Long-term signal vs. Short-term noise

Insight

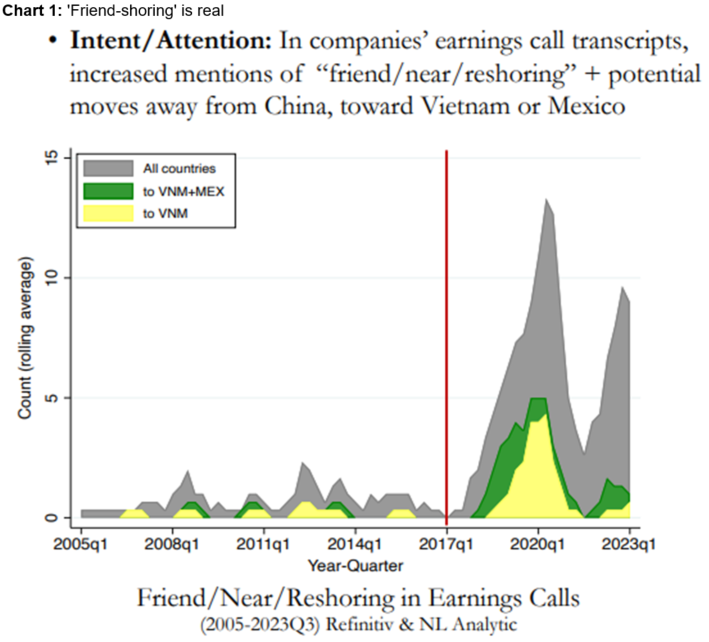

Powell affirmed the Fed will ‘keep at it’ on inflation, but what else happened at Jackson Hole? In the weekly, we pull out some of the key insights, including on the outlook for government debt and the ‘friendshoring’ dynamic.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.