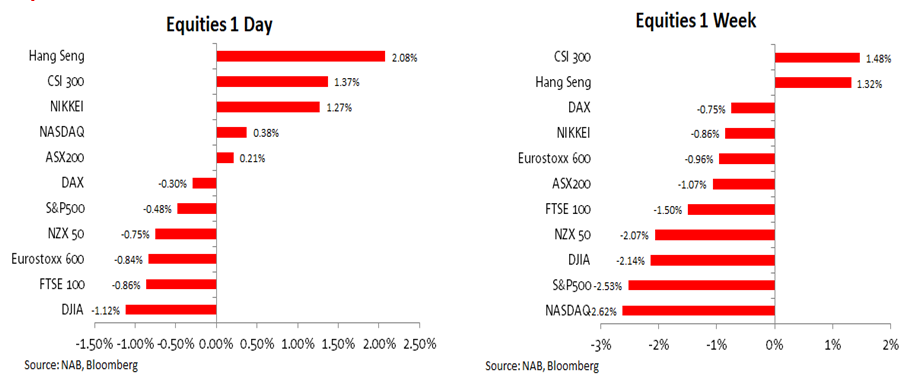

European and US equities ended the week with a cautious tone. The S&P 500 extended its weekly decline to 2.53% and entering correction territory in the process. Weekend news that Israel has begun a ground invasion of Gaza suggest markets are likely to retain a cautious tone at the start of the new week.

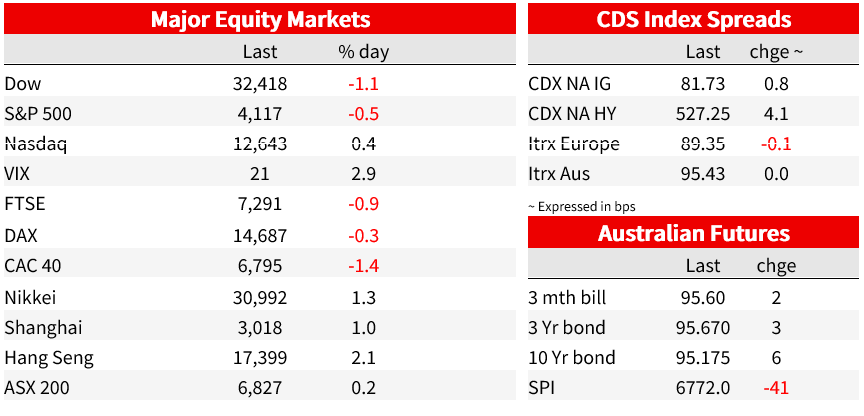

S&P 500 (-0.48%) extends decline and enters correction territory

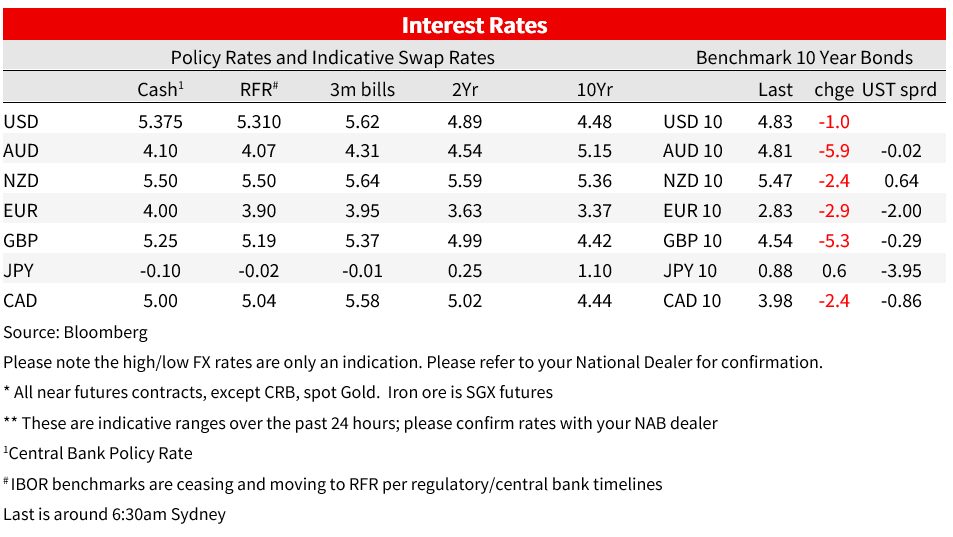

UST curve twists with the front and belly lower while long end yields trade higher

