Analysis: First signs of rebalancing as inflation and yields rise in the US

The persistence of elevated goods inflation surprised sharply in 2021 and has been one of the main drivers of global inflationary pressures. While supply chain issues have been important, demand has also figured, with durable goods consumption running 23% above pre-pandemic levels in the US and 24% higher in Australia. Markets had been expecting that as demand rotated back to services and away from goods, that inflation pressures would start to ease. So far, goods demand has remained elevated and supply chain disruptions have persisted.

In this Weekly we highlight some possible signposts that demand for goods and housing construction in the US may be starting to ease in the face of higher prices and higher interest rates. These will be important to watch given higher frequency data in the US may give a steer on what we can expect in Australia, while the pivot itself is also important for how quickly rates may rise and how high rates may get in this cycle.

(1) Freight indicators are starting to ease in the US and global freight rates have moved lower recently – though the move in global freight also reflects the impact of the lockdown in Shanghai: Freightwaves in the US points to several indicators showing trucking tightness beginning to ease. ‘Tender rejections’ a proxy for truck capacity tightness fell sharply in March and truck freight rates have also fallen despite higher fuel prices. Freight demand expectations have declined.

(2) Business surveys show a rise in inventories and a slowing in new orders: The US NFIB and ISM Manufacturing have shown an increase in inventories and a fall in new orders/sales expectations. One uncertainty is the extent to which firms are deliberately holding higher inventories given supply chain disruptions. On the other side of the equation, consumer surveys are showing a sharp fall in buying intentions, with the detail suggesting inflation is beginning to bite.

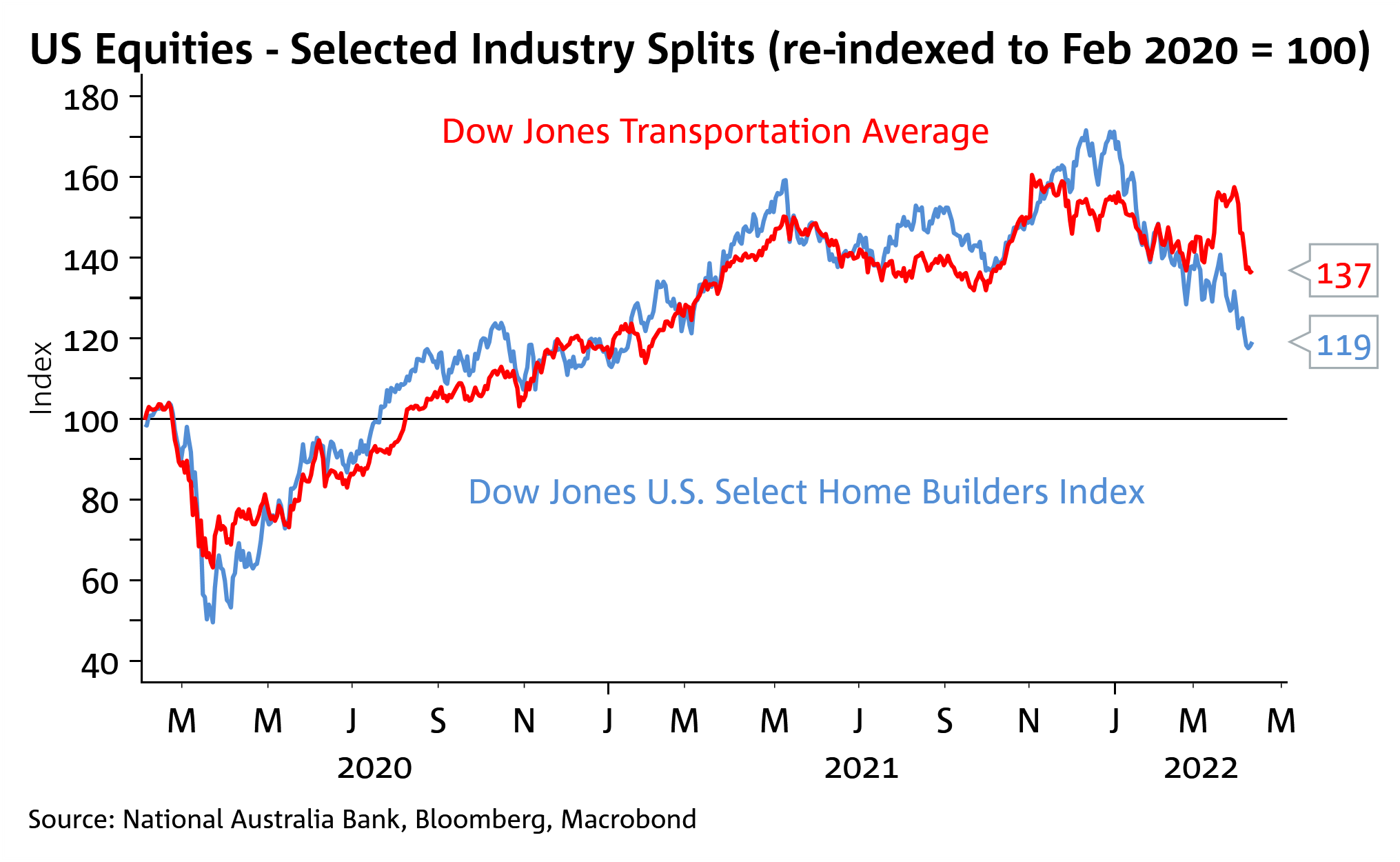

(3) US equities for homebuilders and transport firms have fallen, suggesting equity markets are seeing signs of cooling: The Dow Jones HomeBuilder Equity Index is now down 31.1% since its recent peak and the Dow Jones Transportation Index is down 13.5%. Equity investors in listed homebuilders are no doubt looking at the 30yr fixed mortgage rate which has now risen 179bps since the end of 2021 to be at 5.06%, its highest since 2011. Mortgage applications accordingly have fallen.

A rebalancing from goods to services demand is likely to alleviate some inflation pressures. However, with services inflation picking up and unemployment rates low, the US Fed and other central banks are still likely to remain hawkish and will want to get rates closer to neutral. For the US, the Fed’s long-run dot is pencilled in at 2.4% which is what markets are broadly pricing by the end of 2022.

As for the RBA, they too will want to lift the RBA cash rate to a more appropriate setting given the upside risks to inflation. A forward-looking pivot occurred this month with the RBA set to hike rates by June. A reduction in global inflation pressures may see a more measured hiking cycle than currently priced by markets with the speed of hikes and whether the RBA needs to go beyond neutral will depend more on wages.

Chart 1: The Australian NAB Business Survey is showing unprecedented prices pressure

Chart 2: Higher inflation is starting to impact buying conditions in the US. Will we see the same trend emerge in Australia?

Chart 3: Elevated goods demand is partly responsible for elevated goods inflation. Both Australian and the US durable goods demand is running around 25% above pre-pandemic levels.

Chart 4: Some signs equity investors are seeing signs of rebalancing on the back of inflation and higher rates.

Chart 5: Mortgage rate in the US have soared, they have also risen in Australia but not to the same extent