Confidence and Conditions Lift

Insight

Todays podcast US data not supportive of Fed’s inflation quest US Jobless claims fall well below expectations Final U of Michigan inflation expectations revised up UST curve bear flattens. 2y up 6bps to 4.93% US equities ignore data and keep marching higher Oil slips on news OPEC + meeting delayed. Saudis not happy USD […]

Events round-up

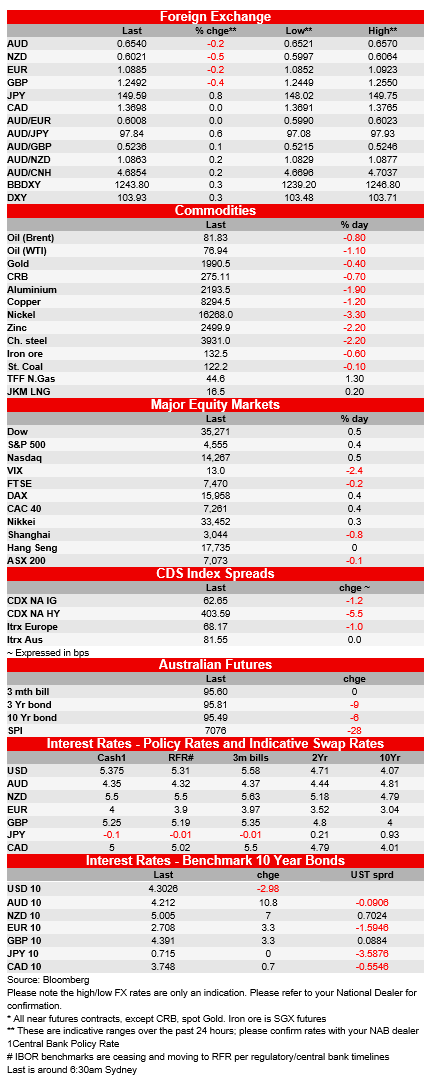

US: Initial jobless claims (k), wk to 18-Nov: 209 vs. 227 exp.

US: Durable goods orders (m/m%), Oct: -5.4 vs. -3.2 exp.

US: Durables ex transport. (m/m%), Oct: 0.0 vs. 0.1 exp.

US: U. of M. consumer sentiment, Nov: 61.3 vs. 61.0 exp.

US: U. of M. 5-10yr inflation exp., Nov: 3.2 vs. 3.1 exp.

Markets can be capricious sometimes and at the present junction investors are looking for clues confirming the Fed is done with its current tightening cycle, thus evidence to the contrary can be unsettling. Overnight second US tier data releases triggered a disproportional market reaction, US jobless claims and inflation expectations data did not support the story US inflation is easing against a weakening US labour market. Front end UST yields led a bear flattening of the curve, the data also gave the USD some broad support while US equities ignored the data, and extended their recent gains. Oil prices slipped on news the OPEC+ meeting has been delayed and last night RBA Governor Bullock emphasised Australia’s homegrown inflation challenge.

Ahead of the US Thanksgiving holiday, US jobless claims were released one day earlier with the new figures bucking the recent trend. Initial jobless claims fell to 209k from 233k, significantly below the consensus, 226k. Last week’s claims print was the highest in 12 week and the big reversal in the overnight figures now challenges the notion that claims are trending higher. The final reading of University of Michigan inflation expectations showed the year-ahead measure revised up a tenth to 4.5% and the 5-10yr measure remained at 3.2%, both measures slightly higher than the consensus. The latter was the highest since 2011, raising the risk that higher inflation expectations are becoming embedded.