10y UST little changed. 1bps lower to 4.83%

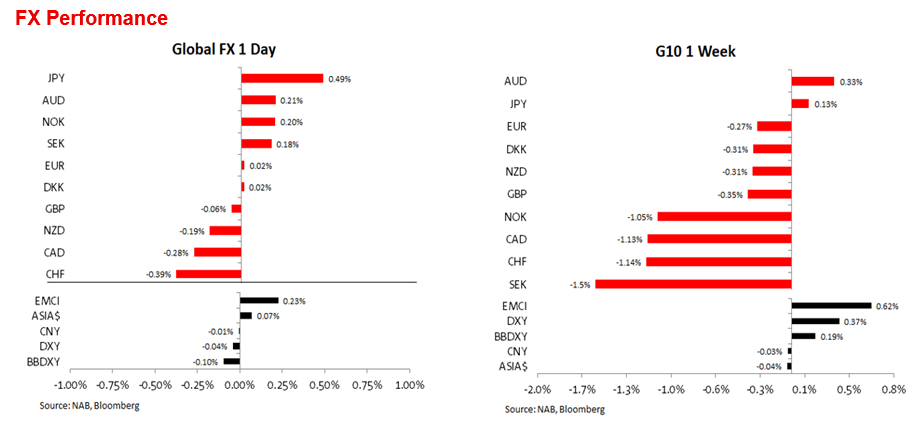

USD also little changed. JPY up on Friday, AUD best performer on the week

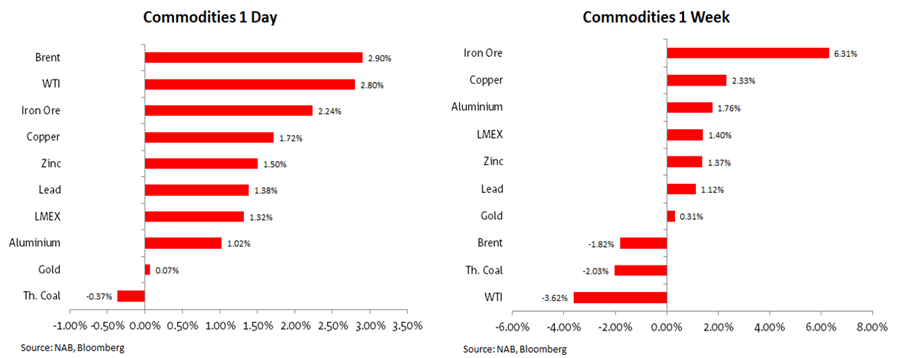

Oil prices gain over 2% (Brent above $90). Gold climbs above $2000

US September Core PCE +0.3% m/m, up from +0.1% – highest monthly reading in 4 months

U of Michigan – 1y inflation expectations jump 100bps to 4.2% in October

Weekend news: Israel begins ground invasion of Gaza

Coming Up Today: AU Retail Sales, German CPI and GDP

Rest of the week: BoJ, CH PMIs, US ECI, US ISM, FOMC, nonfarm payrolls

Events Round-Up

NZ: ANZ Consumer Confidence, Oct: 88.1 vs. 86.4 prev.

JN: Tokyo CPI (y/y%), Oct: 3.3 vs. 2.8 exp.

JN: Tokyo core CPI (y/y%), Oct: 3.8% vs. 3.7 exp.

US: Personal Income (m/m%), Sep: 0.3 vs. 0.4 exp.

US: Real Personal Spending (m/m%), Sep: 0.4 vs. 0.3 exp.

US: PCE Core Deflator (m/m%), Sep: 0.3 vs. 0.3 exp.

