Total spending grew 0.9% in June.

US and European markets have begun the new week a subdued mood. But core global bond yields are showing some life, lower across the board while the USD is a tad softer too

Events round-up

US new home sales – 5.6% to 679K, below the consensus, 723K.

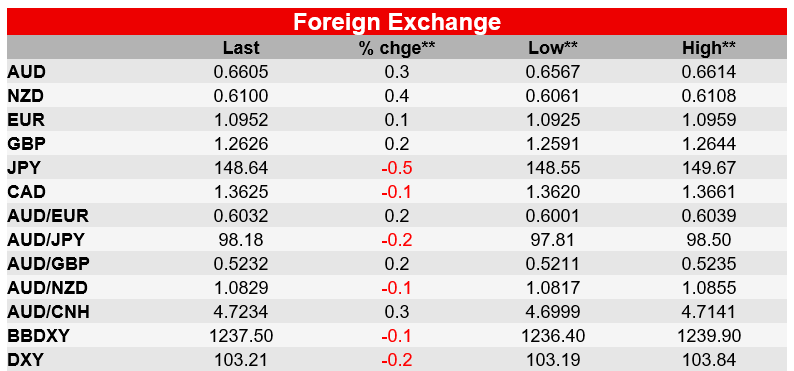

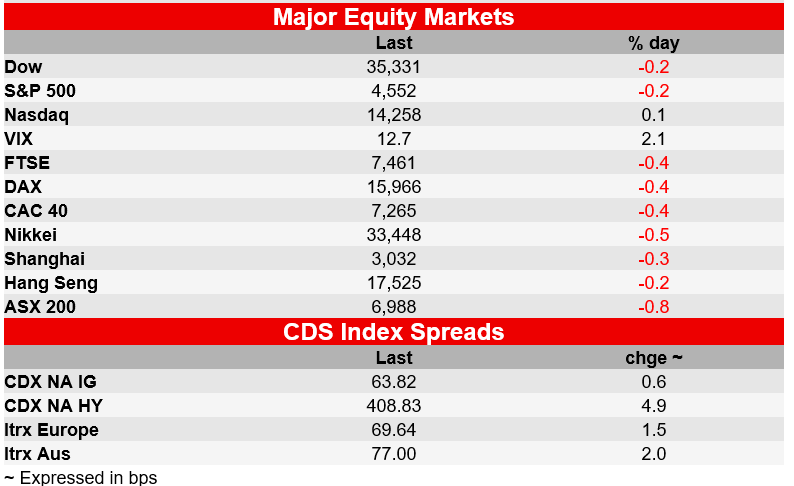

US and European markets have begun the new week a subdued mood. European equities have lost some altitude while in the US the S&P 500 is -0.22% and the NASDAQ is +0.06%. Core global bond yields are showing more life, lower across the board. The USD is tad softer too with AUD and NZD now trading above 0.66 and 0.61 respectively.

The S&P 500 has started the new week in the same fashion as it ended the previous one. November looks set to be a very solid month for equity investors with US stock yet again leading the charge. The NASDAQ is over 11% higher month to date while the S&P 500 is closed to 9%. That said, in recent days, both indices are showing a loss of momentum with the S&P 500 now essentially flatlining over the past three trading days. Technically the S&P 500 looks overbought with many investors wondering if the recent decline in market volatility is setting the stage for an imminent correction. The VIX index is down to 12.7, a month ago it was trading around 22.

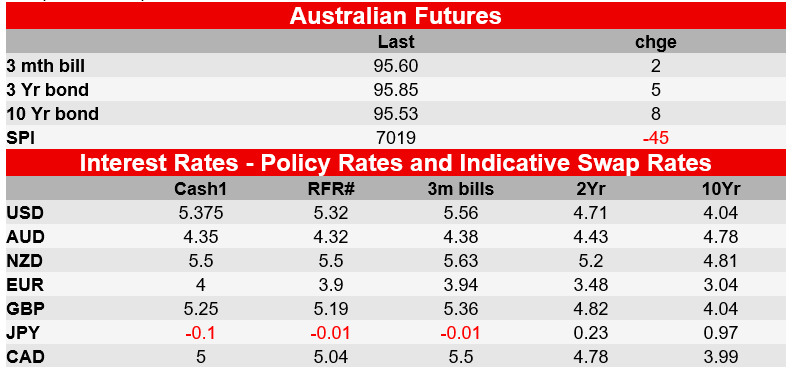

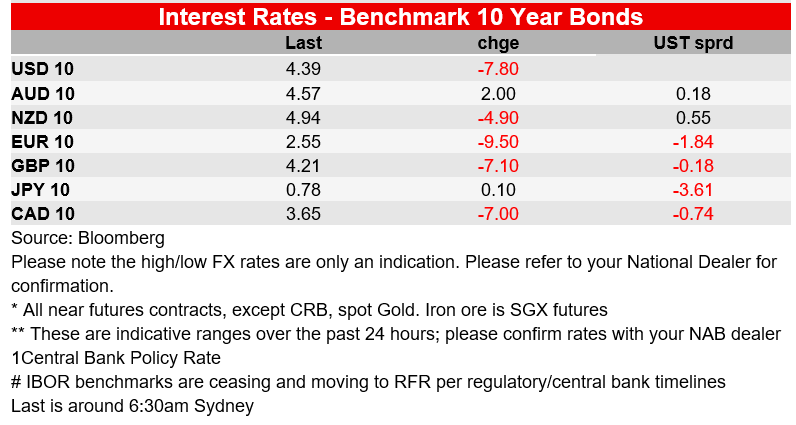

The outlook for central bank policy has been a big factor driving the improvement in risk appetite in November with evidence of an ease in inflationary pressures supporting the view many central banks are done with their tightening cycles while rate cut expectations for next year have been brought forward. The start of the new week has been light in both data and news flow, yet global bond yield have extended their monthly decline. European 10-year rates are down in the order of 9-10bps, while the UK 10-year rate is down 7bps.

