On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

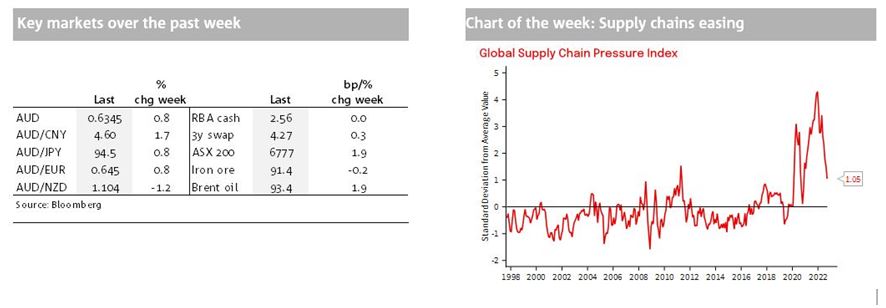

This week we provide a further update on supply chain disruptions and highlight a few areas where businesses might reasonably expect some lower prices from suppliers in coming months.

Analysis:

This week we provide a further update on supply chain disruptions and highlight a few areas where businesses might reasonably expect some lower prices from suppliers in coming months.

Indicators such as order backlogs, delivery times and freight costs have all broadly continued to ease in recent months, suggesting the worst of the supply chain disruptions are behind the global economy, barring some further unexpected development. An expected slowing in demand across the globe over 2023 should further reinforce this trend.

This suggests that businesses should be able to receive some relief on input prices in some areas in coming months. We’d nominate for container costs, and in the areas of steel and timber. Businesses should also consider their inventory levels as they balance current elevated demand and easing supply chain disruptions with expected slower demand next year.

This week:

An important and likely lively week for Australian markets. News over the weekend from the Wall Street Journal’s Nick Timiraos suggests that the Fed – like the RBA has just done – is considering slowing the pace of recent rate rises at some point. This has supported equity markets, eased some of the support for the previously rampant US$ (also assisted by likely BoJ intervention). Like the RBA, this news should not be interpreted as a dovish shift – central banks continue to signal a very strong commitment to returning inflation to target – but more reflects a reasonable desire to observe the impact of the previous rapid phase of rate rises on economic growth and inflation.

Domestically, the key events in Australia this week are Jim Chalmers’ first budget, tomorrow at 7.30PM and the Q3 CPI on Wednesday at 11.30am. The press gives details of the key budget forecasts (GDP growth for 2023/24 expected at 1.5% down from an expected 3.25% this financial year), while the inflation rate is seen easing to 3.5% in 2023/24 (slightly higher than the RBA’s 3.3% forecast in August). The latter upward revision likely reflects the impact of very recent floods but was finalised before the Q3 CPI release.

NAB expects a 1.3% q/q headline CPI outcome, a bit lower than market expectations for 1.5% q/q. Our slightly lower forecast reflects the impact of electricity subsidies in WA and QLD (though importantly Victorian assistance is not expected to be measured as a price reduction in the CPI). We are forecasting a higher underlying rate than the market and see the risks remaining skewed to the upside, especially as sharply higher airfares and rents have not been fully reflected in the Australian CPI as yet.

Elsewhere the ECB meets on Thursday and has been talking hawkishly about the need to restrain inflation. The BoJ meeting on Friday will also be keenly watched for any developments on the BoJ’s Yield Curve Control policy.

NAB Markets Research Disclaimer

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.