Online retail sales growth slowed in May following a fairly strong April

Insight

Lockdowns in Australia are likely to have a very acute impact on the economy, much more than what the RBA had pencilled in only a week ago. While NAB still expects a sharp rebound in activity when restrictions ease, the near-term impact is likely to be larger with lockdowns extending beyond Sydney (e.g. NSW, Melbourne and ACT).

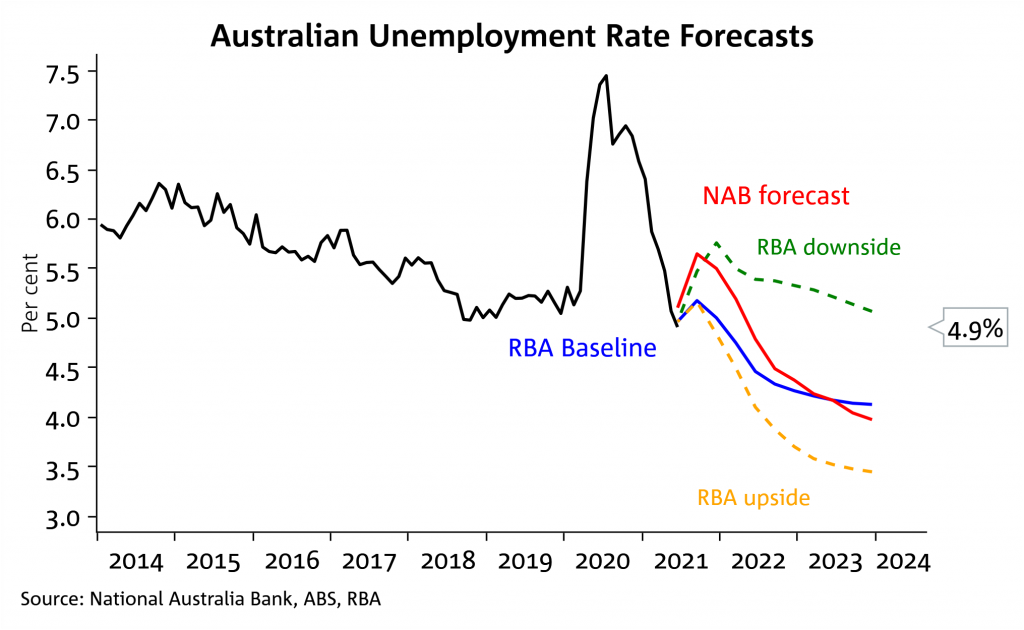

Chart 1: Unemployment expected to rise in the short term

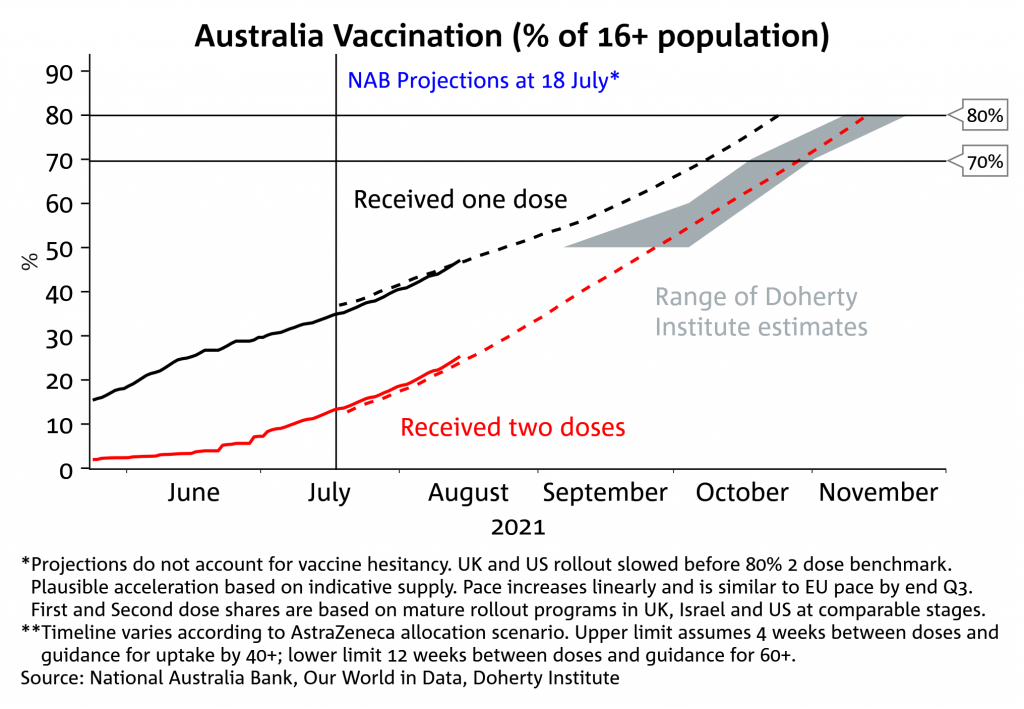

Chart 2: Vaccination hurdles on track to be achieved by mid-November

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.