Speaking overnight, ECB president Lagarde said the ECB will ‘probably’ discuss the reinvestment of its near EUR1.8tn PEPP holdings. Currently the Bank is reinvesting maturities and has said it will continue to do so until the end of 2024. As for the Labour market, Lagarde noted that “Despite the slowdown in activity, (it) remains resilient overall, although there are some signs that job growth may lose momentum toward the end of the year”. And on inflation, the President said that “we expect the weakening of inflationary pressures to continue, even though headline inflation may rise again slightly in the coming months, mainly owing to some base effects”. Adding that the inflation outlook however remains “surrounded by considerable uncertainty”.

Current ECB forecasts don’t project inflation returning to the 2% goal before the second half of 2025. Yet, this month the market has increased expectation of ECB rate cuts for next year and last night we saw another extension to this move. The market now prices 77bps of rate cuts by October next year, up 7bps relative to Friday’s pricing.

BoE Governor Bayle said in an interview with the Newcastle Chronicle newspaper published Monday that the recent step down in UK inflation is “very good news” but warned that the second half of the inflation battle will be “hard work.”. The market seemingly chose to focus on the good news and not the hard work ahead. On Friday the market was pricing 40bps of BoE rate cuts by November next year and now that pricing is at 51bps.

Moving onto the US treasury markets, yields are lower across the curve with the 2y tenor down 4bps to 4.911% the 5y, 10y and 30y are down between 5 and 8bps. The 10y Note has traded in a 12bsp range, climbing to 4.50% halfway through our trading session yesterday and now trades at 4.3885%, essentially at the lows over the past 24 hours. The decline in UST yields was supported by a solid 5y Note auction ($55b auction was awarded at 4.420% vs 4.425% WI yield ), although this was followed by tepid demand on the 2y Note auction ( Treasury’s $54b auction of 2-year notes was awarded at 4.887% vs 4.876% WI yield).

On US economic news, October new home sales fell 5.6% to 679K, below the consensus, 723K. Net revisions were -62K. The lack of existing home supply has helped homebuilders boost sales over the past year or so even notwithstanding a decline in demand given the increase in mortgage rates. More recently however, a new spike in mortgage rates in September and October, alongside a creep higher in existing home supply, has caused the upward trend in new home sales, both in volumes and as a share of total sales, to stall.

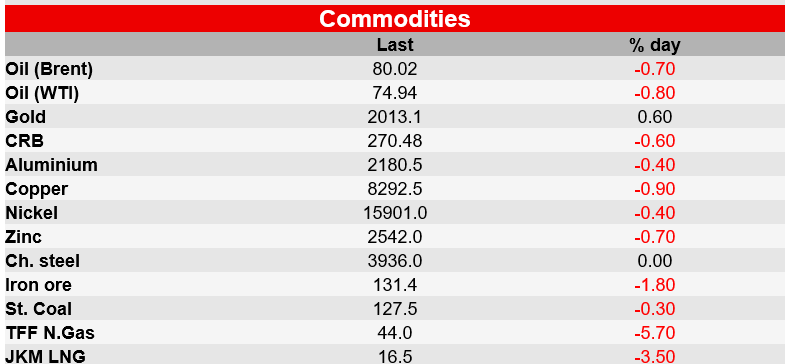

Moving on to FX land, the move lower in UST yields which accelerated post the well supported 5y Note auction has weighed on the USD. JPY is leading the charge (aided by lower UST yields), up 0.84% with USD/JPY now trading at ¥148.51. NOK is up 0.58% although this time not supported by higher oil prices with Brent and WTI down ~0.90%. Lates on the OPEC + delayed meeting have not been that encouraging, Saudi Arabia is asking others to reduce their quota to help support prices. Delegates report that no agreement has yet been made, amidst resistance to cut production

Antipodean currencies have extended their recent appreciation and importantly both pairs have managed to climb above key resistance levels, giving us more confidence they are now moving up into a new higher trading range. The AUD starts the new day at 0.6604 and NZD is at 0.6101.

Yesterday Australia’s Treasurer, Jim Chalmers, announced BoE’s Andrew Hauser will be the next deputy governor of Australia’s central bank. Andrew Hauser has spent more than 30 years at the Bank of England, the UK’s central bank, and served on the executive board of the International Monetary Fund. Notably too, Hauser has strong “green credentials”, in a paper delivered in May 2021 entitled It’s not easy being green – but that shouldn’t stop us, Hauser said “[a]chieving net zero is a pressing global priority. It requires action from everyone, including central banks”. As an outsider, Hauser is also expected to bring support one of the RBA review recommendations to “further encourage diverse viewpoints and constructive challenge”.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.