RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

In this Weekly we highlight some of the indicators that suggest a peak in global inflation is near

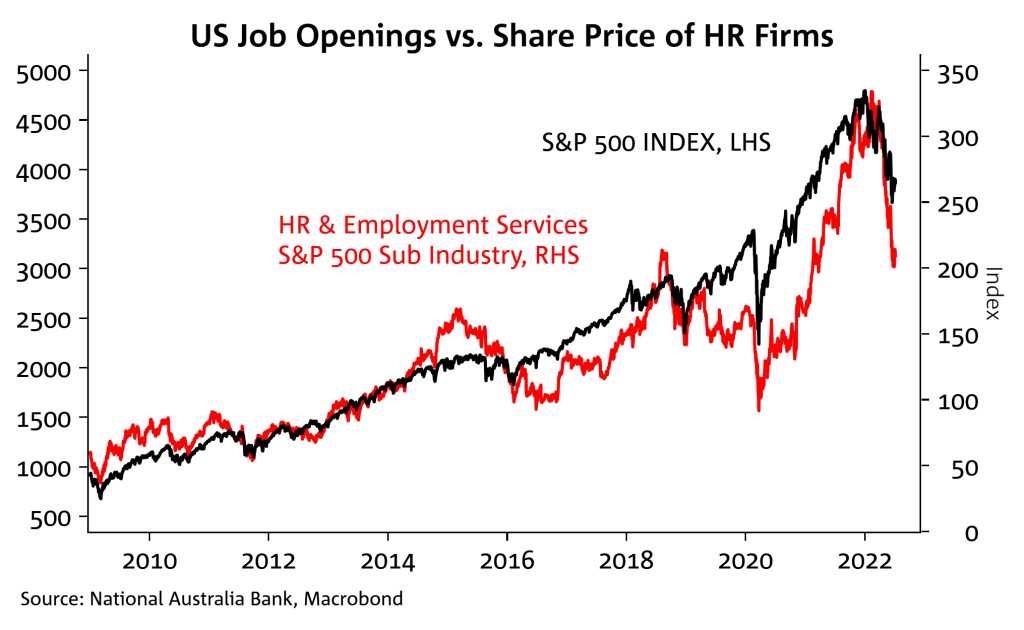

Chart 1: Labour market tightness could ease in the US according to equity investors

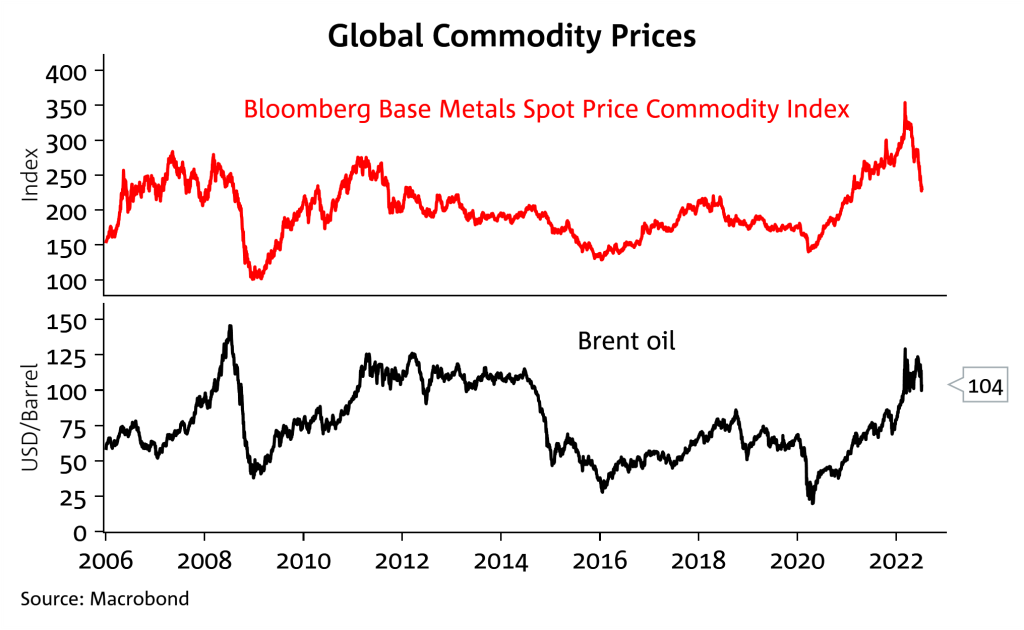

Chart 2: Commodity prices have eased recently

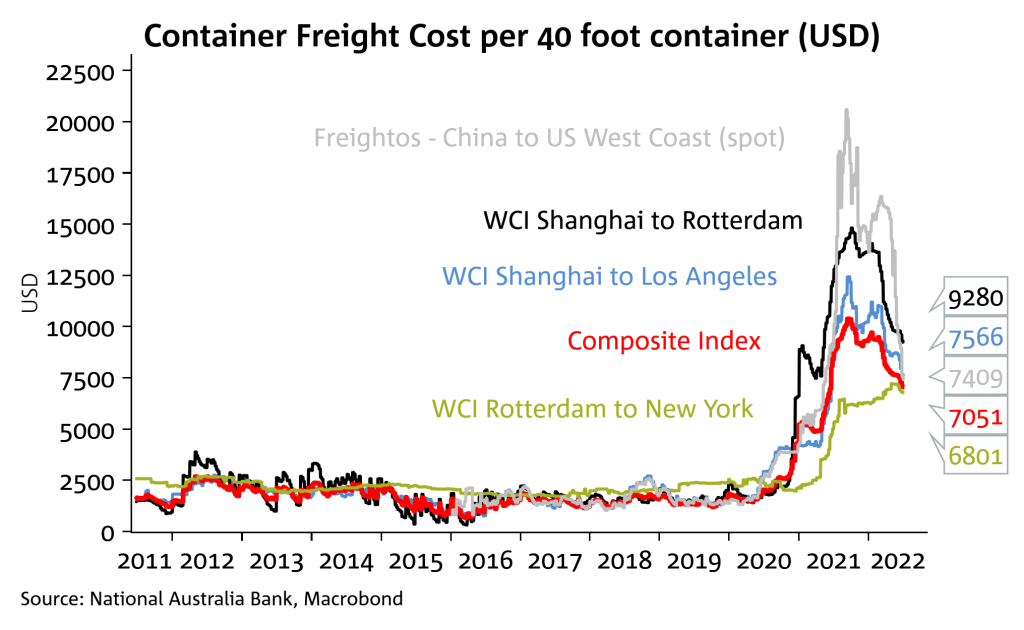

Chart 3: Container freight costs have eased sharply, though still remain well above pre-pandemic levels

RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.