Total spending grew 0.9% in June.

Whilst the US economy seems to go from strength to strength, there is speculation that China will ramp up stimulus measures to keep their economy strong.

https://soundcloud.com/user-291029717/brexit-hope-italys-mess-chinas-plans

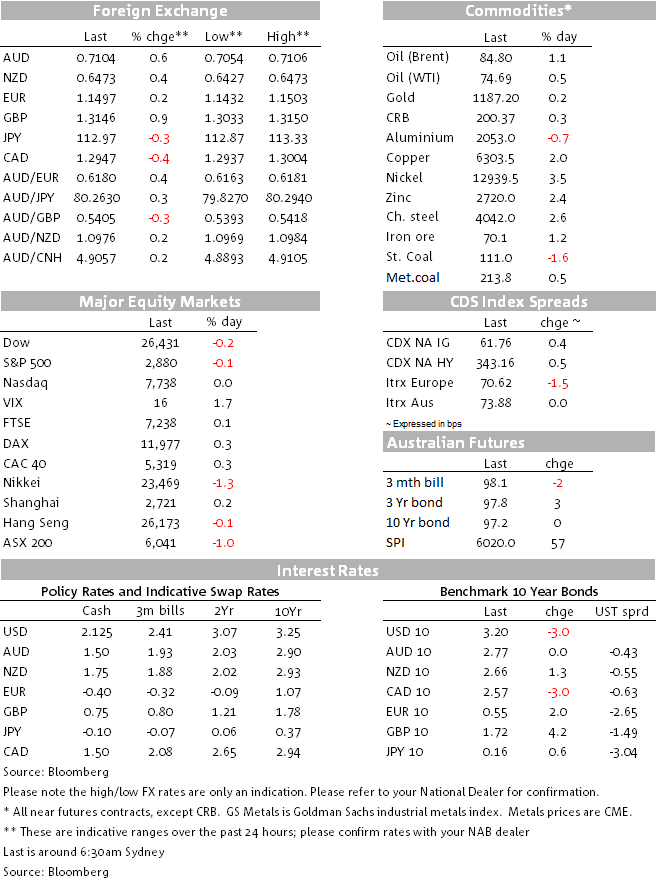

It’s been a rather listless overnight session for markets, investors recalibrating into Thursday’s US CPI, the next big US data piece in this evolving “high US growth/lack of inflation kick” picture for markets. The USD has been moving sideways, while US short term Treasury yields have been steady but longer term yields are down 3-4 bps, having tested higher earlier in the session. Sterling has seen some support as a very short Sterling market gets some positive Brexit mood music but wonders whether this is yet another false dawn. Oil has moved back up, as have base metals, mostly and iron ore/steel China prices.

The USD has struggled for new direction overnight, Sterling the centre of attention earlier in the overnight session – especially EUR/GBP that’s down 0.36% since yesterday afternoon. The EU’s chief Brexit deal maker Barnier noted that they had entered a 10 day “tunnel”, from which they would come out the other side hopefully with an agreement to put to an EU Summit on 18/19 October. PM May is apparently to present a revised Chequers proposal, seeking not to change a frictionless Northern Ireland/Ireland border with trade checks from the UK side. The market remains very short sterling and it’s only very recently that May received a cold reception from the EU at that Salzburg informal dinner summit, back to square one again.

There is also the matter of the UK Parliamentary approval to get over, so you can understand that the market is a tad skittish about whether a Withdrawal Agreement (WA) can be nutted out and agreed to by both sides with the clock ticking loudly now into coming EU Summits in coming months and the exit deadline next March. An agreement is presumably needed to extend the status quo beyond next March to January 2021.

The AUD has been trading in an orderly manner, making some net gains toward 0.71 where it sits this morning amid a listless USD. EM currencies have fared better overnight, the ZAR up 2.7% and the BRL up 1.9%, adding some background support, while commodities have generally also been friendly.

We also note that China will further increase export tax rebates from 1 Nov and quicken export tax rebate payments to support foreign trade, the State Council, the cabinet, said on Monday. The rise in tax rebates will help reduce costs for the real economy, help it cope with the complex international situation and maintain stable foreign trade growth, the cabinet said after a regular meeting. This is the 2nd increase this year, last month China increasing export rebates for 397 items, including steel and electronic products to help exporters as the trade war with the United States worsened. The Shanghai stock market was up marginally yesterday after Monday’s near-4% fall.

In the last hour, NZ dairy giant Fonterra has cut their milk price forecast for the 18/19 season from $6.75 to a range of 6.25-6.50. There’s been no fallout for the NZD, such a price in the market’s mindset already.

There’s little new to report on bonds. European high quality bond yields rose a little, but Italian and Greek bond markets rallied for once, Italian yields down 9.2 bps after the large push higher of late. The US Treasury curve has flatted with 2s steady but longer term yields easing back a net 3-4 bps.

Oil prices have continued to get support, WTI up 0.75% and Brent by 1.25% as the market continues to fret about supplies shrinking from Iran and Venezuela, an IEA spokesman calling for more OPEC supply. There is also Hurricane Michael approaching the Florida panhandle with around one fifth of US Gulf production closed as a result.

The US NFIB Small Business Optimism index for September barely missed expectations of a small pull-back after the August reading hit a record (107.9; L: 108.8; F: 108.3). Last week’s NFIB Employment report had already reported the continuing tightness of the US labour market for businesses, those elements of the survey reporting still elevated numbers of positions unable to be filled as well as increasing compensation and compensation plans.

Fed Presidents Kaplan and Harker have been speaking overnight. Kaplan repeated his recent remarks that he supports further gradual rises in the funds rate, another three by June 19, but reserves his judgement beyond that. He still doesn’t see “inflation running away” and noted the difficulty of not knowing whether productivity is rising, super important for business unit labour costs. Harker also noted that the labour market has very little slack with businesses telling him of the increasing difficulty of being able to fill jobs. There’s more Fed speak in our time zone today – see below.

The next big US data release is Thursday’s CPI. My colleague Tapas Strickland has released a preview in which he sees the risk tilting to a 0.3% m/m print for core CPI, above the market’s 0.2% consensus that his model formally predicts. Email me or ask the FX Strategists if you’d like a copy of that note, and similar heads up releases.

In late news, President Trump has been railing against the Fed and rate rises, saying that there isn’t an inflation problem.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.