US: PCE Core Deflator (y/y%), Sep: 3.7 vs. 3.7 exp.

European and US equities ended the week with a cautious tone with the S&P 500 extending its weekly decline to 2.53% and entering correction territory in the process. Geopolitical risk emanating from the Middle East as well as underwhelming corporate earnings weighed on sentiment. Oil prices gained over 2% on Friday while Gold traded above $2000 market. Weekend news that Israel has began a ground invasion of Gaza suggest markets are likely to retain a cautious tone at the start of the new week. The UST curve twisted with yields in the front and belly edging lower while long end yields traded higher, the USD was little changed, JPY the outperformer on Friday, AUD the outperformer on the week.

The S&P 500 closed Friday 0.48% lower, recording its eight daily decline in nine days. The index is down over 2.5% on the week and looks set to record a third monthly decline, it has now entered a ‘correction’ having declined more than 10% from the peak near 4600 in July . The rise in global yields led by US Treasuries has triggered a reassessment on the equity outlook and more recently heightening geopolitical tensions have become an additional headwind with mixed corporate earnings reports not helping sentiment either.

Banks were notable underperformers on Friday (S&P 500 index -1.82%) with the KBW Bank Indexnow at its lowest level since September 2020 . Amazon, META and Intel Corp gained on Friday following better than expected earnings, helping the NASDAQ close 0.38% higher on the day, still the index was 2.62% lower on the week and down 4.36% month to date. Earlier in the session European equities also closed lower with the STX Europe 600 -0.84%.

Equities Performance

US personal income and consumption data along with the PCE for September were one of the key data releases on Friday with the final October University of Michigan survey the other one.Consumer spending, one key driver of economic growth, rose 0.7%mom in September, compared with a 0.4% increase in August. In real terms consumption was strong in July (+0.6%m/m, sa), slipped in August (+0.1%m/m, sa) and then rebounded in September (+0.4%m/m, sa). Consumer spending growth in September was much faster than real income gains, which rose 0.3%mom, the arithmetic implication resulted in the saving rate falling from 4.9% in June to 3.4% in September. That is lowest rate since December, indicating households used some of their savings to sustain their consumption, raising the question of whether this pattern can be sustained for much longer.

The University of Michigan final reading for October had one major surprise, its reading of one-year inflation expectations surged to 4.2%yoy, up from 3.2% the prior month. This was its highest since May while the measure of five-year inflation expectations was up two tenths at 3.0%. Commenting on the results survey director Joanne Hsu noted that “Although inflation is slowing, people’s concerns about inflation continued to rise,”. Looking at the details, expectations for gas prices a year ahead rose with an overwhelming portion of consumers expecting an erosion in their living standards.

The FOMC meets this week and after comments from Fed chair Powell and other Fed speakers, expectations are for the Bank to stand pat, but the recent uptick on inflation, consumer resilience and jump in inflation expectations, together suggest the Fed will retain a hawkish bias, leaving the door open for a hike in December and or January. Inflation and labour market data releases between now and then are going to be important, including non-farm pay rolls on Friday.

