NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Conditions are expected to remain strong for corporate and institutional level borrowers in Australia in 2019.

The syndicated loan market has been strong in Australia and Asia more generally this year. While not yet delivering record volume, the level of activity and demand from banks and funds increased significantly. Competition in certain sectors has been fierce, with Infrastructure a clear standout. Additionally, 2018 has seen a strong reinforcement of support for high brand credits, with big names getting incredible support from lenders locally.

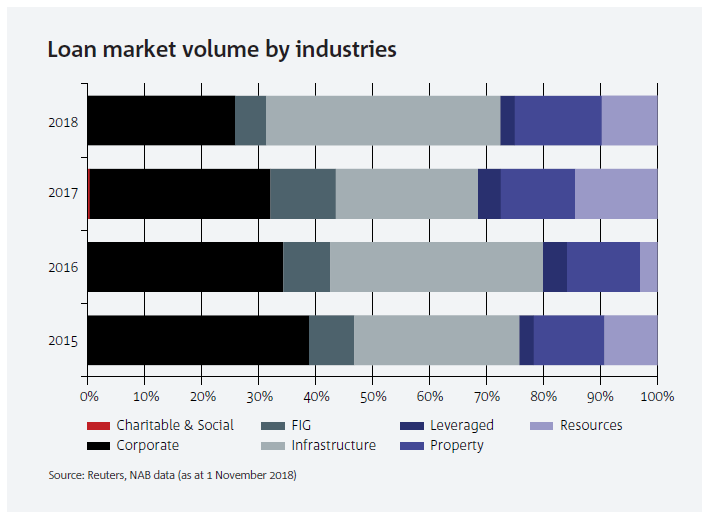

Availability of credit has been high and spread well across sectors. Given the focus on infrastructure nationally, it is no surprise that borrowing for infrastructure was the largest share of market in recent history. In the fourth ar quarter of 2018, demand is high and borrowers are approaching the market during its busiest quarter which is likely to make 2018 a record year for loan issuance. A key feature has been volume of underwritten loans, driven by a strong level of acquisition finance and very stable market conditions.

Additionally, movement on terms and conditions has started during the year.

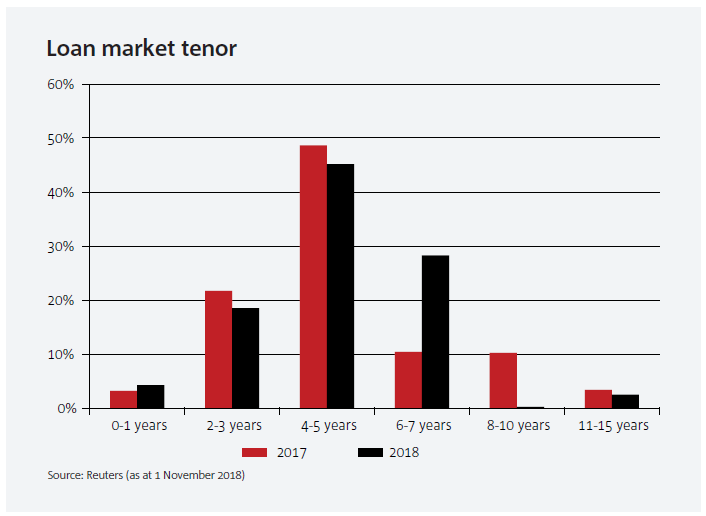

Demand from banks has been universal across the tenor spectrum. Borrowers have switched focus to longer tenor with the balance moving to five years from three and longer dated tranches being made available from both banks and institutional investors.

In certain sectors, headroom in financial covenants and debt sizing criteria has crept in favour of borrowers, again an indicator of strong competition for assets.

The increasing presence of the major Japanese and Chinese lenders has been felt throughout the year. Their ability to place large commitments, and increasingly underwrite transactions, has resulted in easy conditions for loan syndications. This flexibility has additionally resulted in a large number of self-arranged transactions passing through market. Volume of transactions has however allowed distribution to a variety of smaller lenders from Korea and Taiwan who have strongly supported underwritten transactions bookrun by the major banks in market.

A variety of Asian banks have opened operations locally in Australia to be close to borrowers and meet the need to be “local” to get allocation in transactions. Various European and larger Asian banks have also expanded local operations and product capabilities.

Institutional participation in Loans has seen a step change in Australia in 2018. Important work undertaken by several market participants, with NAB at the forefront, has seen institutional participation not only increase but extend into investment grade, real assets and corporates for the first time with any real momentum.

Transactions specialised as Institutional Term Loans for Brickworks, Visy, Viva Energy REIT and various others indicate the level of demand from institutional investors to participate in loans, not just focussing on high yield but building out a broad portfolio of unrated credit to complement existing portfolios. Leverage finance transactions have grown strongly in the Unitranche and Term B markets locally. Demand for these assets has been driven by several large institutional funds placing significant commitments to underpin transactions.

Following this has been a series of smaller funds and then several investment banks with deep global distribution channels, willing to provide underwritten commitments to their broad channels to stimulate this market.

There is no indication that institutional demand will wane or weaken over coming years. Funds are now firmly positioned in all levels of the syndicated loan market and will continue so as funds under management increase and drive alternate asset allocation volumes higher.

Significant demand for assets from banks has driven strong pricing outcomes for borrowers during 2018. Starting the year flat, pricing has eased in during the year driven by weight of commitments from banks in Australia and Asia:

Differential sector pricing has been a strong theme. Infrastructure and Energy/Utility borrowers have benefited from high demand, pricing between 20 and 30 basis points inside the broader corporate and institutional market. Notwithstanding this preference, pricing for all sectors has remained tight and borrowers have benefited from excellent pricing conditions.

With more banks than ever opening and maintaining branches in Australia, in addition to increased institutional participation, conditions are expected to remain very strong for corporate and institutional level borrowers in Australia.

Key headwinds of increasing bank regulation are likely to change the composition of lending groups and potentially pricing outcomes, rather than strictly limit availability of loan credit. Expect a strong year in 2019 as Australian and Asian banks in particular continue to provide Australian business with the credit they need to move the Australian economy forward.

This article was first published in 2019 Outlook Creating Opportunities. Read more articles from the magazine.

Speak to a specialist

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.