Analysis: Global recession risks lift, how will central banks respond?

Recession risks are high with NAB having called a US recession in 2023. Data out on Friday points to a possibility of the US having gone into a recession sooner (at least when measured as two consecutive quarters of negative growth) with the Atlanta Fed GDP Now pointing to Q2 growth of -2.1 annualised, following -1.6% print in Q1. The US ISM Manufacturing Index is also one indicator pointing to near-term weakness.

In this Weekly we explore how central banks may respond to rising recession risk and expand upon some of the leading indicators of recession. Our headline insight is that central banks are very focused on inflation and inflation expectations. From a risk management perspective, US Fed modelling suggests “the more costly error is assuming inflation expectations are anchored when they are not” (Mester 2022).

Fed Chair Powell played to this hawkish view at Sintra, noting: “Is there a risk we would go too far? Certainly there’s a risk….The bigger mistake to make — let’s put it that way — would be to fail to restore price stability”. Indeed the June FOMC forecasts see the unemployment rate rising four tenths as the Fed hikes to bring inflation back to target. Part of NAB’s rationale for a US recession is Fed tightening to combat inflation.

What would cause the Fed to pause and/or start cutting rates? Fed Chair Powell was posed this question in House Testimony – how would the Fed respond to a situation where inflation is still high and unemployment is escalating quickly, and economic growth is negative? Powell’s response was in that situation inflation could be expected to come down, and that the Fed could slow or stop rate rises, but be “reluctant to cut”.

That reluctance to cut would change once the Fed is assured inflation is on a firm downward track and inflation expectations were more anchored. This would allow the risk management approach to more firmly look towards activity rather than inflation. This of course does not apply to the current situation given labour market indicators are still strong with elevated job openings and jobless claims being at low levels.

One benchmark for labour market loosening is perhaps provided by the latest Fed Forecasts which sees the unemployment rate rising by four tenths as the Fed hikes. A forecast rise in excess of four tenths may be the catalyst for a more dovish pivot should inflation start to trend lower, and inflation expectations stabilise.

As for US recession risk, two important indicators for the US are pointing towards elevated recession risk. The ISM Manufacturing Index saw a sharp fall in the new orders sub-index, while the inventory index remained elevated. The difference in these indexes is widely used as a recession indicator and is currently in negative territory (see chart of the week).

The other indicator is the Atlanta Fed GDP Now for Q2 which is currently at ‑2.1%, following -1.6% in Q1. Of course, two consecutive quarters of negative growth don’t always constitute a recession, and to call one (especially in the US) you would also need to see rising unemployment. As such the Fed is unlikely to fear two quarters of negative growth if labour market indicators remain tight as they are currently.

Chart 1: US recession risks are elevated

Chart 2: Supplier deliveries are starting to ease, which points to supply chain pressures easing

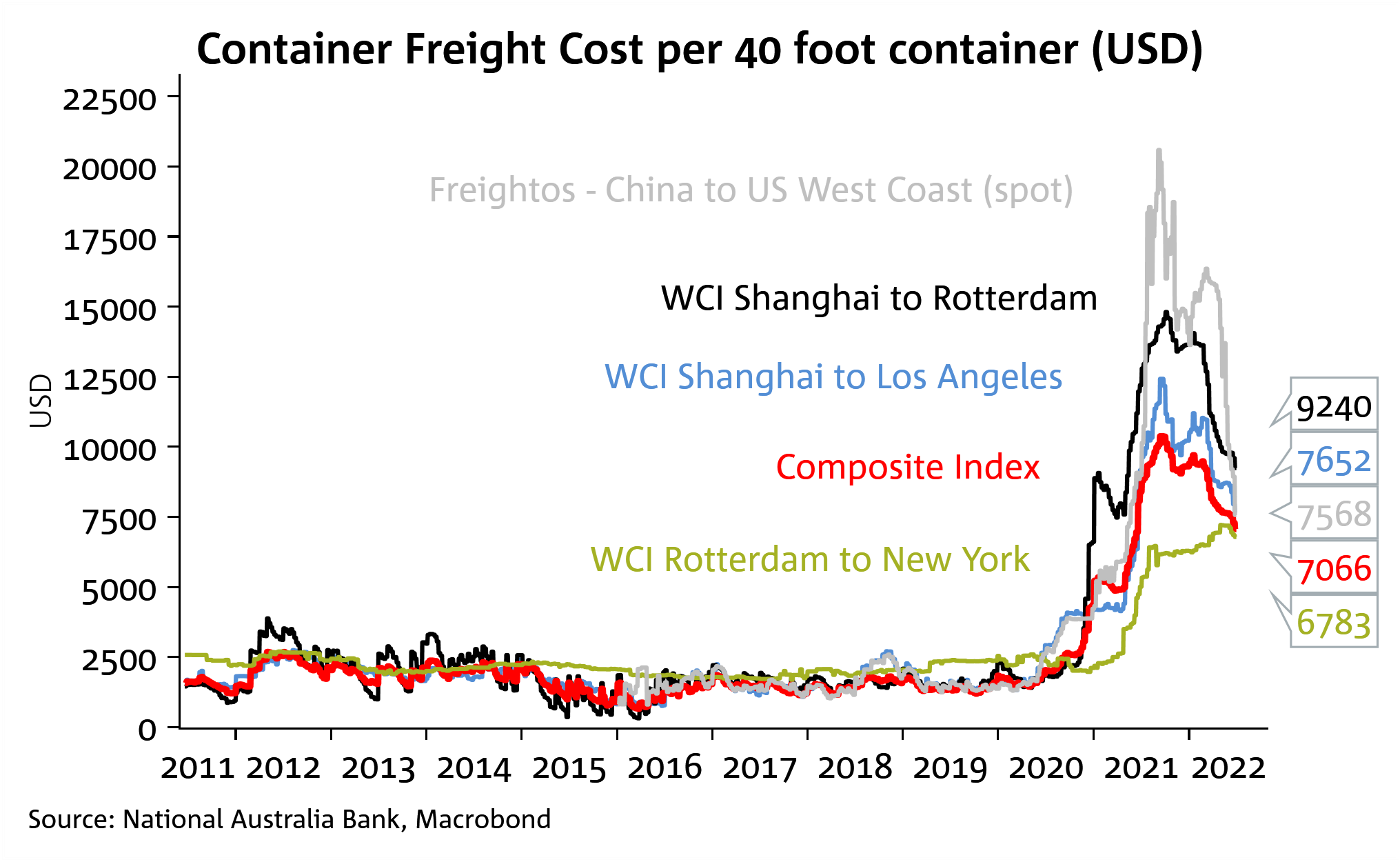

Chart 3: Freight rates have fallen sharply from peaks

Chart 4: Rate cuts priced for the US Fed in 2023, but not so for the RBA. Will this divergence persist?