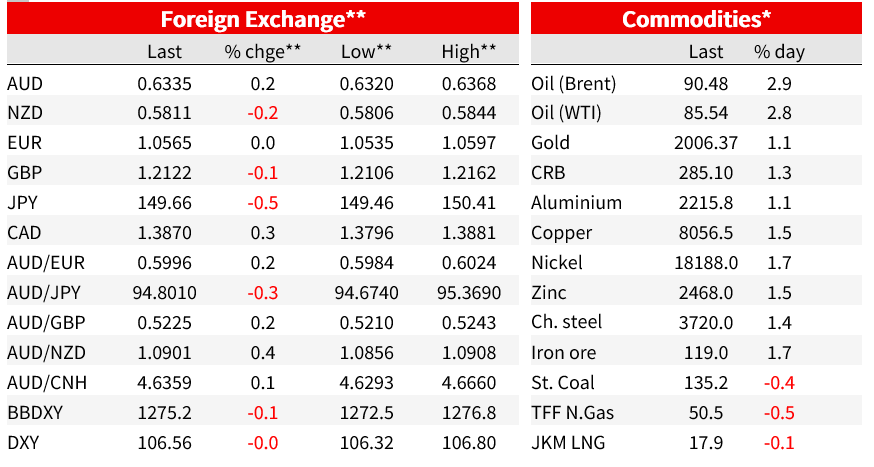

US Treasuries had a more subdued end to the week with the 10y rate little changed on Friday, down 1bps to 4.83%. The US Treasury curve twisted with front end yields edging a bit lower (2yr down 3.8bps to 4.89%) while the long end traded higher, 30y up 2.8bps to 5.016%. The modest steeping bias saw the 2y/10y curve close at -17bp which is close to its recent highs. European bond markets closed lower in yield. 10-year bund yields ended the week at 2.82%, down 3bp on the day, while 10-year gilt yields fell 6bp to 4.54%.

US Treasuries over the past week

The USD was little changed in index terms on Friday, but both the DXY and BBDXY indices gained on the week, up 0.37% and 0.2% respectively . Looking at G10 pairs, JPY was the outperformer on Friday with USD/JPY down 0.5% and the pair has opened the new week at 1.49.58. On Friday, Tokyo CPI (core CPI Oct: 3.8%yoy vs. 3.7% exp.), which can act as a leading indicator for nationwide data, was stronger than expected ahead of the Bank of Japan’s (BOJ) policy meeting tomorrow. Tomorrow the BoJ will have to upgrade its inflation outlook yet again and given JPY weakness and political pressure emanating from the cost of living, there is a good chance the Bank could announce another tweak to its yield curve control policy.

The AUD was another notable performer on Friday and indeed on the week. The pair gained 0.2% on Friday to be up 0.33% on the week. In what was a subdued week for FX markets, the AUD was the top G10 performer and now starts the new week at 0.6336, around the middle of the 0.6270 to 0.6511 range that has contained its price action over the past 30 days.

The NZD benefited from the temporary improved risk tone and traded to an overnight session high close to 0.5845. However, the move quickly reversed, and NZD/USD ended the week near 0.5810. The euro closed the week at 1.0569, down 0.27% over the past five days, the pound was little changed on Friday (1.2122) with CAD extending its weekly decline to 1.387 ( -0.28% on the day, -1.13% on the week). CHF was the underperformer on Friday (-0.39%) and on the week (-1.5%).

FX Performance

Oil prices gained over 2% on Friday with heightened geopolitical tension over the weekend suggesting more of the same is likely at the start of the new week. Gold gained just 0.007% on Friday, but notably it closed above the $2000 mark. The precious metal has gained ~9% since Hamas attacked Israel on October 7, bouncing back from a seven-month low as demand for haven assets increased. Iron ore and Copper were the other notable performers on Friday; indeed the former is the best performer on the week, up 6.3% and benefitting from the improvement in China’s growth outlook following last week’s news of an increase in fiscal spending.

Commodities Performance

Coming Up

Locally, the calendar is full with (second tier) data. Retail Sales is the highlight on Monday, where NAB looks for a 0.4% m/m gain. Other domestic data releases include Building Approvals (Wednesday), Trade figure (Thursday) and Retail Sales – quarterly volumes (Friday).

In NZ, employment data (Wednesday) is expected to show robust employment but a tick higher in the unemployment rate.

Offshore, BoJ is on Tuesday, the FOMC Wednesday, and the BoE Thursday.

Datawise, the US releases JOLTS, ECI, ISMs ahead of Payrolls on Friday. The Eurozone gets GDP & CPI data (Tuesday) and the German CPI is out later today. China releases its official PMIs on Tuesday and the Caixin version are out on Wednesday (Manufacturing) and Friday (Non-Manufacturing).

US Reporting season highlights include Apple, Airbnb and McDonald as well as Starbucks, VF Corp (owner of the Vans and North Face brands) and plus drugmakers Moderna and Eli Lilly & Co.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.