RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

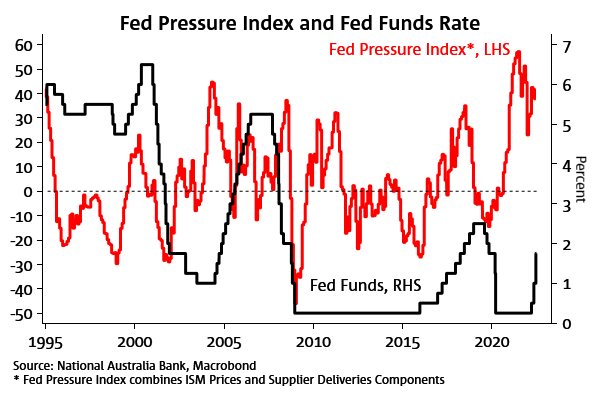

In this weekly, we look at some indicators that might reliably provide warning of some unwind or easing of the supply chain disruptions.

Chart 1: Fed Pressure Index right again

RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.