Coming in for landing in a heavy cross wind

Insight

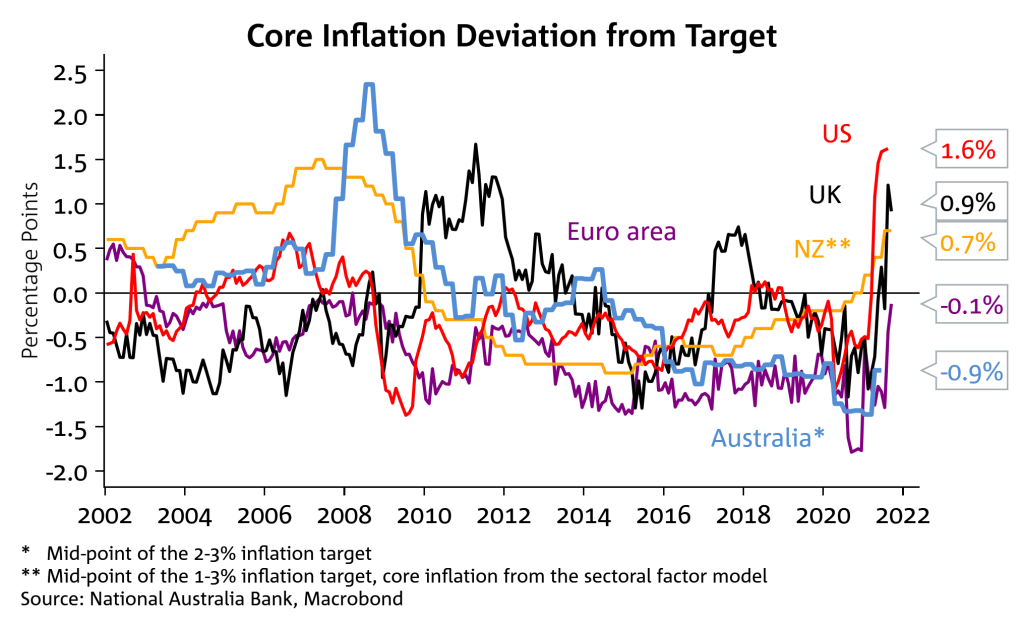

The RBA is likely to lag the US, UK and NZ in rates normalisation coming out of the pandemic.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.