Online retail sales growth slowed in May following a fairly strong April

Insight

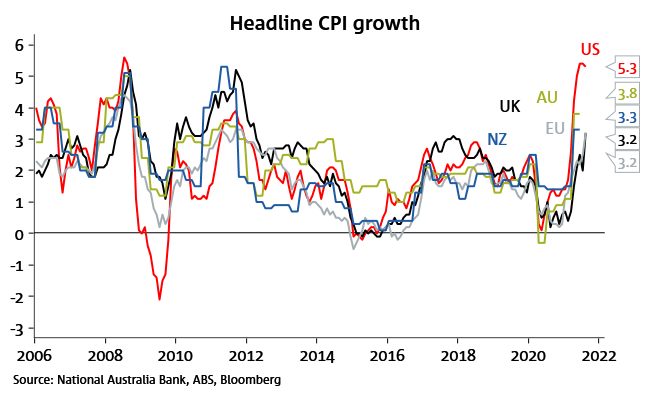

We are unlikely to get a true read of the underlying pace of inflation until mid-2022, with both transitory and policy driven impacts continuing to play out.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.