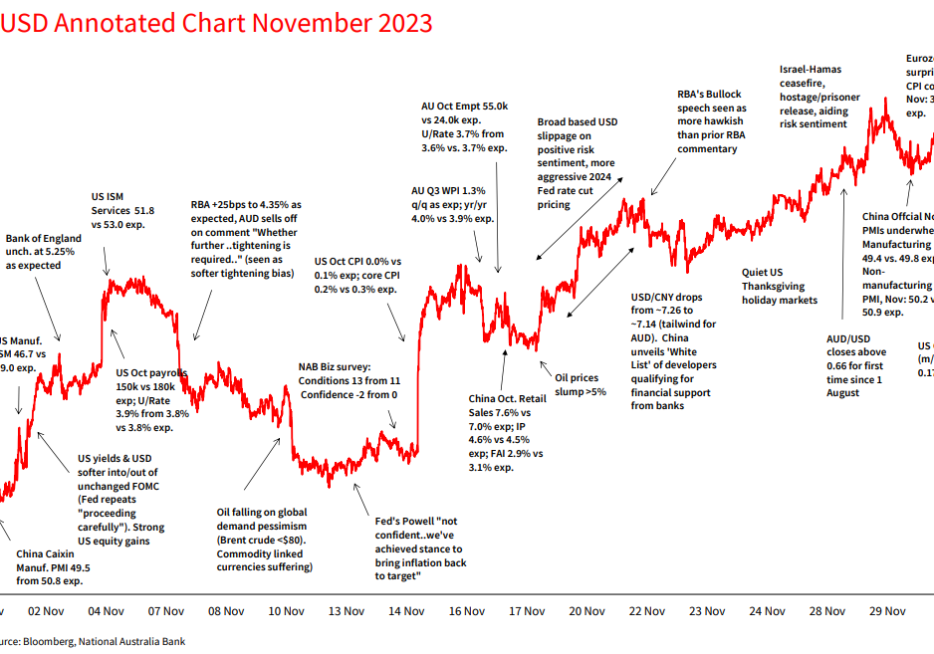

The AUD in November AUD/USD returned to ‘normal’ levels of monthly volatility in November.

Author

Rodrigo is a Currency Strategist and member of the FX strategy team at NAB. In this role, he contributes to the creation of trade ideas and research publications, and advises our internal and external clients on developments in global foreign exchange markets.

Rodrigo has lived and worked around the world. Before coming to Australia, he worked in London for Henderson Global Investors, firstly as the Head of Risk Measurement and then as a Quantitative Analyst in the Global Fixed Income Hedge Team. In 2009, Rodrigo made his move to NAB as an investment strategist within the private wealth division. He then worked in Rate Strategy for four years, before taking on his role today as Currency Strategist.

Rodrigo was born in Chile, and holds a Bachelor of Commerce, Honours and Masters in Economics from the University of the Witwatersrand in South Africa. He’s also a CFA charter holder, and has a diploma of Financial Markets (AFMA).

The AUD in November AUD/USD returned to ‘normal’ levels of monthly volatility in November.

After what has been a solid month for equities and bond investors, month end flows have probably play their part in the price action overnight, US equities have lost momentum, UST have led a rise in core global bond yields and the USD is stronger. US and European inflation releases favoured the notion the Fed and ECB are done with their respective tightening cycles.

US and European markets have begun the new week a subdued mood. But core global bond yields are showing some life, lower across the board while the USD is a tad softer too

Todays podcast US data not supportive of Fed’s inflation quest US Jobless claims fall well below expectations Final U of Michigan inflation expectations revised up UST curve bear flattens. 2y up 6bps to 4.93% US equities ignore data and keep marching higher Oil slips on news OPEC + meeting delayed. Saudis not happy USD […]

US equities start the new week in a positive mood, the USD has remained under pressure and after initially edging higher, longer dated UST yields edge lower supported by a well-received 20y Bond auction.

US equities recorded a solid end to the week with the S&P 500 closing above the 4400 psychological mark. Equity investors showed little reaction to news of a downbeat consumer

Risk assets had a solid end to the week with softer US economic data releases fuelling the notion that the Fed is done with the current tightening cycle. Front end yields led a rally in UST yields while the USD extended its decline to a third consecutive day.

European and US equities ended the week with a cautious tone. The S&P 500 extended its weekly decline to 2.53% and entering correction territory in the process. Weekend news that Israel has begun a ground invasion of Gaza suggest markets are likely to retain a cautious tone at the start of the new week.

US equities are lower led by the tech heavy NASDAQ index and not helped by a new surge in UST yields. The USD extended yesterday’s gains with the AUD at the bottom of the G10 board, reversing its post CPI gains.

Reaction to the Israel-Hamas conflict triggers a spike in energy prices while German Bunds lead a rally in European bonds with US Treasury futures also pointing to a decline in US Treasury yields. Not all the initial moves have been sustained. The USD is little changed, AUD is up, after being down with Fed speakers favouring holding rather than hiking rates, helping US equities rally while European shares fall.

Markets mark time ahead of payrolls tonight. Core global yields trade in narrow ranges, the USD loses a bit of altitude while US equities end the day little changed.

A better-than-expected US JOLT report provided rattled markets. US Treasuries led a rise in core global bond yields, equities traded lower and the USD was stronger. USD/JPY gapped lower ( official intervention?) and AUD was the notable underperformer.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.