AMW: Government Debt and RBA balance sheet unwind musings

In this Weekly we look at Australia’s latest monthly deficit figures ahead of MYEFO in December, which show the deficit is set to come in much better than expected even with Sydney, Melbourne and Canberra having been in lockdown

Analysis: Government debt and RBA balance sheet unwind musings

UK Gilt yields recently fell in response to the latest UK Budget that saw debt issuance slashed by a fifth thanks to the faster-than-expected economic recovery. Gilt supply for 2021/22 was cut to £195bn, down by a fifth from the April projection and there could have been an even larger cut to issuance if bill supply was not also adjusted down by £25bn in a concerted effort to reduce bond market impacts.

As economies rebound and the ‘automatic stabilisers’ kick in (higher tax revenue and lower transfer payments as unemployment falls) it is likely debt issuance needs will fall sharply for more countries. Lower debt issuance is likely to offset apprehension within markets as central banks taper and end QE programs, and also potentially allows central banks to begin to unwind their bloated balance sheets.

In this Weekly we look at Australia’s latest monthly deficit figures ahead of MYEFO in December, which show the deficit is set to come in much better than expected even with Sydney, Melbourne and Canberra having been in lockdown. The 2021/22 YTD deficit to September 30 was $31.7bn against the Budget profile of $39.4bn, a $7.7bn improvement which came despite $24bn in extra assistance spending in lockdown.

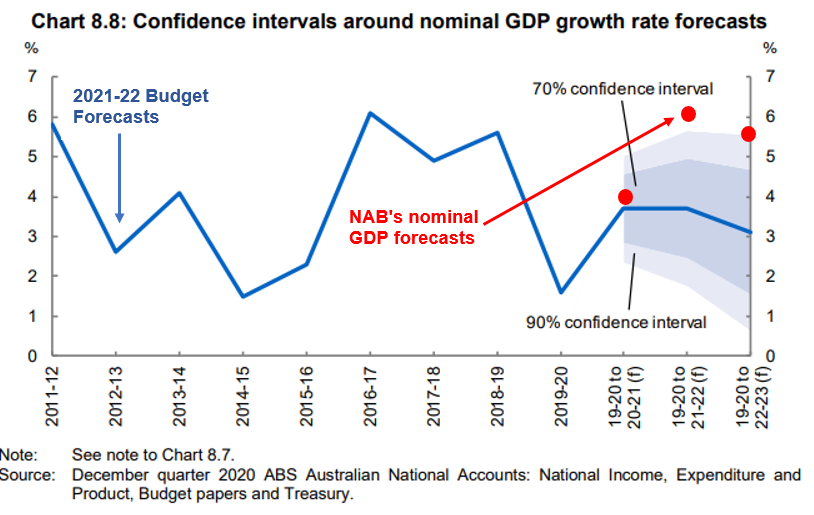

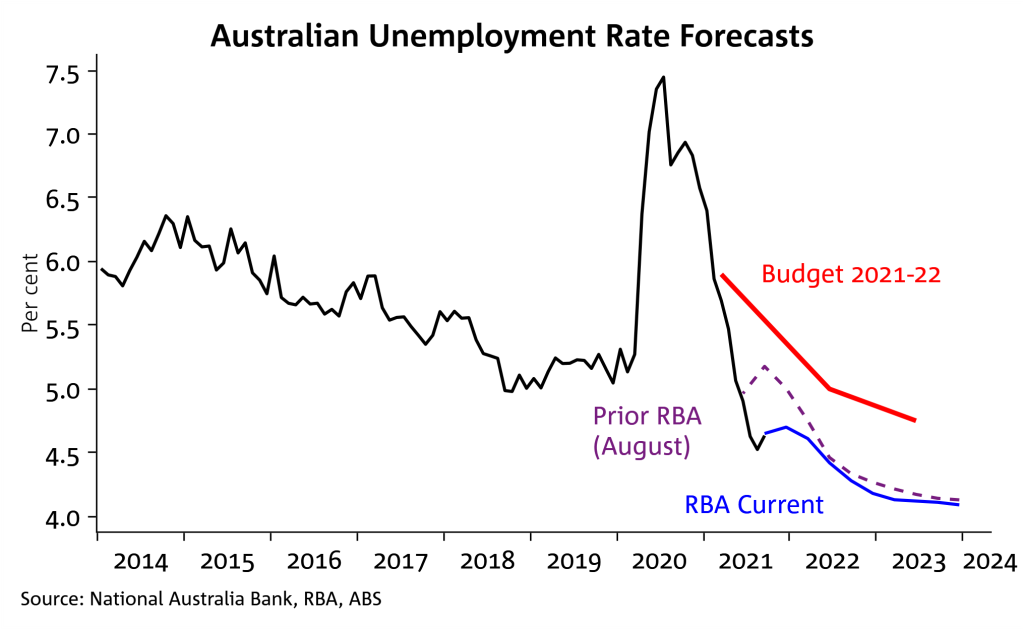

Since the end of lockdown, forecasters have revised up their projections. Taking the RBA’s latest November SoMP as a guide, unemployment is expected to be 4½% by June 2022 and fall further to 4% by June 2023. Clearly the RBA expects the economy to be stronger than what was assumed in the 2021-22 Budget even when accounting for the effect of the lockdown in Q3. Revenues run off the nominal side of the economy and the nominal side is running well ahead due to the terms of trade. Our preliminary 2021-22 nominal GDP growth forecast is around 6½%, well above the Budget’s 3.5%.

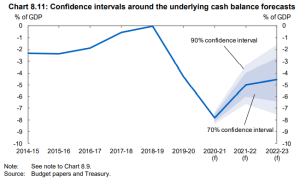

The 3ppts point difference if realised would place the nominal GDP above the its 90% historical confidence interval for the Budget forecast (see chart of the week below). If translated to the deficit this could see the deficit closer to 3.3% of GDP rather than the currently projected 5% of GDP. In dollars, that would mean a deficit closer to $70bn rather than the currently projected $106.6bn, $36bn lower than projected which is a third lower than forecast. While this is only rough, it broadly aligns with the monthly budget figures seen to date and excludes any new policy impacts ahead of the election that must be held by May 2022.

How will this interact with the RBA’s asset purchase program? RBA Governor Lowe has stated that the RBA’s current “plan is to hold to maturity ” and allow holdings to fall naturally as maturities fall due. The RBA of course has time up its sleeve to provide further clarity around the balance sheet (including on whether they see the balance sheet being larger than pre-pandemic), something Governor Lowe noted recently with the first bond maturity under QE not being until July 2024 for semis and November 2024 for ACGBs. Before then maturities for bonds acquired under YCC occur from April 2023. It is worth noting that some bond maturities related to market functioning have already been allowed to roll off.

Chart 1: Nominal GDP has been much better than projected in the 2021-22 Budget

Chart 2: Unemployment is also much lower, by up to 0.75 ppts compared to 2021-22 Budget projections

Chart 3: Underlying deficit consistent with the nominal GDP beat would be more consistent with a deficit closer to 3% instead of the current 5% forecast for 2021-22

Australian carbon project developers see a maturing of institutional financing as key to scaling the market and taking it on a similar trajectory as renewable energy.