Asset finance and leasing is in a growth phase in Australia as organisations seek a capital-effective way to modernise and upgrade across a broad range of asset classes and industries.

NAB’s review of first quarter corporate debt issuance.

Facing volatile financial markets in Q1, Australian corporate bond issuers maintained their funding diversification momentum across multiple global funding platforms better than one may have expected.

Volatile global credit markets yet few ‘goose eggs’

After a dream 2017 for global financial market performance, reality bit in Q1 2018 with volatility resurfacing. Yet in context it wasn’t significant enough to shutter credit markets or derail the term debt funding goals of Australian corporates.

After a solid January, volatility crept up over the quarter underpinning equity market gyrations and rising risk aversion for both credit investors and issuers. This ‘risk off’ thematic was attributable to concerns including US interest rate steepening in short and long rates, persistent headline risk and an elevation of a ‘trade war of words’ between the US and China. All of this caused ripples across financial market ponds.

Amid a cautious backdrop, primary market activity continued nonetheless and corporates globally progressed issuance plans. To illustrate the point in the deepest bond market in the world, the 144A market, days of ‘zero issuance’ — which in context are rare – are called ‘goose eggs’. In the roiled markets of Q1 2016 the 144A market saw nine ‘goose eggs’, Q1 2017 saw three, while Q1 2018 recorded only two according to Informa Global Markets.

Global credit markets reached an inflection point in early February, causing a rethink of risk-reward metrics and which in turn led to a widening of credit spreads. With local A$ bond issuance clearly tempered but not halted, corporate issuance volumes declined in major Northern Hemisphere public markets by about 10%-15% in Q1, compared with a year earlier.

The United States Private Placement market, which is popular for Australian corporates because it is less sensitive to volatility, fared better, ending flat in volume terms.

Secondary corporate credit spreads were marked wider over the quarter with secondaries wider by ~15bps even though actual selling appears to have been limited. Bloomberg secondary pricing data in fact showed that by the end of Q1, 75% of all bonds issued in euro markets were being valued at wider levels than where they were priced at launch.

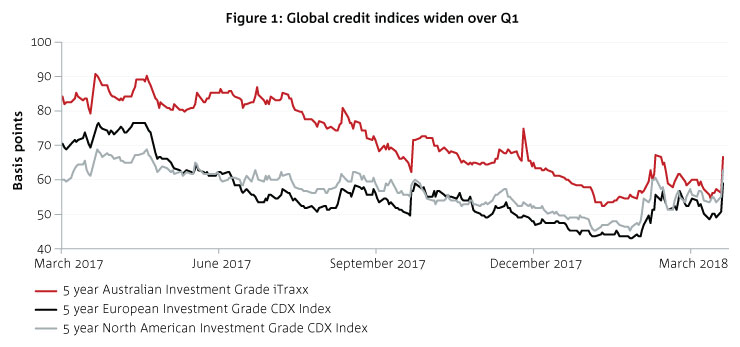

Closer to home, 5yr Australian major bank spreads — one of the best proxies for A$ credit risk — saw prices move 15-20bps wider from the low of +77bp in January, dampening financial and corporate enthusiasm to issue. Broader measures of risk sentiment, local and global credit default swap indices, similarly edged ~15bp wider versus the start of the year showing how interconnected global credit markets are (See Figure 1).

Figure 1: Global credit indices widen over Q1

Primary bond markets remained open

One primary execution feature that universally gained momentum over the quarter was the necessity to offer ‘new issue premiums’ (NIP) for new transactions as a means of using wider pricing on new issues to incentivise investor participation. For some price sensitive issuers this was a pill too bitter to swallow, while others keener to proceed accepted this to be the most commercial means to funding themselves in the debt capital markets

The size of premiums varied depending on market, with often quoted numbers ranging from 5bp-15bp. This is in the context of the S&P/ASX 200 recording its worst quarter since Q1 2008. While NIP oscillated, in Northern Hemisphere markets premiums ranged between 10bp-15bp in mid March causing flow-on effects globally, including to Australian financial and corporate issuers.

Australian corporate issuance rises in Q1

Unperturbed by this challenging backdrop, Australian corporates pushed ahead with their bond transactions, with a distinct focus on offshore funding diversification opportunities.

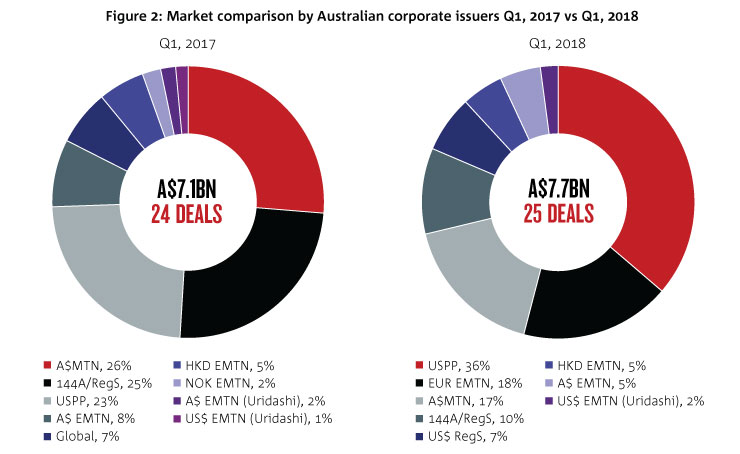

Large Australian corporates across multiple sectors issued an equivalent of ~A$7.7bn of senior ranking bonds across multiple markets from 25 transactions. NAB is pleased to have been associated with over 40% of this supply measured on a volume basis, or 45% of investment grade supply only, or almost one in every two dollars raised in volume terms.

Some of the larger issuers in volume terms and across multiple markets included Tabcorp (USPP), AusNet Services (A$, Euro and HKD), Toyota Australia (Euro, Euro A$, Uridashi), Fortescue Mining (Reg S/144A), Pacific National (USD Reg S) and Victoria Power Networks (A$ and HKD) to name a few. These included a variety of 5-yr and 10-yr and in some instances longer transactions in benchmark size in local and offshore markets.

Figure 2: Market and sector by Australian corporate issuers Q12018 vs Q12017

A number of large Australian corporates in the property and infrastructure sectors also undertook roadshows in Q1. If they had all issued as planned, Q1 issuance could well have been closer to A$10bn or more. As has been the case early in Q2, windows of stability should see these corporates come to various markets.

Key comparisons

Some key takeaways comparing the latest quarter with Q1 2017 are:

The second quarter is off to a positive start and we expect to see some of these themes continue in the second quarter.

Asset finance and leasing is in a growth phase in Australia as organisations seek a capital-effective way to modernise and upgrade across a broad range of asset classes and industries.

Growth in the major advanced economies bounced back in Q2

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.