The US data release triggered a more longer lasting reaction in the US Treasury market compared to the equity market. Front end yields led a bear flattening of the curve with the 2y tenor rising 6bps to 4.93% while the 10y Note edged up 3bps to 4.425%, after trading to an overnight high of 4.445%

In contrast US equities, showed little reaction to the “inflation disappointing” data. The S&P 500 opened higher, had a small wobble and then recovered, to end the day up ~0.4%, recording a six day rise in seven after yesterday’s small blip (down just 0.2%). The NASDAQ gained 0.46% and the Dow 0.47%. In company news, Amazon shares gained (~1.8%) ahead of the start of the holiday shopping season and Microsoft also rose (1.06%) on news Sam Altman will return to lead OpenAI. Nvidia’s shares dropped (-2.54%) after yesterday results. Earlier in the session Europe’s Stoxx 600 closed 0.3% higher with all main regional indices closing in the green barring the UK FTSE 100 which was -0.1%.

US Durable goods orders were also released last night. The October figures were softer than expected but this was ignored by the market. The headline fell of 5.4% m/m in October exacerbated by reduce aircraft orders. The core figures were flat and with downward revisions. Pantheon Macroeconomics estimates that real business equipment investment is on course for another decline in Q4, following the 3.8% annualised contraction in Q3.

The move up in UST yields triggered by the US jobless claims and inflation expectations releases, supported the USD across the board and arguably ahead of Thanksgiving it may well provided an excuse for traders trimmed their short positions ahead of the holiday break. The BBDXY and DXY indices gained ~0.3% with all G10 pairs losing ground against the greenback. CAD was little changed while JPY ( -0.83), NOK (0.7%) and NZD (-0.41%) ended as the notable underperformers. CAD was supported by the market re-assessing the BoC options, after good inflation numbers in the previous day, the BoC is likely to proceed carefully with any consideration of rate cuts next year. The move up in USD/JPY to 149.58 (this time yesterday the pair was at 148.39) was supported by higher UST yield while NOK’s retracement was weighed down by the decline in oil prices.

Oil prices are down 2-2½%, after the OPEC+ meeting scheduled for this weekend was delayed, with talk that Saudi Arabia is not happy with the production levels of other members – likely other countries are unwilling to cut production whilst Saudi Arabia is doing much of the work to contain supply. Brent crude is trading just over the USD80 mark.

NZD weakness is probably justified by the technical resistance at 0.6040/50 area. The Kiwi has struggled to break above this level in recent times and last night the barrier proved yet again to hard to overcome. NZD traded to a high of 0.6089, but now starts the day at 0.6020.

The AUD was also negatively impacted by the stronger USD, but a speech by RBA Governor Bullock which sounded on the hawkish side was supportive. The AUD is only down by 0.18% and starts the new day at 0.6539.

Last night RBA Governor gave a speech on A Monetary Policy Fit for the Future. The Governor explained that “the remaining inflation challenge we are dealing with is increasingly homegrown and demand driven” and “a more substantial monetary policy tightening is the right response to inflation that results from aggregate demand exceeding the economy’s potential to meet that demand”. • In the Q&A, Bullock said she expects a new Statement on the Conduct of Monetary Policy (SCMP) may be by the end of the year. Adding that the new SCMP will give confidence that “we are not just aiming for the cap, we are aiming to get to the midpoint” of the 2-3% target. NAB expects a hike in February, see here for more

Looking at other FX pairs, broad USD strength sees EUR back below 1.09 and GBP back below 1.25. On the latter, the UK autumn Budget was released last night and Chancellor Hunt offered up tax cuts (a payroll tax cut of 2%) alongside some business-friendly measures and increased pensions and welfare benefits (linked to the higher September CPI figure than October’s lower figure). This has been facilitated by higher inflation increasing tax revenue, with tax as a share of GDP still on a rising path, towards a 70-year high, and allows Hunt to meet his debt targets.

Jason Wong, my BNZ colleague, notes that opponents have criticised the Budget by not addressing the impact of higher inflation on public services expenditure that makes the rosier fiscal projections look unsustainable. The bond market has noted the Treasury’s higher inflation track compared to the BoE, and possible inflation implications of tax cuts, and sent UK rates higher, with the 10-year Gilt up 5bps to 4.15% against a backdrop of little change in European yields.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.