud infrastructure, or SaaS (Software-as-a-Service). Enterprise Resource Planning (ERP) systems will develop more real-time analytics, and bank connectivity will be enhanced to drive improved transaction and data exchange to support a broader range of business functions. So, what are the fundamentals a business should consider in this evolving landscape when it comes to banking?

Online platforms continue to be a key area of focus for banks as the primary electronic interface with their customers, with increasing access to self-service tools, customised reporting options and wider range of payment options.

In a single bank relationship, using a bank hosted platform is a low-cost and secure approach. Increasingly however, these platforms lack the range of reporting and analytics sought by finance teams. Many corporates with complex needs are increasingly leveraging more capability from their ERP system, or turning to specialised 3rd party Treasury Management Systems (TMS). A well implemented TMS can support the full lifecycle of treasury transactions and presents a consolidated view of all positions for a business. Day-to-day activities are performed more efficiently, as all data is centralised, with controls supported by the TMS.

Some banks are building out more specialised capabilities to address this gap, with enhanced cash and liquidity management platforms to drive better control and efficiency. The reality, however, is that there is still much manual intervention with spreadsheets by staff to address this.

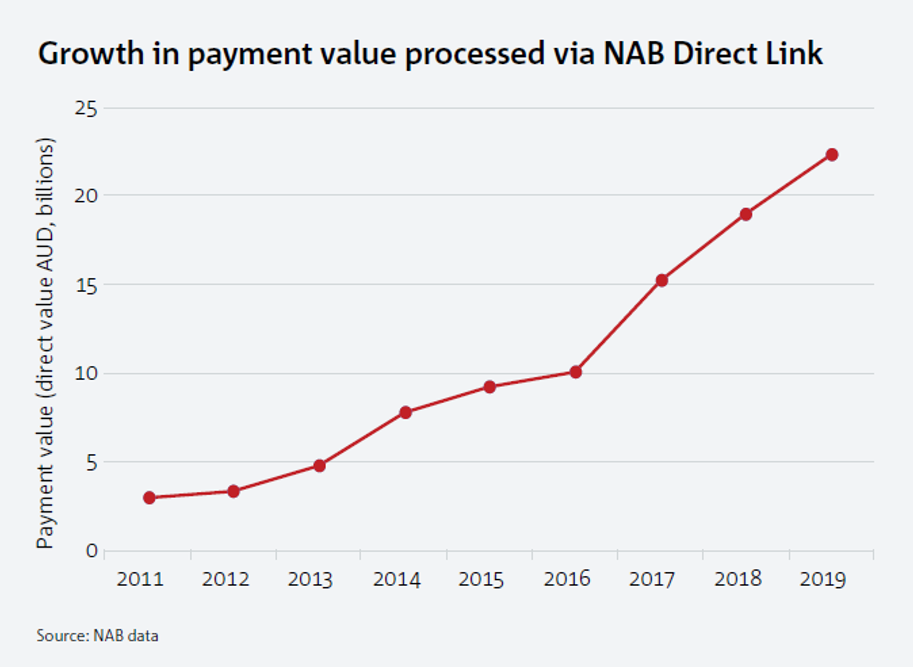

In an evolving technology landscape, other interfaces with banks are becoming more common. STP, where a client’s systems communicate directly with the bank’s system for payments and transaction data, was once purely the domain of large corporates. We now see this being more frequently implemented in mid-sized operations. Access to technology resources, an increased focus on fraud and standardisation of connectivity and messaging have contributed to this. STP does drive operational efficiency and security; however, it can be expensive to set up, so sometimes is not best aligned for multi-bank relationships.

For multinationals, direct integration to the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network is also a common approach. SWIFT is the common messaging network and standard for bank communication globally. This arrangement delivers a single point of integration with banks, using a standardised messaging structure. This can be costly however, and is usually only an option for corporates that regularly deal with multiple offshore banks.

Major ERP, accounting and billing platforms are trending towards API integration with banks. Simply put, an API is a small packet of data that is transmitted between two systems using a common language, and can easily be modified to align with business needs (eg payment instructions or account information). Banks are in various stages of opening their environments to APIs, with some offering mature developer portals today.

APIs are an example of how corporates can standardise connectivity and customise messaging with many banks in near real-time. Like STP, it is a 1:1 connection so requires configuration for each bank.

‘Open Banking’ captures the practice of securely sharing data between authorised parties on the request of a customer (data owner) . This is in place in the UK now, and given rise to many ‘challenger’ banks. In Australia, Consumer Data Right (CDR) legislation passed on 1 August 2019, and will take effect for the big four banks in February 2020.

Underpinned by API, data portability between banks, and the ability to engage third party fintechs for discrete functionality, products and services, open banking could herald a seismic shift in the role that banks play for business clients in future.

Other concepts around AI, robotics and Distributed Ledger Technology (DLT) will have implications for both corporate finance teams and their relationship banks, in terms of the data sought and its timeliness.

Corporates are faced with a broad range of technology options today for connectivity and finance administration. Themes of centralisation, automation and standardisation should be front of mind today and in the coming years.

In a rapidly shifting technology landscape, corporates need to have a clear strategy for not only their core business, but the technology systems, platforms and interfaces that underpin their operations. Banks, fintechs and solution providers will keep innovating at an increasing pace – paving the way for greater efficiency, flexibility, and profitability for corporate clients. Importantly, poor strategic choices on any of these technology fronts may drive the exact opposite effect.

This article was originally published in 2020 Outlook: Creating Opportunities- read the full magazine or download this article.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.